Fri 6 Feb: After the Bell

Wall Street Bounces Back, Nvidia Leads, Dow Breaks 50,000 ...

ℹ️Find more performance tables here.

Good evening,

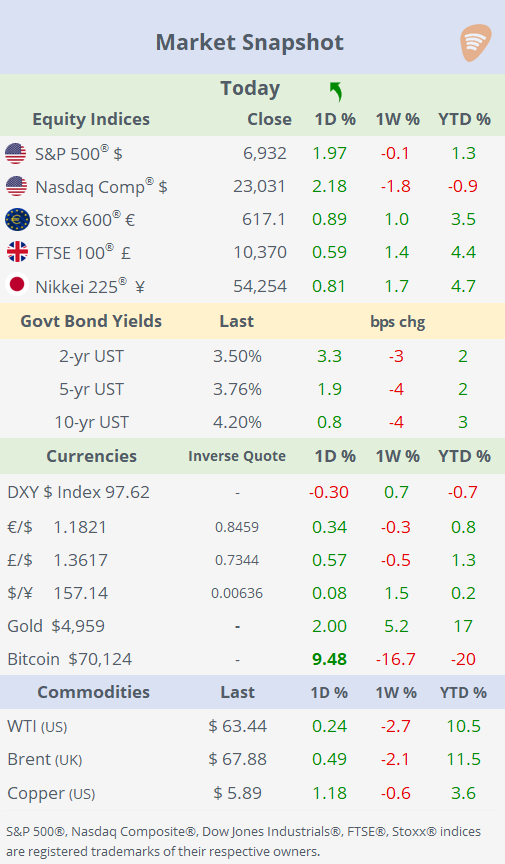

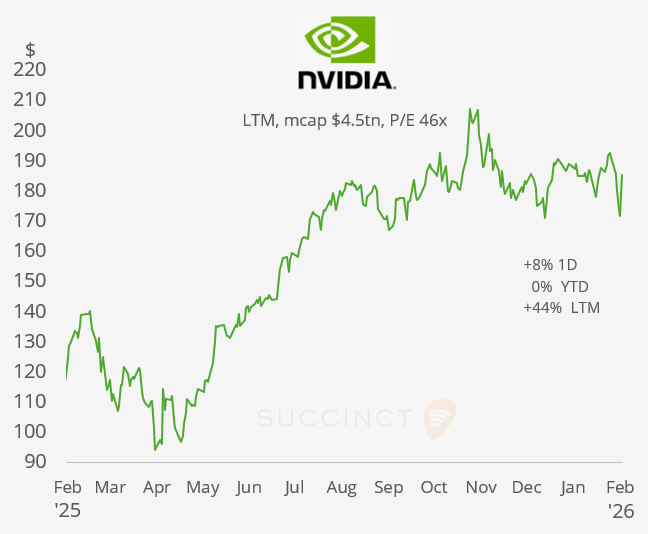

Markets closed a highly volatile week on a positive note, with US equities staging a sharp rebound after several days of heavy selling. The S&P 500 and Nasdaq Composite both rose around 2% on Friday, helped by an 8% surge in Nvidia, while the Dow Jones pushed above 50,000 for the first time and the Russell 2000 jumped 3.6%, signalling a broad-based recovery. Investors reassessed fears around AI disruption and outsized Big Tech capex, arguing that the recent drawdown had overshot underlying fundamentals, with resilient growth, solid earnings and an improvement in consumer sentiment, the University of Michigan index at its best level since August, supporting risk appetite.

Despite Friday’s bounce, the week remained mixed: the Dow ended up 2.5%, while the S&P 500 and Nasdaq still finished in the red. In single names, transatlantic automaker Stellantis plunged 24% after warning of a €22bn charge tied to scaling back its EV strategy. The stock lost 52% in the past twelve months.

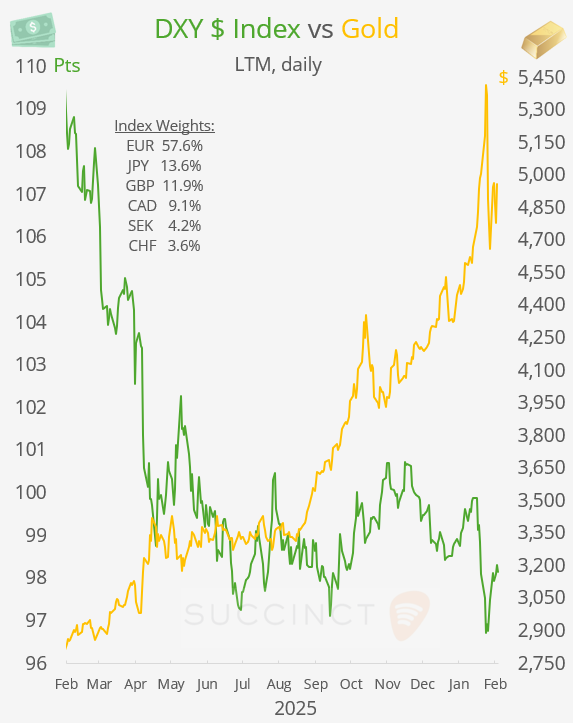

In other asset classes, Bitcoin rebounded toward $70,000 after its sharpest sell-off since 2022, though it still fell 17% over the past week. The $ softened on Friday amid the risk-on move but ended the week firmer overall, mainly against the ¥, while Treasury yields were relatively stable, finishing 4–5bp lower across the curve as markets continue to price in an 80% probability of no Fed rate change in March.

Earnings: → It was a quiet day. Philip Morris, Societe Generale and Ubiquiti Inc all reported results, with Ubiquiti standing out on the upside as shares rallied 8% on stronger-than-expected results and positive guidance, while SocGen traded slightly lower and Philip Morris remained largely flat as its report lacked fresh catalysts.

Monetary Policy: → The Reserve Bank of India held its repo rate at 5.25% as expected, maintaining a neutral stance and signalling a pause in its easing cycle as inflation remains contained and economic growth proves resilient. Policymakers highlighted a benign inflation outlook and supportive growth momentum, keeping future rate moves dependent on incoming data amid global uncertainties.

Economics: → The US Michigan Consumer Confidence climbed to 57.3, the best reading since August, pointing to improving household sentiment and resilience despite elevated rates and recent market volatility.

→ Canada unexpectedly lost 24,800 jobs in January, well below expectations for job gains, even though full-time positions rose modestly in the month. Despite the decline in employment, the unemployment rate fell to 6.5%, the lowest in 16 months, largely because fewer people were actively searching for work, signalling a softening labour market alongside still-tight jobless conditions.

Corporate Deals: A calm day for M&A deals.

Regarding IPOs, Once Upon a Farm (OFRM), a California-based children’s organic food company, raised $198mn in its IPO priced at $18 per share, implying a valuation of roughly $720mn at listing. Shares rallied about 17% on debut, reflecting strong investor appetite for branded consumer staples with growth potential.

→ SpyGlass Pharma, an eye-care biopharmaceutical company, raised $150mn in its IPO priced at $16 per share, implying a valuation of $550mn at listing. Shares surged about 65% on debut, also underscoring strong investor appetite for late-stage healthcare names.

Week Ahead:

Data → T: US retail sales, China inflation; W: US non-farm payrolls (Jan); Thu: UK GDP, US existing homes sales; F: US CPI inflation.

Earnings → M: Unicredit, Apollo; T: Coca-Cola, AstraZeneca, BP, S&P; W: Cisco, McDonald’s, Shopify, TotalEnergies; Th: Applied Mat, Siemens, L’Oreal, Hermes, Unilever, Airbnb, Coinbase.

That’s all for this week.

Copyright © 2025 Succinct.

All rights reserved. This publication contains proprietary content and is intended solely for the recipient’s personal use. Disclaimer: Our service is for informational purposes only and does not constitute personal financial advice.