Fri 12 Dec: After the Bell

Choppy Week Ends with Tech Under Pressure and Commodities Mixed.

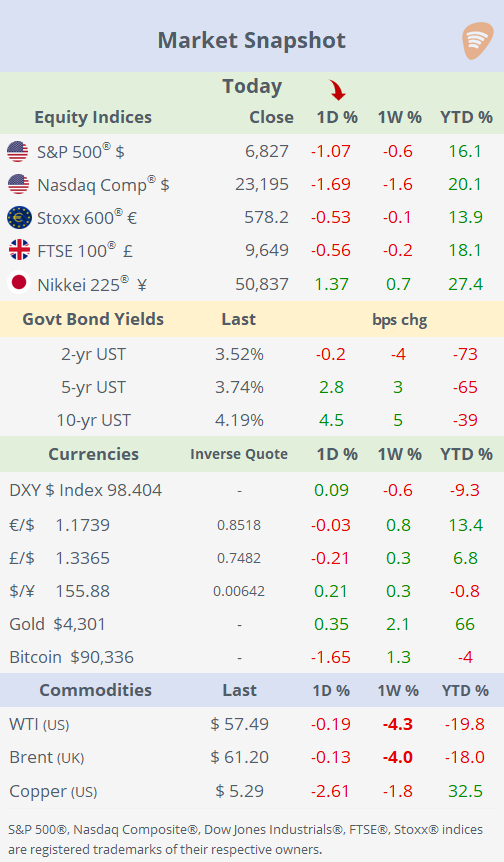

ℹ️ Today’s performance tables & charts on the ‘Market Data’ post.

Good evening,

Friday delivered a sharp risk-off tone across markets: the Nasdaq dropped nearly 2%, the S&P 500 slipped 1% from its record high, and the SOX Semiconductor index fell 5%. Technology was the clear laggard with an almost 3% decline for the day, making it the worst-performing sector of the week, while Financials and Materials led weekly gains.

Two consecutive earnings disappointments weighed heavily on sentiment: Oracle fell 11% on Thursday and Broadcom dropped 11% today, fueling renewed doubts over AI-related capex spending and elevated valuations. Broadcom’s results in particular triggered questions around sales forecasts, backlog visibility, and margin expectations.

The week’s main storylines included the Fed meeting, weak tech earnings and guidance, and the Warner Bros Discovery takeover developments. Despite substantial volatility in equities, both FX and rates markets finished the week little changed. Precious metals had a strong week, while energy markets sold off sharply, with crude oil down more than 4% and US natural gas lower by 22% WTD.

On the policy front, Trump stated that former Fed governor Kevin Warsh is now his leading candidate to chair the Federal Reserve.

Separately, China announced plans to impose export controls on certain steel products next year in an effort to limit outflows of a commodity frequently tied to global trade disputes.

Business News: → Disney will invest $1bn in OpenAI under a three-year deal that lets the startup use more than 200 Marvel, Pixar, and Star Wars characters in ChatGPT and Sora for user-generated images and videos. In exchange for licensing its IP, Disney receives equity plus warrants to buy additional OpenAI shares at a nominal price. The agreement is the largest AI–media partnership to date, signalling a clear thaw in relations between the two sectors.

Data: → UK GDP unexpectedly contracted by 0.1% MoM in October (+1.1% YoY), reversing forecasts for modest growth and reflecting broad business caution ahead of Rachel Reeves’ tax-raising Budget. The data underscore the Labour government’s economic headwinds, with output flat since May and activity weakening across production, construction, and services. 10-year Gilts yields jumped 4bp today to 4.521%.

→ Headline inflation for November was confirmed at 2.6% YoY in Germany, 0.8% in France, and 3.2% in Spain.

Deals: → In private markets, stablecoin leader, Tether Holdings, is pitching a massive private stock sale to raise ~$20bn at a $500bn valuation—among history’s largest—while blocking existing investors from secondary sales at discounts that could undermine the target. Post-deal, Tether eyes tokenising its equity on blockchain (via Hadron platform) or buybacks for liquidity, amid booming USDT circulation ($186bn market cap), and strategic talks with SoftBank/Ark.

→ In IPOs, Palo Alto, California-based Wealthfront (WLTH), a robo-advisor providing automated investing, cash management, lending, and planning for digital-native Millennials/Gen Z (1.3mn clients,~$90bn assets), priced its Nasdaq IPO at $14/share (high end of $12-14 guidance range), raising $486mn. Fully diluted market cap reaches $2.6bn at IPO price, with BlackRock/Wellington anchoring $150mn. Shares gained just 1% on their debut.

Week Ahead:

→ Monetary Policy meetings: Thu: ECB, Bank of England; Fri: Bank of Japan.

→ Data: Sun: China retail sales, industrial production; Mon: Canada inflation; Tue: US non-farm payrolls (Nov); Wed: UK inflation, US retail sales; Thu: US CPI inflation, Japan inflation; Fri: UK retail sales.

→ Earnings: Wed: Micron Tech; Thu: Nike, Cintas, FedEx; Fri: Paychex.

Enjoy your weekend.

Copyright © 2025 Succinct.

All rights reserved. This publication contains proprietary content and is intended solely for the recipient’s personal use. Disclaimer: Our service is for informational purposes only and does not constitute personal financial advice.