Mon 10 Nov: After the Bell

Your 5’ evening market wrap 📄📈

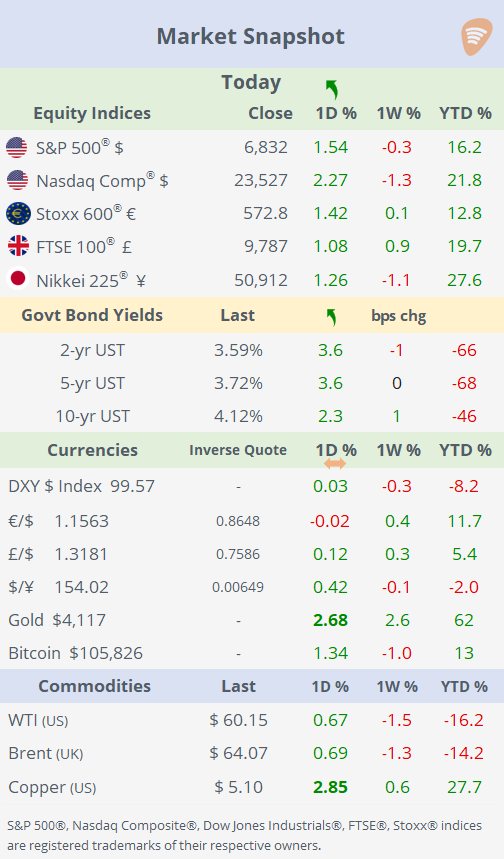

→ Indices + Large Caps + FX + Treasuries + Commodities tables on the ‘Market Data’ post.

Good evening,

The record-long US government shutdown appears close to ending, fueling a broad-based market rally. The Senate cleared a key hurdle late Sunday, with Democrats providing just enough votes to advance a funding measure. The next step is for the Republican-led House to consider and approve the bill.

Once the shutdown ends, expect a surge of delayed economic data releases, including jobs, inflation, and fiscal reports, which could impact markets. Moreover, government workers who have missed paychecks may finally receive their wages, potentially supporting a boost in consumer spending.

Renewed interest in AI-related stocks drove markets higher, with Nvidia up nearly 6% and Palantir gaining 9%. The rally in mega-cap tech led to a clear outperformance of the market-cap weighted S&P 500 (+1.5%) compared with its equal-weight version (+0.6%). The Nasdaq Composite gained over 2% today and recovered 4% from its Friday intraday low when a weak consumer confidence print triggered a selloff.

Gold rose nearly 3% (and Silver ~5%), supported by expectations that the Fed may inject liquidity into the system to offset the partial drain caused by the government shutdown, which increased demand for hard assets.

Currency markets had a calm session, with the DXY $ index closing unchanged. The Australian dollar outperformed, supported by signs of easing tensions between the US and China. Core bond yields rose modestly, with the Treasury curve shifting up by ~3bp; futures still imply a 65% chance of a Fed rate cut in December, while the curve’s shape and steepness have changed little in recent weeks (see Market Data for chart).

No major earnings releases or relevant market-moving economic data were reported today.

Business News: → Warren Buffett (95), the outgoing CEO of Berkshire Hathaway (mcap $1tn), will no longer write the company’s annual letter or speak at the shareholder meeting. His February letter marked his 60th and final edition. Shares are 10% higher YTD versus +16% for the S&P 500.

→ Tesla (mcap $1.48tn) announced leadership changes affecting its Cybertruck and Model Y programs, as both unit heads are departing the company. The moves come amid ongoing production and sales pressures across its key vehicle lines. Shares jumped almost 4% today.

Data released over the weekend: China’s CPI inflation rose 0.2% YoY in October, reversing September’s 0.3% decline and marking the fastest pace since January. Producer price inflation (PPI) remained negative at -2.1% YoY but showed a slight moderation from the previous month.

Deals: The week got off to an active start for M&A and private markets transactions.

→ Apollo Sports Capital, the $5bn investment arm of Apollo Global, agreed to acquire a majority stake (~55%) in Atlético Madrid, Spain’s third-largest football club, in a deal valuing the team at €2.5bn including debt. Existing shareholders, CEO Gil Marín, chair Enrique Cerezo, Ares Mgt and Quantum Pacific, will sell down part of their holdings but remain invested.

→ British private equity firm Permira has agreed to acquire UK-listed fund administrator JTC Plc (mcap £2.2bn) in a £2.7bn deal including debt. The offer represents a 49% premium to JTC’s closing price on Aug 13, the day before Permira made its first bid. JTC provides administrative services across investment funds, including private equity, real estate, and credit. JTC shares are 32% higher YTD and are trading near their all-time high.

→ In private markets, Vancouver-based Legal AI company Clio raised $500mn in a funding round led by New Enterprise Associates, giving the company a $5bn valuation. The round marks a significant milestone for the firm, which develops AI-driven software for legal services.

→ Finally, KKR has agreed to sell aerospace and defence hardware maker Novaria Group to Arcline Investment Mgt for $2.2bn. Arcline, an industrials-focused private equity firm, will take ownership of Novaria, marking a significant transaction in the defence manufacturing sector.

Day Ahead: On Tuesday, the US bond market will be closed for Veterans Day, while stock markets will be open.

→ Data: US ADP weekly employment change (not suspended), UK employment, Germany ZEW indicators, Brazil inflation.

→ Earnings: Occidental Petroleum, Softbank, Munich Re and Vodafone.

See you tomorrow.

Copyright © 2025 Succinct.

All rights reserved. This publication contains proprietary content and is intended solely for the recipient’s personal use. Disclaimer: Our service is for informational purposes only and does not constitute personal financial advice.