Fri 23 Jan: After the Bell

What You Need to Know: Markets End Volatile Week as Geopolitics Drive Cross-Asset Swings ➡️

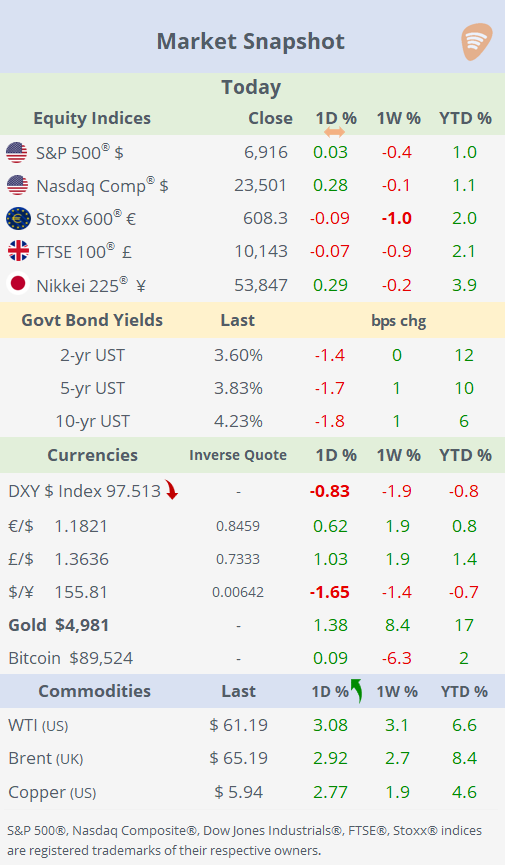

ℹ️ Today’s performance tables & charts on the ‘Market Data’ post.

Good evening,

Equities ended Friday on a mixed note, capping a volatile week dominated by shifting geopolitical headlines. The Nasdaq Composite extended recent gains as tensions eased modestly, while small caps underperformed sharply today, with the Russell 2000 down nearly 2%. The S&P 500 finished little changed but still posted a second consecutive weekly decline amid wide intraday swings. Intel weighed heavily on sentiment, plunging 17% after issuing a disappointing first-quarter outlook. This week, equities in the US outperformed Europe, with energy leading sector gains and financials lagging.

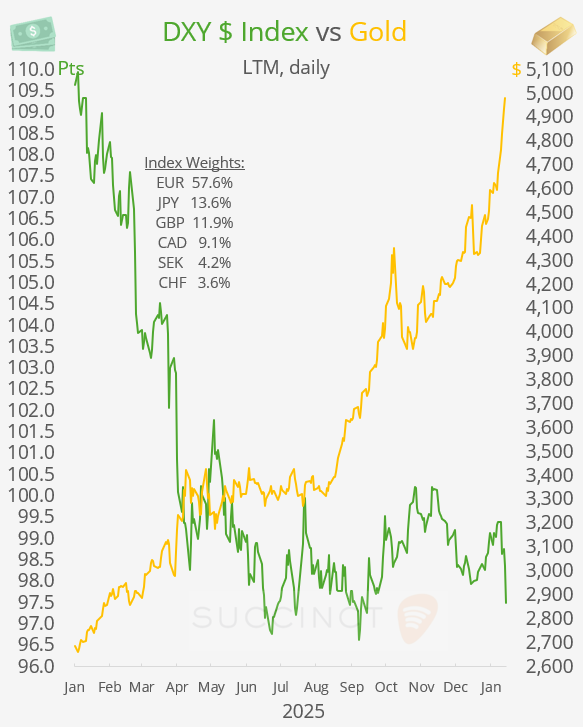

Safe havens surged as geopolitical risk and $ weakness drove gold toward $5,000, its strongest week since 2008, while silver broke above $100. FX markets were particularly volatile, with the $ sliding to its lowest level since late September against the ¥, £ and Swiss franc, as the € hit a four-month high.

Oil prices rebounded as renewed US rhetoric toward Iran revived supply-risk premiums, lifting both Brent and WTI. Meanwhile, benchmark yields ended the week little changed ahead of next Wednesday’s Fed meeting, with the 10-year Treasury at 4.23%, up 12bp over the past month.

Silver surged 6% to a record above $100/oz primarily on acute supply tightness, with the market entering a fifth consecutive year of global supply deficit, prompting aggressive dip-buying and short-covering. The rally has been reinforced by haven demand, lower rate expectations, and a breakdown in the gold-to-silver ratio, but supply constraints remain the dominant driver behind the sharp gains.

Monetary Policy: → The Bank of Japan kept its policy rate unchanged at 0.75%, as expected, but revised up its inflation and growth forecasts, adopting a slightly more hawkish tone and signalling that a rate hike could come in the near term if conditions evolve as projected. The shift supported the yen’s sharp appreciation, which rose strongly against the dollar to a two-month high, reflecting increased expectations of further policy normalisation. At 2.26%, the 10-year JGB yield remains at the highest level since 1998. (WSJ)

Economics: → The Univ of Michigan’s US consumer sentiment index rose to 56.4, marking an improvement and the strongest print since August. The uptick points to a modest recovery in household confidence, likely reflecting easing inflation pressures and improving real income dynamics.

→ UK retail sales rose 2.5% YoY in December, the strongest annual increase since April, signalling a late-year improvement in consumer spending. The rebound suggests some resilience in household demand despite still-elevated interest rates and cost-of-living pressures.

→ Flash Composite PMIs (Jan) across the US, €-area and Germany stayed firmly in modest expansion territory, broadly in line with expectations and showing little change from December. The data point to stable but unspectacular growth momentum, offering no new signal on the near-term economic outlook or policy path.

Corporate Deals: → Clorox (mcap $14bn) agreed to acquire Gojo Industries (privately owned by the Lippman-Kanfer family), the maker of Purell hand sanitiser, for $2.25bn in an all-cash, debt-funded deal, expanding its footprint in health and hygiene. After tax benefits of roughly $330m, the net purchase price is about $1.92bn, with Clorox aiming to leverage Gojo’s strong B2B distribution to accelerate growth in its professional segment.

IPOs: → US construction tech and equipment rental firm EquipmentShare.com priced its Nasdaq debut at $24.50 per share, raising $747mn. The Missouri–based company operates a technology-enabled equipment rental and jobsite management platform and listed at a valuation of $7.2bn. Shares rose 33% on their trading debut, signalling solid investor appetite for new US listings. (Reuters)

→ In Europe, the Czech defence group Czechoslovak Group (CSG) jumped around 30% on its Amsterdam debut, taking its market capitalisation to roughly €30bn. The company raised €3.8bn at €25 per share in the largest-ever IPO by a defence company, benefiting from strong demand amid record-high defence stocks. (BBG)

Week Ahead:

M → US durable goods, Germany Ifo indics. T → Earnings by United Health, Boeing, GM, UPS, Texas Ins, LVMH. W → Fed (no change exp) and Bank of Canada (no change exp) policy meetings; Earnings by Microsoft, Meta, Tesla, ASML, IBM, AT&T and Starbucks. Th → Earnings by Apple, Amazon, Visa, Mastercard and Caterpillar. F → US PPI inflation, Germany inflation, €-zone GDP; Earnings by Exxon, Chevron, Amex and Verizon.

See you tomorrow.

Copyright © 2025 Succinct.

All rights reserved. This publication contains proprietary content and is intended solely for the recipient’s personal use. Disclaimer: Our service is for informational purposes only and does not constitute personal financial advice.