Fri 19 Sep: After the Bell

🎙️📄+ Market Data

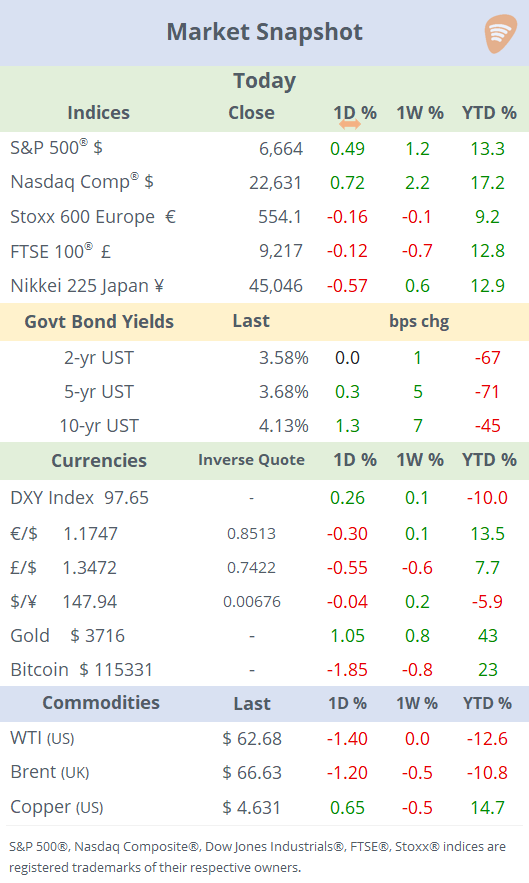

See the ‘Market Data’ post.

Good evening,

Stocks have continued their upward march this week, with major indices hitting record highs and corporate borrowing spreads narrowing to their tightest levels this century, even as investors caution that markets may be “priced for perfection” amid rising risks.

Today marks a triple witching day in US financial markets, when stock options, index options, and index futures expire simultaneously, often bringing heightened trading activity. Tech led the gains, driving the Nasdaq up 2.2% for the week and lifting its YTD return to 17%, with standout performers including Intel, Synopsys, CrowdStrike, and ASML, which rallied between 14% and 23% WTD.

Bond markets were quiet, though yields on the long end of the curve rose 7bp over the week, partially reversing a recent decline. The DXY $ index edged slightly higher across the last few sessions, finishing almost flat for the week, while the £ was this week’s notable mover on the downside. Crude oil dipped 1% on Friday but ended the week broadly unchanged.

In geopolitics, Estonia, a Baltic country in Eastern Europe, has invoked NATO Article 4, which calls for consultations among allies when a member’s security is threatened, after a “unacceptable” Russian airspace violation by three MiG-31s; NATO condemned the incursion as “reckless” following its jets’ interception.

Trump said Washington and Beijing have approved a deal for investors to control TikTok’s US operations, with new investors owning about half the company and existing ByteDance stakeholders (including Susquehanna, KKR, and General Atlantic) holding roughly 30% while ByteDance’s stake drops below 20% and Oracle will manage user data.

“I just completed a very productive call with President Xi of China. We made progress on many very important issues, including trade, fentanyl, the need to bring the war between Russia and Ukraine to an end, and the approval of the TikTok deal,” Trump posted.

Monetary Policy: The Bank of Japan maintained its key short-term interest rate at 0.5%, as expected. Two out of seven board members dissented, advocating for a quarter-point hike, indicating a shift towards a more hawkish stance. Governor Ueda emphasised that, while Japan's economy has shown a moderate recovery, global economic uncertainties persist, necessitating a cautious approach to monetary policy. In a significant policy shift, the BoJ announced plans to gradually unwind its $250bn holdings of ETFs and REITs. Japan’s core inflation rate, released today, decelerated to 2.7% YoY in August from 3.1% in July, to the lowest level since October.

Data: Germany’s producer prices fell 2.2% YoY, accelerating the deflationary trend. UK retail sales rose 0.7% YoY, a soft slowdown from the previous month.

In commodity markets, Arabica coffee futures plunged to a one-month low of $3.60 today, marking a 4% drop and a 7.6% decline for the week. The downturn follows reports that US lawmakers are preparing to introduce a bill to exempt imports from tariffs. This potential policy shift could alleviate trade disruptions, particularly with Brazil, the world's largest arabica coffee exporter, which has reduced shipments due to a 50% tariff.

Deals: Sumitomo Mitsui Financial Group (mcap $107bn), Japan’s second-largest bank, is raising its stake in US investment bank Jefferies Financial Group (mcap $14bn) to 20%.

Apollo is in advanced talks to acquire a majority stake in Spain’s Atlético Madrid, marking its first major football investment; the club has an estimated €1.9bn enterprise value and generated €410mn in revenues last year.

IPOs: Verisure, the Swiss-based home and small business security provider majority-owned by private equity firm Hellman & Friedman, is considering a €3bn IPO on Nasdaq Stockholm, in what could become one of Europe’s largest offerings in recent years.

Week ahead: M: China loan prime rates. T: G7 PMIs, Japan holiday. W: US new home sales. Th: Swiss National Bank and Banxico policy meetings, US GDP update. F: US PCE inflation, Canada GDP.

Enjoy your weekend.

Copyright © 2025 Succinct.

All rights reserved. This publication contains proprietary content and is intended solely for the recipient's personal use. Disclaimer: Our service is for informational purposes only and does not constitute personal financial advice.