Fri 17 Apr: After the Bell

Markets Rally to New Highs as Hormuz Reopens

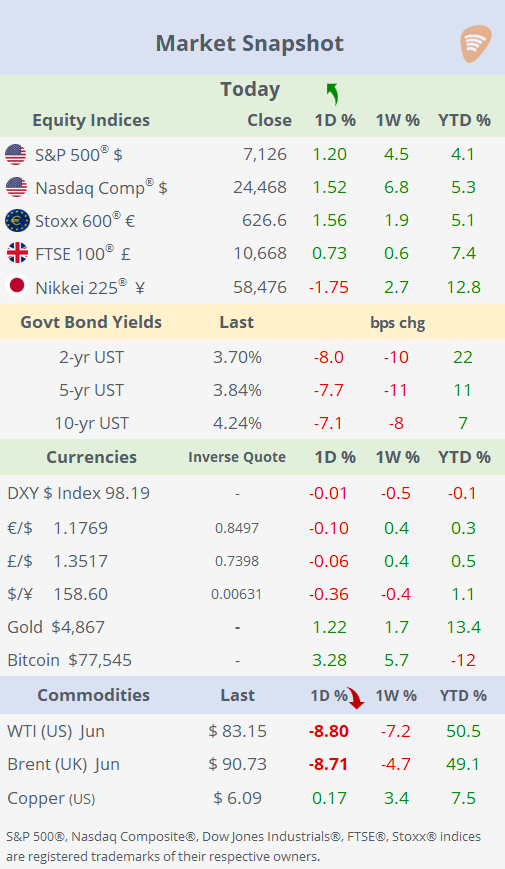

📈 Today’s performance tables.

Good evening,

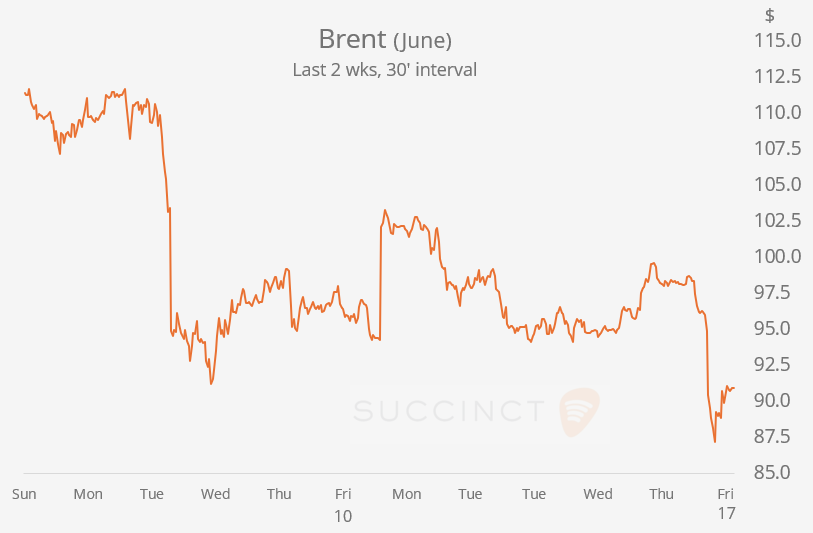

Global markets closed the week in strong risk-on mode, with equities extending their rally as hopes grew for a de-escalation in the Iran conflict. Iran said the Strait of Hormuz was open, while Trump said talks with Tehran could take place this weekend and that a deal to end the war may come soon, helping send oil sharply lower even as some shippers awaited further clarity and security guarantees. European leaders also offered military support to secure the waterway.

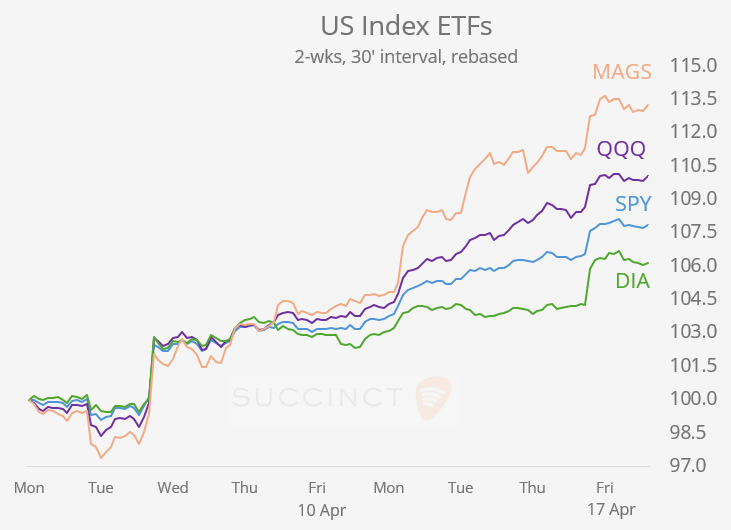

Wall Street responded with another powerful advance, capping one of its strongest three-week runs since 2020. The S&P 500 rose every day this week and gained 4.5% WTD, while the Nasdaq surged nearly 7%, driven by an 8% jump in the Mag-7 and broader IT sector strength. All major US equity benchmarks are now positive for the year, with the Russell 2000 leading on a 12% YTD gain.

Bonds rallied as Treasury yields fell ~8bp across the curve, taking the 2-year yield to 3.70%, a four-week low, while currencies were little changed and Bitcoin added 6% on the week.

Today’s data calendar was quiet, with no meaningful economic releases to drive markets. On the earnings front, only Truist Financial (+2.3%) and State Street (+2.5%) reported, both topping estimates, with shares modestly higher.

Deals: → In sports deals, the San Diego Padres are set to be sold by the Seidler family to a group led by José Feliciano and Kwanza Jones for a record $3.9bn, the highest valuation ever for an MLB team. Feliciano is the co-founder of Clearlake Capital and part of the ownership consortium of Chelsea FC. The transaction would surpass the previous MLB sale record of $2.4bn for the New York Mets in 2020.

→ In France’s telecom sector, Bouygues Telecom, Orange, and Iliad Group submitted bids worth ~$24bn for Altice Group’s telecom operations, as controlling shareholder Patrick Drahi seeks to reduce leverage. The proposed transaction would break up SFR and reshape the country’s telecom market, reducing the number of major operators from four to three.

→ In private markets, TPG invested $100mn in Zum, valuing the US student transportation and mobility company at $1.7bn, up from its $1.3bn valuation in the 2024 Series E round.

→ In IPOs, Massachusetts-based Kailera Therapeutics, a biotech focused on obesity and weight-loss drugs (GLP-1/GIP pipeline), raised $625mn, priced its IPO at $16 for a $2.1bn valuation, and shares jumped 62.5% on their Nasdaq debut under the symbol KLRA.

→ California-based Alamar Biosciences, a life sciences company focused on ultra-sensitive proteomics and diagnostics tools, raised $191mn, priced its IPO at $17 per share for an approximately $1.1bn valuation, and shares rose 29% on their Nasdaq debut under the symbol ALMR.

→ AEVEX Aerospace, a US drone and defence technology company, raised $320mn in its NYSE debut, pricing shares at $20 for an implied valuation of ~$1.8bn, with the stock gaining 34% on its first trading day under the symbol AVEX.

Day Ahead:

Data → Sun: China LPR rates. Mon: Canada inflation, Germany PPI.

Earnings → n/a.

That’s all for this week.

Copyright © 2026 Succinct.

All rights reserved. This publication contains proprietary content and is intended solely for the recipient’s personal use. Disclaimer: Our service is for informational purposes only and does not constitute personal financial advice.