Fri 13 Mar: After the Bell

Three Weeks of Losses for US Equities; Oil & $ rally; PCE inflation update.

ℹ️ Today’s performance tables.

Good evening,

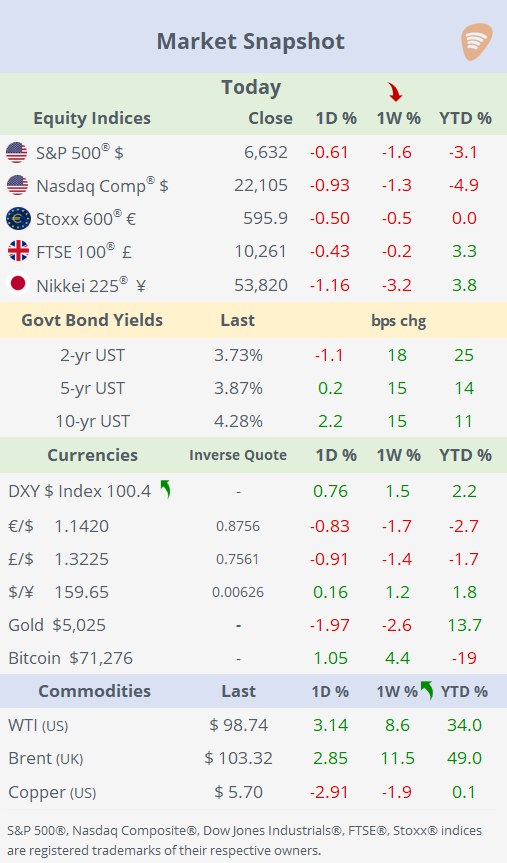

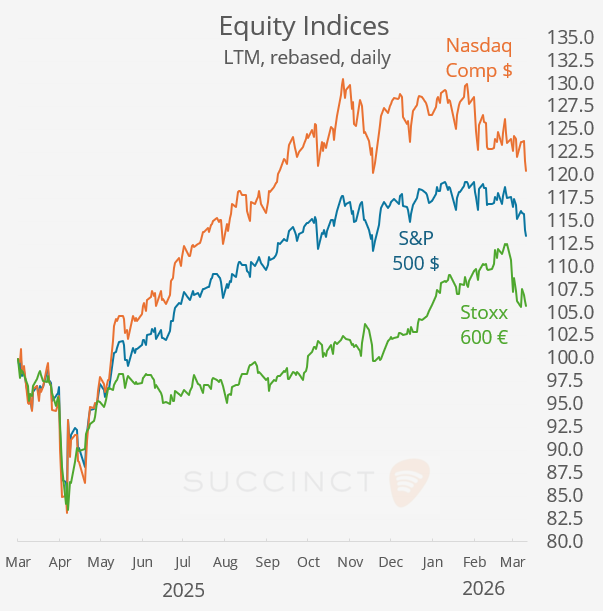

Markets ended the week on a weak footing, with stocks on Wall Street declining again and extending their losing streak to three consecutive weeks. The S&P 500 fell 1.6% over the week as geopolitical tensions continued to weigh on sentiment. Oil climbed back above $100, while safe-haven flows lifted the $, pushing the DXY above 100 points to its highest level since May. The move came as the € and £ each lost ~1.5% over the week, sending the € to an eight-month low, while gold slipped around 2% to end near $5,000.

The geopolitical backdrop remains the dominant driver of markets. Iran stepped up attacks on shipping in the Strait of Hormuz, prompting the Pentagon to deploy additional warships and a Marine expeditionary unit to the region, a force that typically includes several vessels and roughly 5,000 Marines and sailors. The escalation has kept energy markets on edge and reinforced fears of a prolonged disruption to global oil supply.

Separately, in Washington, a federal judge dismissed two Justice Department subpoenas issued to the Federal Reserve in a criminal probe into whether Fed Chair Jerome Powell misled Congress about cost overruns at the central bank’s Washington headquarters. The ruling represents a legal victory for the Fed, with the judge stating that the subpoenas appeared designed to “harass and pressure” Powell amid ongoing political tensions with the White House.

Economics: → US PCE Inflation, the Fed’s preferred inflation measure, showed headline PCE rising 2.8% YoY, slightly below expectations and easing from the previous month. Core PCE, which excludes food and energy, rose 3.1% YoY, in line with forecasts and remaining well above the Fed’s 2% target. The report underscores that underlying inflation remains sticky, particularly in services, strengthening the case for the Fed to stay on hold for now. The data also predates the Iran conflict and the sharp rise in oil prices, which could push headline inflation higher in the coming months and complicate the Fed’s policy outlook.

→ Other US data releases today: Michigan Consumer Sentiment (55.5): slightly above forecasts but still very weak historically, and the drop is largely tied to higher gasoline prices following the Iran conflict. JOLTS Job Openings (6.94mn): broadly in line with expectations and consistent with the gradual cooling trend in labour demand, nothing suggests a sharp deterioration in the labour market. Durable Goods Orders (0% MoM): roughly as expected, pointing to flat business investment momentum but no major surprise.

→ The UK GDP release was mildly disappointing but largely a non-event for markets. The economy showed 0% MoM growth in January, below expectations of +0.2%, while annual growth came in at 1.1% YoY, pointing to modest expansion but still weak momentum. Overall, the data reinforced the picture of sluggish growth rather than contraction, and had little impact on markets, which remain focused on geopolitics and the surge in oil prices.

Corporate Deals: → Friday was a quiet day for M&A deals. In fintech, Airwallex said it plans to invest about $1.1bn over the next five years to expand across Europe, launching in markets including Spain and Sweden. The cross-border payments firm, valued at $8bn, said its EMEA revenue more than doubled in Q4’25 as transaction volumes tripled, highlighting strong growth in the region. Airwallex is a private fintech company founded in Australia, now headquartered in Singapore, and backed by Tencent, T. Rowe Price, and DST.

→ In IPOs, Singapore-based GLP is exploring a Hong Kong listing that could value the company at $20bn, marking a potential return to public markets after being taken private in 2017. The firm manages over $80bn in logistics real estate, data centres, and infrastructure assets, though the timing and size of the IPO have yet to be finalised.

Week Ahead: Active for central bank policy meetings.

Data → Su: China retail sales, industrial production, house prices; M: Canada inflation; T: Australia (RBA) and Indonesia policy rate decision; W: Fed rate decision (unch exp); Th: ECB, BoE and BoJ policy rate decision.

Earnings → W: Tencent, Micron Technologies; Th: Enel, FedEx; F: Carnival.

That’s all for this week.

Copyright © 2026 Succinct.

All rights reserved. This publication contains proprietary content and is intended solely for the recipient’s personal use. Disclaimer: Our service is for informational purposes only and does not constitute personal financial advice.