Fri 27 Feb: After the Bell

Month-End Jitters: Hot (PPI) Inflation, Credit Stress and Rising Geopolitical Risk

Good evening,

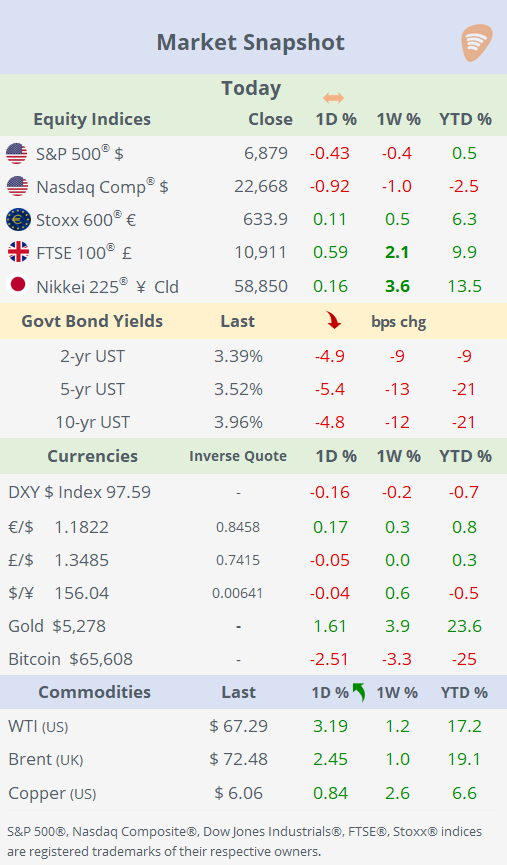

Stocks fell on the last trading day of February, closing out a volatile weekend and month-end as a hot US wholesale inflation (PPI) print, fresh stress in private credit, and rising geopolitical tensions combined to hit risk appetite. AI-linked equities again bore the brunt: the MAGS ETF fell 1.5% on the day and is now down 7% YTD, significantly underperforming the S&P 500 equal-weight index (+7%), underscoring how quickly enthusiasm around AI has given way to valuation and growth anxieties.

Concerns over private-credit exposures dragged financials to the bottom of the tape, with major US bank stocks falling between 5 and 7.5%, marking their worst session since April’s tariff turmoil and leaving the sector down 6% this year.

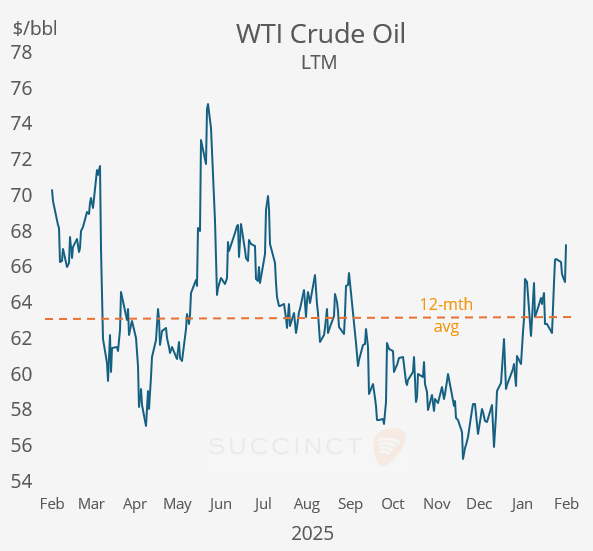

At the same time, geopolitical risk pushed oil prices higher as Washington-Tehran nuclear talks ended without a deal, while the risk-off move lifted bonds, sending 2-year Treasury yields (3.39%) to their lowest since August 2022, and reignited safe-haven demand, with gold and silver rallying sharply, silver jumping 7%. Long-end Treasury yields plunged ~30bp in February.

The week capped a turbulent stretch that also featured Supreme Court tariff rulings, shocks from the AI ecosystem, Nvidia’s earnings, and a sharp drop in Bitcoin, a reminder that volatility, not complacency, is setting the tone into March.

In geopolitics, Trump said the US has not made a final decision on striking Iran, stressing he would prefer to avoid military action but warning that “sometimes you have to.” He added that Washington is unhappy with Tehran’s negotiating stance and reiterated that Iran “cannot have nuclear weapons,” keeping geopolitical risk elevated despite no immediate action signal. This triggered a 3% rally in crude oil to the highest level since August.

Credit news: → London-based and privately-owned Market Financial Solutions (MFS UK, not related to MFS in the US) has collapsed into administration amid fraud allegations, triggering a scramble among Wall Street lenders to assess losses on roughly £2bn of financing and raising fresh concerns over underwriting standards in asset-backed credit. Banks and credit funds, including Barclays, Jefferies and Apollo, are exposed, with a potential collateral shortfall of up to £930mn, linked to alleged double-pledging and serious account irregularities. The episode has rattled lender stocks and revived memories of past credit blow-ups, as AlixPartners steps in as administrator and regulators and investors scrutinise whether risk discipline is again slipping in private credit markets. (FT)

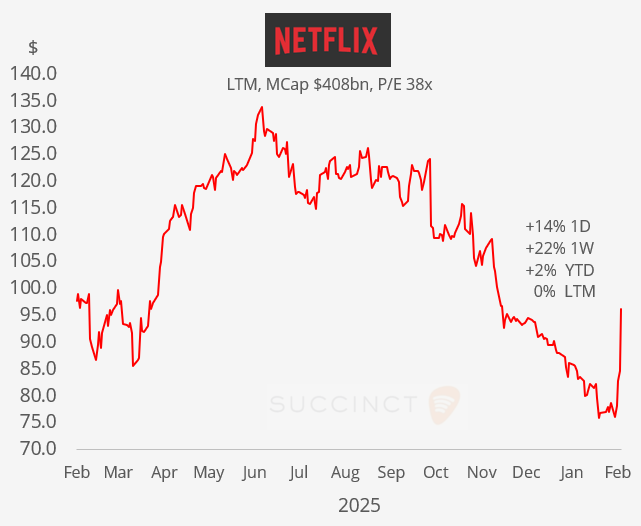

Notable mover: → Netflix (mcap $405bn) shares rallied sharply (14%) today after it declined to raise its bid for Warner Bros. Discovery, effectively clearing the way for Paramount Skydance’s higher offer to prevail in the bidding war. After the close, Paramount announced it had entered into a definitive agreement to acquire Warner Bros. (THR)

Earnings: → It was a quiet day for corporate results. European releases were mixed as Germany’s BASF (mcap €43bn) reported a 9.5% drop in full-year earnings and flagged a profit outlook that missed expectations, contributing to a ~2% stock decline, while Swiss-based Holcim (mcap $50bn, -1.4%) delivered strong recurring EBIT growth and margin expansion for 2025, though sales remained under pressure from currency effects.

Economics: → The US Producer Price Index (wholesale inflation) for January came in hotter than expected, rising 0.5% MoM vs 0.3% forecast and 2.9% YoY vs 2.6% consensus, with core prices also surprising to the upside, highlighting persistent wholesale inflation pressures. The stronger print weighed on risk assets and complicated the outlook for early Fed rate cuts, reinforcing the narrative that inflation remains more stubborn than markets had anticipated. (WSJ)

→ In the €-zone, inflation trends across these major economies show a mixed picture in February, cooling in Germany (1.9% YoY), acceleration in France (1.1%), and stable but slightly elevated rates in Spain (2.5%), suggesting that euro-area price pressures remain uneven rather than uniformly easing.

Corporate Deals: → In the ATM sector, The Brink’s Company (mcap $4.8bn) agreed to acquire NCR Atleos (mcap $3.4bn) in a $4bn cash-and-stock deal, combining two major ATM operators and adding 78,000 owned-and-operated ATMs to Brink’s network. Brink’s shares fell 15% while NCR Atleos jumped 8.5%.

→ In private markets, ChatGPT’s parent OpenAI finalised a funding round valuing the company at $730bn, raising $110bn in fresh capital led by Amazon ($50bn), NVIDIA ($30bn) and SoftBank Group ($30bn). The valuation marks a sharp step-up from a $500bn level implied by a secondary transaction in October 2025, and from an earlier 2025 primary raise of $40bn at roughly $300bn.

→ In the real estate sector, Canada’s CPP Investments and REIT Equinix (mcap $95bn) agreed a $4bn deal (incl. debt) to jointly acquire Nordic data-centre operator atNorth, strengthening their footprint in the region. CPP will invest $1.6bn for a 60% stake, Equinix will hold 40%, and Partners Group (Swiss private equity) will reinvest up to 10%, supporting CPP’s global data-centre strategy and Equinix’s Nordic expansion.

→ In IPO’s, Massachusetts-based Generate Biomedicines raised $400mn on Nasdaq at $16 a share, valuing the AI-drug developer at roughly $1.9bn. It had a weak debut, falling 21% below the IPO price, reflecting investor caution in volatile markets.

Week Ahead:

Data → T: €-zone inflation; F: US non-farm payrolls, employment and retail sales. Earnings → S: Berkshire H; T: CrowdStrike; W: Broadcom; Th: Costco. Monetary Policy → No central bank rate decision meetings scheduled.

That’s all for this week.

Copyright © 2026 Succinct.

All rights reserved. This publication contains proprietary content and is intended solely for the recipient’s personal use. Disclaimer: Our service is for informational purposes only and does not constitute personal financial advice.