Fri 30 Jan: After the Bell

Violent Month-End Unwind Hits Metals, Leaves Equities Flat on the Week....

ℹ️ Today’s tables & charts on the ‘Market Data’ post.

Good evening,

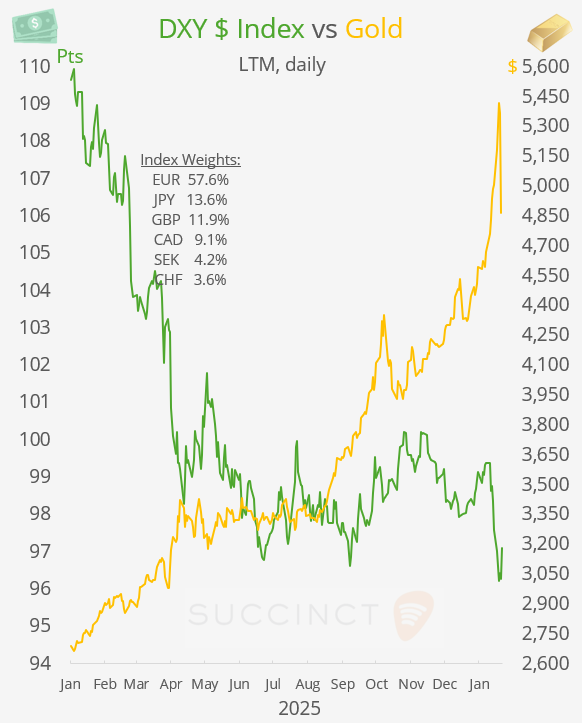

The week was defined by wild trading: equities tilted risk-off around the Fed and mega-cap earnings, while safe havens such as gold suffered abrupt reversals. Month-end flows drove another volatile session across markets. US equities fell for a third straight day, with the S&P 500 under pressure into the close, while precious metals saw a brutal unwind: silver suffered its worst one-day drop in roughly 45 years (-30%) and gold fell 11%, both retreating sharply from recent record highs as the entire metals complex was hit by violent position unwinds.

The $ strengthened 1% after investors finally received clarity on Trump’s pick for the Fed chair while the Treasury curve steepened both on the day and over the week as short-end yields moved lower.

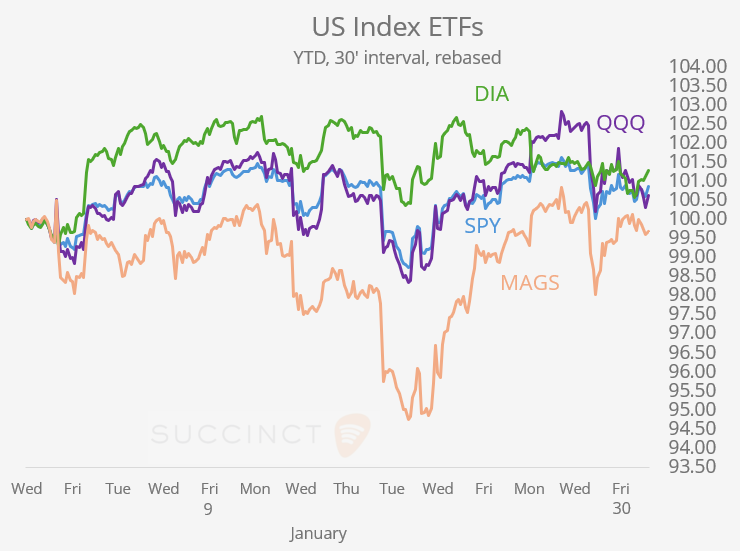

Weekly and monthly context: for the week, the S&P 500 and Nasdaq finished little changed, while the Russell 2000 lagged, ending 2% lower. In January sector performance, energy led on the back of crude’s recovery and a strong natural gas rally, followed by materials and consumer staples, while financials underperformed.

Central Banks: → Trump has formally nominated former Fed governor Kevin Warsh to succeed Jerome Powell as the next Chair, with Powell’s term set to expire in May 2026. The pick, which still requires Senate confirmation, ends months of speculation over the succession and, given Warsh’s Fed experience and reputation as an inflation hawk favouring tighter monetary policy, could signal a more restrictive bias under Trump’s second administration.

Earnings: → Exxon, Chevron and American Express all beat expectations with generally solid results, but Verizon’s stock surged ~11% after reporting better-than-expected Q4 earnings and revenue, driven by its highest postpaid subscriber additions in six years, robust broadband growth and upbeat 2026 profit and free-cash-flow guidance, along with a $25bn share buyback plan.

Economics: → US PPI inflation for December showed a stronger-than-expected pickup, with headline producer prices rising 0.5% MoM, the largest monthly gain in three months, and up 3.0% YoY, above the ~2.7% expected; core PPI (ex food/energy) also jumped to 3.3% YoY and 0.7% MoM, both beating forecasts, underscoring persistent wholesale inflation pressures. The hotter PPI print reinforces concerns that inflation pressures remain elevated and may feed into consumer inflation, complicating the Fed’s disinflation narrative and supporting cautious pricing of future policy moves.

→ Germany’s prelim January inflation rose to 2.1% YoY, above December’s 1.8% and slightly above expectations, signalling a modest uptick in price pressures near the ECB’s 2% target.

→ €-zone prelim GDP data showed the economy expanded by 1.3% YoY in Q4’25, slightly above expectations and confirming steady if modest growth as domestic demand offsets external headwinds.

Corporate Deals: It was a quiet day for M&A. No major US or EU transactions were formally announced.

→ OnlyFans is in exclusive talks to sell a ~60% stake to San Francisco–based Architect Capital, in a deal valuing the equity at about $3.5bn (around $5.5bn including debt). The discussions are advanced but not final, and the transaction could still fall through, according to people familiar with the matter.

→ In IPOs, Asta Energy Solutions AG, an Austrian copper-based products maker, completed its IPO on the Frankfurt Stock Exchange today, raising about €165m (€190m including greenshoe) in its debut and saw its shares jump ~46% above the issue price on first trading. It was priced at €29.5 per share and a €420mn valuation. The company produces copper solutions for energy transmission, transformers and industrial applications, and this was the first IPO of 2026 in Frankfurt’s Prime Standard segment.

Week Ahead:

Monetary Policy → T: RBA, Thu: ECB, BoE. Data → W: €-zone inflation, F: US non-farm payrolls. Earnings → M: Palantir, Disney. T: ADM, Merck, Pepsi, Amgen, Pfizer. W: Alphabet, Eli Lilly, Uber, Qualcomm. Th: Amazon, Shell, Unilever, PM, BNP.

That’s all for this week.

Copyright © 2025 Succinct.

All rights reserved. This publication contains proprietary content and is intended solely for the recipient’s personal use. Disclaimer: Our service is for informational purposes only and does not constitute personal financial advice.