Mon 13 Apr: After the Bell

Risk Assets Rise Despite Strait of Hormuz Escalation

Good evening,

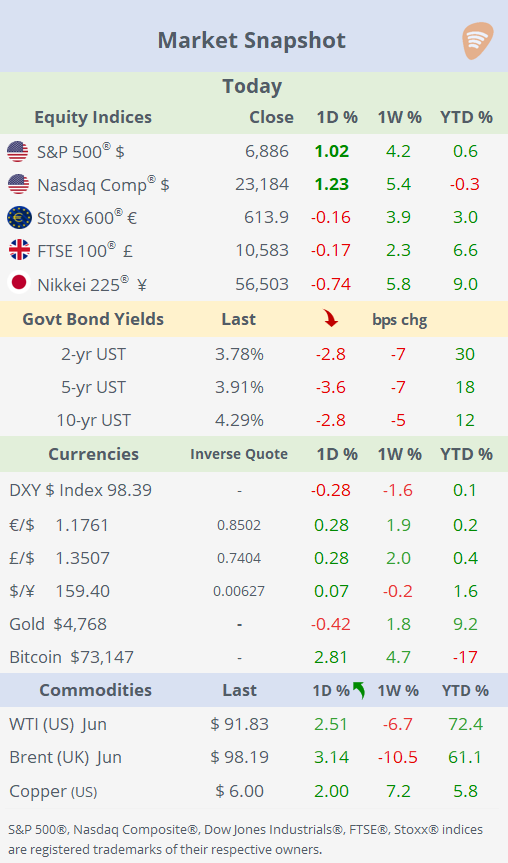

Weekend negotiations between Washington and Tehran failed to deliver a breakthrough, prompting a sharp escalation in tensions as the US formally launched a military blockade of the Strait of Hormuz. Trump warned that any Iranian fast-attack vessels approaching the exclusion zone would be destroyed, while reports indicated more than 15 American warships had been deployed to support the operation. Maritime advisories also confirmed access restrictions around Iranian ports and nearby Gulf waters.

The blockade has intensified fears of an oil supply shock, with some of the last pre-conflict cargoes from the Gulf now en route to global refineries. Brent rose 3% on the day as markets priced in tighter near-term supply and renewed geopolitical risk, reinforcing concerns over energy inflation and global growth.

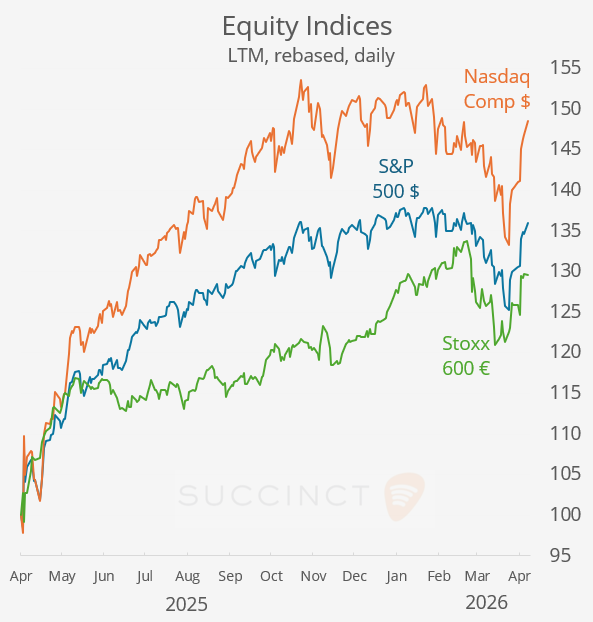

Despite the escalation, Wall Street equities mounted an impressive reversal. Major indices erased early losses after Trump said Iran had contacted his administration on Monday morning “to work out a deal,” reviving hopes that diplomacy may still be possible. Indices finished more than 1% higher, led by technology and financial shares.

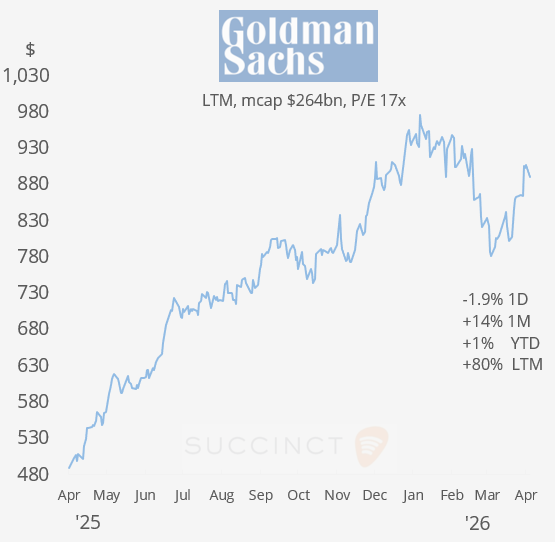

Single-stock moves remained mixed, with Goldman Sachs falling 2% despite reporting solid earnings, as investors focused more on the uncertain macro and geopolitical scenario.

Economics: → US Existing Home Sales fell 3.6% MoM in March to 3.98mn annualised units, below expectations (~4.05–4.07mn) and marking the weakest pace in nine months, signalling a soft start to the spring selling season. Sentiment is modestly negative, as higher mortgage rates, affordability pressures and weaker consumer confidence continue to restrain demand, though limited inventory is still supporting home prices.

→ India’s CPI rose to 3.4% YoY in March (from 3.21% in February), broadly in line with expectations, as higher food and fuel costs lifted prices, though inflation remains below the Reserve Bank of India’s 4% target, supporting a steady policy stance for now.

Earnings: → Goldman Sachs reported a strong Q1, with profit rising 19% to $17.55/share (above estimates) and revenue up 14% to $17.23bn, driven by record banking & markets revenue, a 48% jump in investment-banking fees, and solid trading activity. However, shares fell 2% on the day as strong backwards-looking results were overshadowed by management caution that the Iran conflict and elevated uncertainty could slow IPOs, M&A and broader Wall Street activity later this year. The Q1 earnings season officially starts tomorrow with other mega-banks reporting. (CNBC)

Deals: → In the US bedding sector, Kentucky-based Somnigroup International (mcap $16bn), agreed to acquire Missouri-based Leggett & Platt (mcap $1.53bn) in a $2.5bn all-stock deal, vertically integrating a key supplier into its mattress and bedding empire. Leggett shares gained 12% today and 64% in the LTM. (WSJ)

→ In Canada’s waste management sector, Ontario-based GFL Environmental has agreed to acquire Secure Waste Infrastructure (mcap $3.5bn), a listed Calgary-based industrial waste and energy infrastructure operator, in a deal worth CAD 6.4bn (~$4.6bn) including debt. The transaction expands GFL’s footprint in Western Canada and adds Secure’s network of landfills, treatment facilities, recycling assets and injection wells, highlighting continued consolidation in the waste management / environmental services sector.

→ In private markets, Leonard Green & Partners is nearing a deal to acquire NY-based construction project manager Cumming Group from New Mountain Capital in a transaction valuing the business at ~$3bn, including debt. The deal highlights continued private equity appetite for business-services assets with stable cash flows, even as broader sponsor-backed mid-market deal activity remains subdued amid higher interest rates.

→ In IPOs, the US pipeline is reopening despite market volatility, with ~$15bn of offerings expected to debut, signalling improving risk appetite after a slow start to 2026. Recent filings span biotech, real estate and industrial names, while bankers look to rebuild momentum ahead of larger marquee deals. A major focal point is Bill Ackman, who has launched a roadshow for the combined IPO of Pershing Square Capital Management and Pershing Square USA, seeking to raise $5bn–$10bn on the NYSE, potentially one of the year’s largest listings, ahead of the widely anticipated SpaceX IPO expected in June. (Reuters)

Day Ahead:

Data → US PPI, ADP employment change; Germany wholesale prices; China balance of trade. Earnings → JPM, Citi, Wells Fargo, BlackRock, J&J, BMW.

See you tomorrow.

Copyright © 2026 Succinct.

All rights reserved. This publication contains proprietary content and is intended solely for the recipient’s personal use. Disclaimer: Our service is for informational purposes only and does not constitute personal financial advice.