Fri 20 Mar: After the Bell

No Ceasefire in Sight: Equities Tank, Treasuries Tumble, Fed Rate Hike Odds Jump

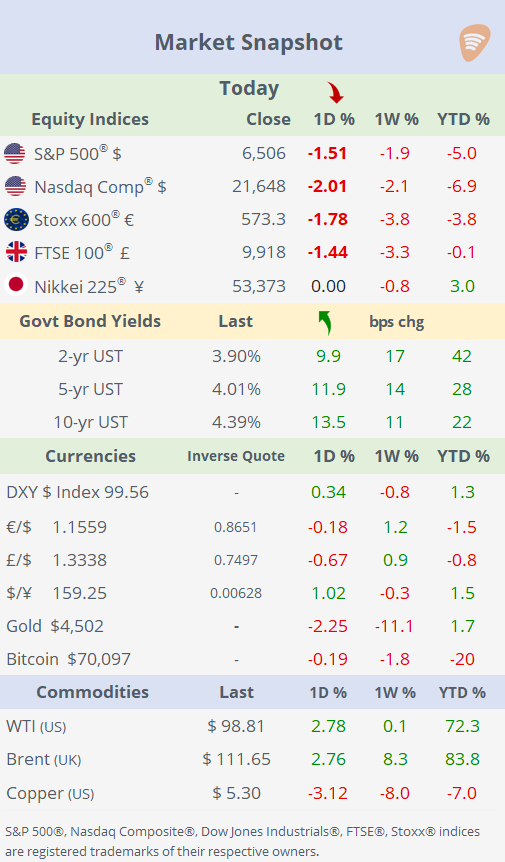

ℹ️ Today’s performance tables.

Good evening,

Equities and bonds sold off sharply this week amid escalating Middle East tensions, with no ceasefire in sight, driving a broad risk-off sentiment.

The Pentagon deployed three warships and thousands more Marines to the region, the second such Marine deployment in a week, keeping investors on edge as attacks intensify. Trump stated Friday he’s not interested in a ceasefire with Iran, fueling fears of prolonged conflict. Mideast risks now dominate markets, with Iran targeting Gulf oil sites and aiming for $200/barrel crude to disrupt the global economy.

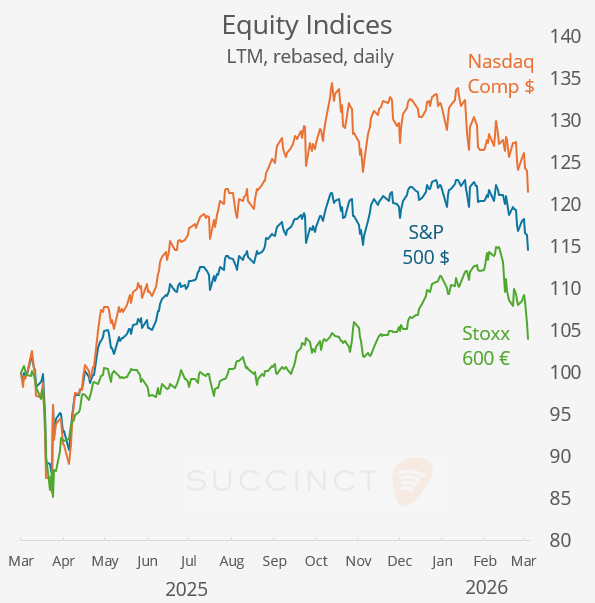

Leading US and European indices fell 2% on Friday, capping a tough week. Europe underperformed sharply, with Germany’s DAX and Switzerland’s SMI down ~4% WTD, despite the € gaining 1.2% against the $.

Benchmark US 10-year Treasury yields rose 13bp today to their highest since July, reflecting bets on rate hikes. Futures now price a 10% chance of a 25bp Fed increase at the April meeting, up from 0% a week ago. In the UK, 10-year Gilt yields rose to 5%, a level not seen since 2008, as inflation fears mount amid the war’s economic fallout.

Gold posted its lowest close since early January after declining daily all week, pressured by shifting rate expectations. Crude oil bucked the trend, rising 3% today; longer-dated Brent for Dec ‘27 trades near $78/barrel, up from $66 last month, signalling bets on sustained supply risks. Saudi Arabia warns of $180 oil if shocks persist past April.

Economics: → Germany’s PPI fell -3.3% YoY (vs. -2.7% exp) and -0.5% MoM, confirming deeper-than-expected producer price deflation, likely driven by weaker industrial demand and easing input costs. The data reinforces a pipeline disinflation trend in Europe, suggesting continued downside pressure on CPI and supporting a more dovish policy backdrop.

Monetary Policy: → Russia’s central bank cut rates by 50bp to 15% (as expected), continuing its easing cycle as inflation gradually slows and economic momentum softens. The move signals a cautious normalisation path, with further cuts likely, but policymakers remain wary of pro-inflation risks (energy, fiscal dynamics) that could limit the pace of easing.

Corporate Deals: → Unilever Plc (mcap $134bn) is in talks to spin off its food division and merge it with McCormick & Co (mcap $14bn) in an all-stock deal, as part of a broader portfolio overhaul. The move would exit food and refocus Unilever on higher-growth beauty, personal care, and home segments, a strategy aligned with activist pressure from Nelson Peltz. Unilevel shares are 6% lower YTD.

→ NY-based Prestige Consumer Healthcare (mcap $3bn) will acquire a portfolio of OTC brands, including Breathe Right, from private equity-owned Foundation Consumer Healthcare for ~$1bn.

→ In IPOs, the Denver-based senior housing REIT Janus Living was priced at $20 (the top end of the guidance range), raised $840mn at a $5.9bn valuation, and shares jumped 18% on today’s debut on the NYSE under the symbol JAN.

Week Ahead:

Monetary Policy → Banxico on Thursday.

Data → M: Japan inflation; T: Australia inflation, PMIs in developed countries; W: UK inflation; F: UK retail sales, US Michigan consumer confidence.

Earnings → Busy for Chinese bluechips, including China Telecom (Tue); PDD and China Life (Wed); Bank of China, CNOOC (Thu); and ICBC, Petrochina (Fri).

That’s all for this week.

Copyright © 2026 Succinct.

All rights reserved. This publication contains proprietary content and is intended solely for the recipient’s personal use. Disclaimer: Our service is for informational purposes only and does not constitute personal financial advice.