Fri 6 Mar: After the Bell

War Escalation Triggers Global Risk-Off, Oil Rallies

ℹ️Today’s Performance tables.

Good evening,

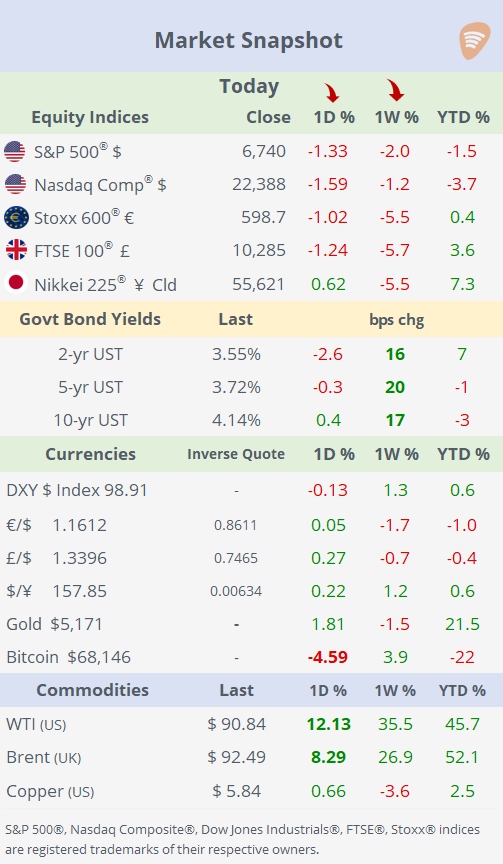

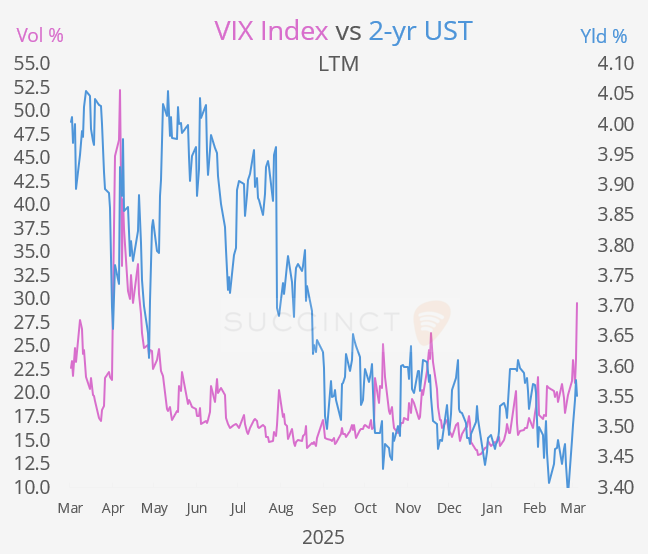

Global markets ended the week firmly in risk-off mode as the Middle East conflict intensified and weak US labour data deepened concerns about the economic outlook. Equities fell across the US and Europe on Friday, capping a difficult week in which the Dow Jones declined about 3% and the Euro Stoxx 50 dropped nearly 7%, while the € weakened almost 2% against the $. The Vix index jumped to 29.7%, the highest level since April.

A surprisingly weak US non-farm payrolls report showed a loss of 92,000 jobs in February, far below expectations, reinforcing signs of a softening employment market.

Geopolitics remained the dominant driver of markets. Trump said there would be no agreement with Iran short of “unconditional surrender,” raising fears that the conflict could broaden further. At the same time, Israel continued strikes on Hezbollah infrastructure in southern Beirut, while Gulf producers warned that the war could severely disrupt energy flows. Qatar cautioned that the conflict could force Gulf states to halt energy exports within days, after declaring force majeure at its Ras Laffan LNG facility following recent attacks. Meanwhile, Kuwait cut oil production as congestion built across the Persian Gulf, with the Strait of Hormuz, responsible for roughly a fifth of global oil and LNG shipments, becoming increasingly constrained and regional storage facilities rapidly filling.

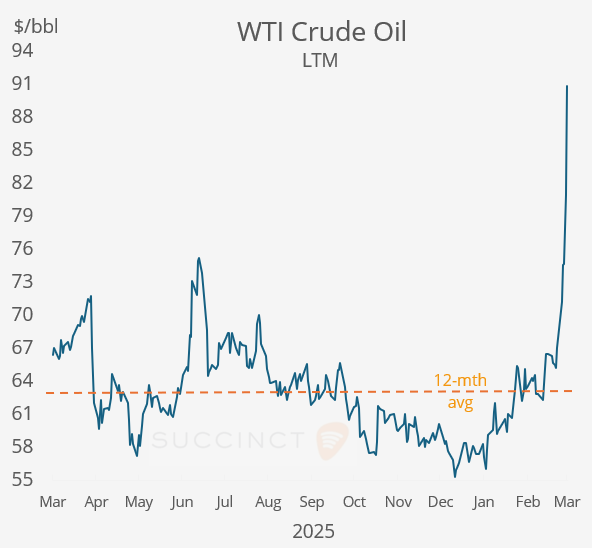

Energy markets reacted sharply. Oil prices surged above $90 per barrel, with WTI jumping 13% on Friday and posting its biggest weekly gain (35%) since at least 1985 as the conflict disrupted key export routes. Despite the energy rally, broader equity performance remained weak: in the US, materials, consumer staples, healthcare and industrials were the worst-performing sectors this week, each falling roughly 4–6%, while energy was the only sector to finish higher, up about 1%.

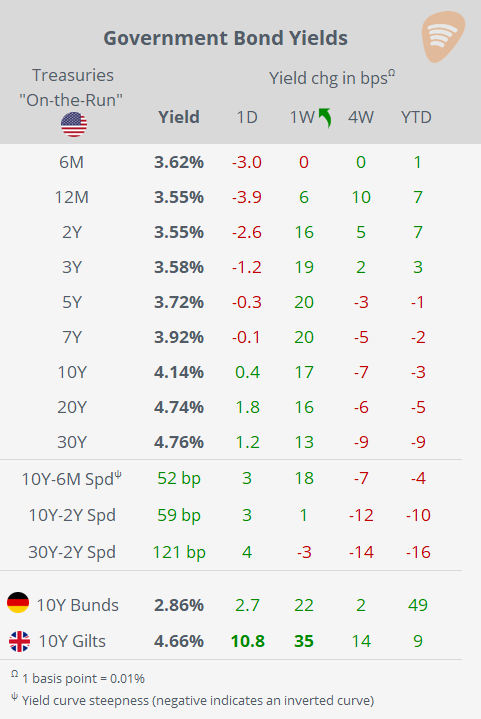

In fixed income, Treasury yields fell marginally on Friday, reversing part of the recent sell-off as investors reacted to the weak jobs data, though yields still ended the week significantly higher. Markets are increasingly pricing the risk that sustained oil price gains will feed into inflation, with 3-, 5- and 7-year Treasury yields rising about 20 basis points over the week.

Economics: → The US labour market weakened in February, with non-farm payrolls falling by 92k, sharply missing expectations for a ~50k gain and reversing January’s 126k increase. The unemployment rate edged up to 4.4% from 4.3%, while private-sector employment also declined, highlighting broader softness in hiring. The report indicates a cooling labour market following several months of weak job growth.

The implied probability of a rate cut by the Fed rose to 20% for the April meeting (not the upcoming one in 11 days), from 11% before the release. Still, the Fed is unlikely to cut rates soon as the Iran-driven oil price shock risks reigniting inflation, leaving policymakers in a difficult balancing act.

→ US retail sales fell 0.2% MoM in January (vs −0.3% expected) but remained up ~3% YoY, suggesting a modest short-term pullback in consumer spending while underlying demand stays relatively resilient.

→ China set its 2026 GDP growth target at 4.5–5%, the lowest range in decades and slightly below last year’s “around 5%” goal, as leaders warned of rising economic challenges at home and abroad. Beijing signalled a more cautious policy stance, maintaining a relatively high fiscal deficit and boosting defence spending by 7%. Officials acknowledged ongoing weakness in the property market and employment pressures, while emphasising long-term priorities such as technological development and resilience amid geopolitical tensions and global economic slowdown. Beijing will release inflation data on Sunday.

Corporate Deals: Friday was surprisingly active for M&A announcements.

→ In Japan’s auto sector, Denso Corp (mcap $35bn) has proposed acquiring Rohm Co (mcap $8bn) in a deal valuing the power-chip maker at ¥1.3tn ($8.2bn), an 18% premium to its prior close. Rohm shares gained 18% today and 46% YTD. The takeover would strengthen Japan’s position in power semiconductors critical for EVs and autonomous driving, aligning with government efforts to consolidate the sector amid rising competition from Chinese chipmakers.

→ In the healthcare sector, French privately held Servier agreed to acquire California-based Day One Biopharmaceuticals (mcap $2.2bn) for $2.5bn in cash ($21.50/share, 68% premium), expanding its rare oncology portfolio and strengthening its pipeline in pediatric and adult cancer treatments, including pediatric low-grade glioma. Day One shares jumped 66% today. (Reuters)

→ In private markets, the Intercontinental Exchange, owner of the NYSE, has taken a stake in crypto exchange OKX in a deal valuing the platform at $25bn, marking a push by traditional market operators into digital assets. The partnership will support the launch of US-regulated futures tied to OKX crypto prices, as ICE expands into tokenised assets and blockchain-based market infrastructure. (OKX)

→ German publisher Axel Springer agreed to acquire Telegraph Media Group (publisher of The Daily Telegraph) for £575m (~$766m) in cash, ending a lengthy ownership process for the British newspaper group.

→ In IPOs, MiniMed Group, a diabetes medical-technology company headquartered in Northridge, California, completed its IPO on the Nasdaq, raising $560mn after pricing at $20 each, implying a $5.6bn valuation at the IPO price. The company, a carve-out from Medtronic, develops insulin pumps and glucose-monitoring systems for diabetes management. Shares fell 7.5% on their debut.

Week Ahead:

Data → S: China inflation; T: US existing home sales, China trade; W: US inflation; Th: US housing starts; F: US personal income and spending, JOLTs, Michigan consumer sentiment, durable goods; UK GDP.

Earnings → M: HP; T: Oracle; W: Foxconn; Th: Adobe, BMW.

That’s all for this week.

Copyright © 2026 Succinct.

All rights reserved. This publication contains proprietary content and is intended solely for the recipient’s personal use. Disclaimer: Our service is for informational purposes only and does not constitute personal financial advice.