Fri 13 Feb: After the Bell

Cooling Inflation, Falling Yields; Equities Close a Volatile Week in the Red

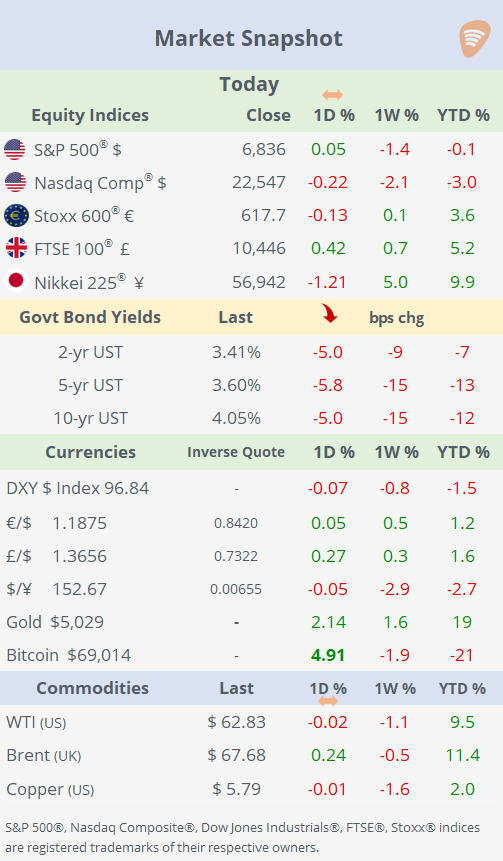

ℹ️Performance tables here.

Good evening,

Markets ended the week on a mixed but fragile note, stabilising on Friday after Thursday’s AI-driven selloff, though all major US indices finished the week lower. The Nasdaq underperformed (-2% WTD), while the S&P 500 slipped 1.4% on the week; the equal-weight S&P 500 fared better, reflecting continued rotation away from megacap tech amid further cooling in inflation data.

Under the surface, defensives led Utilities gained 7.3% on the week while Financials lagged (-4.8%) and the Magnificent Seven ETF fell 3%. Global markets were mixed, with Asian equities selling off in sympathy with US tech weakness and European indices little changed.

In rates, the bond rally extended sharply, with the 10-yr Treasury yield falling to 4.05% (-15bp WTD, the biggest weekly drop since August) and the 2-yr sliding to 3.41%, its lowest close since September 2022, reinforcing easing financial conditions.

A strong rally in corporate bonds in recent weeks has driven credit spreads to multi-decade lows, sharply reducing the compensation for taking extra credit risk and prompting warnings of bubble-like behaviour as investors aggressively hunt for yield. The ICE BoFA US Corporate (IG) Index Spread fell to 78bp and a 4.75% yield.

Bitcoin rebounded late in the week but still closed down ~2% at $69,000, while gold held above $5,000 and gained 1.6% on the week.

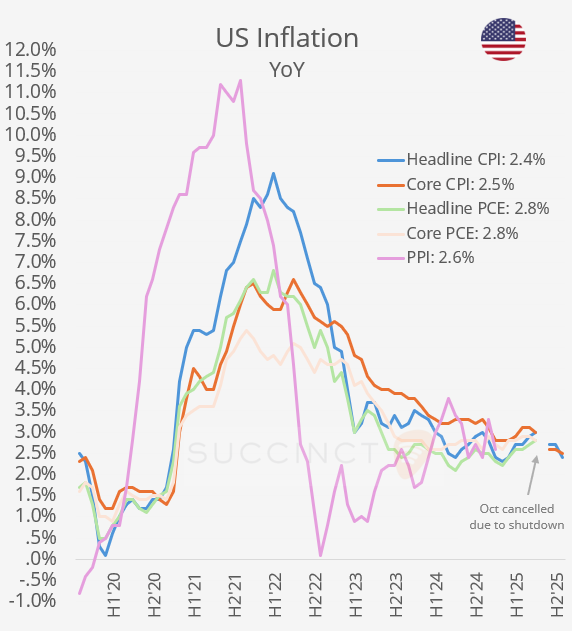

Economics: → US inflation cooled more than expected in January, with headline CPI easing to 2.4% YoY (from 2.7%) and core CPI steady at 2.5% YoY, helped by lower gasoline and used-car prices. Despite the softer inflation print and a strong jobs report earlier in the week, markets see little urgency for policy easing. Fed funds futures continue to price a ~90% probability that the Federal Reserve holds rates at its March 18 meeting, with only a 10% chance of a rate cut, reinforcing the Fed’s wait-and-see stance.

Earnings: → It was a quiet day in the US, but a few non-US releases stood out:

→ Safran (France, Aerospace & Defence): shares jumped ~8% after a clear beat on earnings and cash flow, helped by strong aircraft engine deliveries, resilient aftermarket demand, and upgraded full-year guidance — the guidance uplift was key for the rally.

→ Enbridge (Canada, Oil & Gas Midstream): shares rose ~4% on stable earnings, reaffirmed dividend growth, and reassurance around cash-flow visibility — investors rewarded the defensive profile and income certainty.

→ NatWest (UK, Banking): results were broadly in line, with capital returns supportive but no major surprise.

Corporate Deals: → In private markets, Platinum Equity agreed to sell Spanish waste management group Urbaser to Blackstone and EQT for $6.6bn, in one of the largest European infrastructure-style buyouts this year. Blackstone and EQT will each acquire 50% stakes and jointly control Urbaser, while Platinum Equity will retain Urbaser’s Argentine waste management operations, carving them out of the transaction.

→ Savvy Games Group, an online gamer backed by Saudi Arabia’s Public Investment Fund, is in advanced talks to acquire Moonton from ByteDance in a deal valuing the studio at $6bn, marking one of the largest cross-border acquisitions of a Chinese gaming asset. The potential sale reflects ByteDance’s retreat from gaming after failing to challenge Tencent, while underscoring Saudi Arabia’s ambition to build a global gaming and esports champion using its multi-billion-dollar war chest.

Week Ahead:

Data → T: UK unemployment, Canada CPI; W: US housing starts, FOMC Minutes, UK CPI; Th: Japan CPI; F: US personal income and spending, UK retail sales.

Earnings → M: BHP; T: Palo Alto Networks, Cadence Design; W: Booking H, Analog Devices, Moody’s, Glencore; Th: Walmart, Airbnb, Deere, Alibaba; F: Warner Bros, Anglo American.

That’s all for this week.

Copyright © 2026 Succinct.

All rights reserved. This publication contains proprietary content and is intended solely for the recipient’s personal use. Disclaimer: Our service is for informational purposes only and does not constitute personal financial advice.