Fri 10 Apr: After the Bell

Two-Week Rally Meets Geopolitical Reality

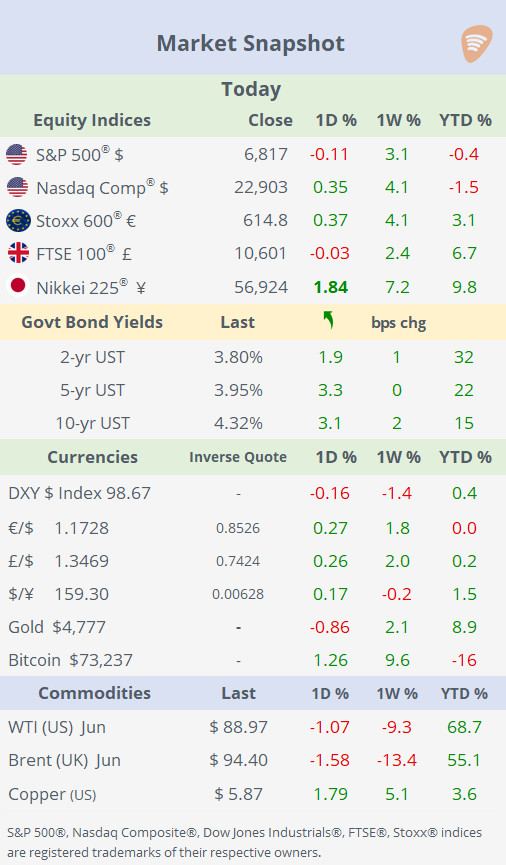

📈 Today’s performance tables.

Good evening,

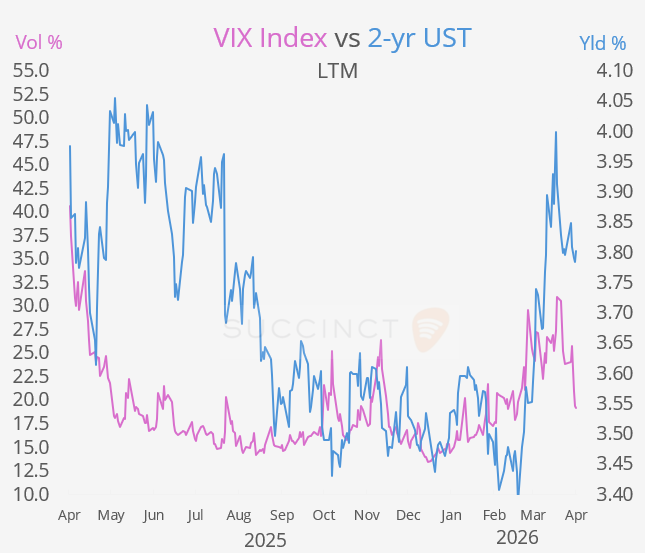

US equities paused on Friday but capped a strong week, with the S&P 500 rising more than 3%, its second consecutive weekly gain, driven by a relief rally following the fragile US–Iran ceasefire. Volatility eased notably, with the VIX Index falling to a six-week low of 19.2%, below its 2026 average, as risk sentiment improved despite lingering geopolitical uncertainty.

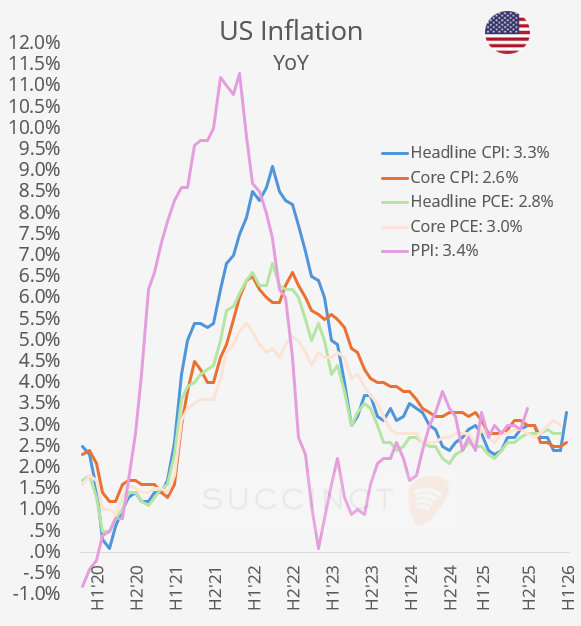

Macro data, however, painted a more complex picture. Headline CPI inflation accelerated sharply to 3.3% YoY in March, driven by a surge in gasoline prices amid the conflict, while rates markets now price the Federal Reserve on hold through year-end, with just a 21% probability of a December cut. Meanwhile, the DXY $ Index edged to a five-week low as the € and £ strengthened, and Treasury yields ended the week little changed, with 2-year yields around 3.80% (above its 3.6% YTD average).

Attention now turns to high-stakes Washington-Tehran talks set for this weekend in Islamabad, described by Pakistan’s Prime Minister as a “historic” moment that could “make or break” prospects for a lasting ceasefire. However, risks remain elevated, with Iran reportedly demanding the release of blocked assets ahead of negotiations and ongoing tensions in Lebanon threatening to derail progress, even as Iran-linked vessels continue to dominate traffic through the Strait of Hormuz.

In commodities, oil posted steep weekly declines but remains elevated in the high-$90s, highlighting a still-significant YTD rally and continued sensitivity to geopolitical developments.

Economics: → US headline CPI inflation rose +0.9% MoM in March (3.3% YoY, a 2-year high), in line with expectations and marking a sharp acceleration from February, driven primarily by a surge in energy prices. However, core CPI was softer at +0.2% MoM and 2.6% YoY, both below forecasts, suggesting underlying inflation pressures remain contained. The spike was largely attributable to the Iran conflict, with gasoline prices jumping 21.2%, accounting for the bulk of the headline increase, while several core categories (e.g. medical care, used cars) declined. Overall, the data presents a mixed picture, headline inflation re-accelerating on energy, but core trends pointing to ongoing disinflation beneath the surface.

→ The University of Michigan Consumer Sentiment Index fell sharply to 47.6 (April prelim), marking a steep decline from the prior reading and one of the lowest levels in recent years. The drop reflects deteriorating consumer confidence amid rising inflation expectations and geopolitical uncertainty, reinforcing a more cautious outlook for consumption despite still-resilient spending data.

Deals: → In private markets, CVC Capital Partners is seeking co-investors to support its proposed €10.9bn takeover of Recordati Industria Chimica Spa (mcap €10bn), a diversified pharma group focused on speciality care and rare diseases, with an equity cheque of €5.5–6bn, one of Europe’s largest recent LBOs. Early talks include major sovereign and institutional investors, though discussions remain preliminary, as CVC looks to syndicate risk and optimise the business post-acquisition.

→ In IPOs, HawkEye 360, a Virginia-based firm specialising in space-based radio frequency intelligence and analytics for defence and security clients, has filed for an IPO amid strong demand for defence tech. The company is expected to list in the US and was last valued at $2.0bn in its 2026 funding round, though IPO size/valuation targets have not been disclosed, suggesting an early-stage filing.

Week Ahead:

Data → M: US existing homes sales, India inflation. T: US PPI inflation. W: China macro data. Th: UK GDP, US industrial output.

Earnings → Q1’26 season kick-off. M: Goldman. T: JPM, Citi, Wells Fargo, BlackRock.

That’s all for this week.

Copyright © 2026 Succinct.

All rights reserved. This publication contains proprietary content and is intended solely for the recipient’s personal use. Disclaimer: Our service is for informational purposes only and does not constitute personal financial advice.