Mon 15 Dec: After the Bell

Wall Street Slips as Investors Brace for Labour Data. Your 5’ evening market wrap📄📈

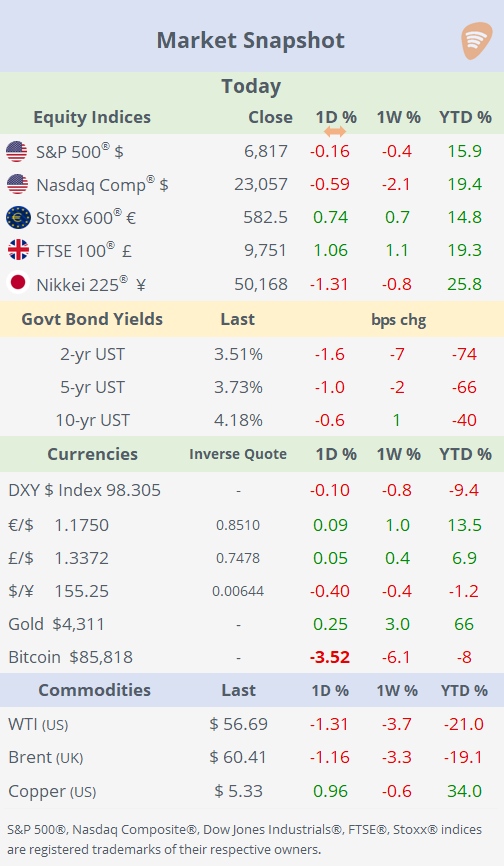

ℹ️ Today’s performance tables & charts on the ‘Market Data’ post.

Good evening,

Wall Street opened the final full trading week of the year on a cautious footing, with attention firmly shifting to Tuesday’s delayed US employment report. Equity futures pointed to a rebound ahead of the open, up around 0.5% after Friday’s sharp sell-off, but the early strength faded through the session. Stocks reversed lower by midday, with technology leading the decline and Nasdaq indices falling to their lowest levels in three weeks. Sector performance was mixed, with healthcare outperforming and IT the clear laggard, though overall moves were contained.

Forex and bond markets were largely unchanged as investors stayed on the sidelines ahead of the labour data. Markets are now pricing a roughly 78% probability that the Fed leaves rates unchanged at its late-January meeting, up from about 68% a week ago following the December cut and Powell’s comments.

In commodities, crude oil slid more than 1%, pressured by weak Chinese economic data released over the weekend, which outweighed ongoing geopolitical supply risks linked to Russia-Ukraine and Venezuela. Risk-off sentiment also extended to digital assets, with Bitcoin trading well below the $90,000 level once again.

A notable large-cap mover was software provider ServiceNow (mcap $160bn, P/E 92x), which plunged 11% (-28% YTD) after Bloomberg reported advanced talks to acquire Internet of Things cybersecurity firm Armis for up to $7bn, ServiceNow’s largest deal ever, sparking investor concerns over the premium price tag and dilution risk.

Business News: → Ford (mcap $54bn) said it will take about $19.5bn in charges mainly related to its electric-vehicle business, a massive hit as it retrenches amid weak EV demand. The impairment, one of the largest ever, underscores the US auto industry’s struggle to make EV ambitions profitable. Ford, having already lost $13bn since 2023, plans to strengthen gas-powered models and pivot toward hybrids and extended-range EVs with onboard engines. Shares barely moved today, but are 38% higher YTD.

Data: → China’s latest data disappointed across the board: industrial production rose 4.8% YoY, well below expectations, while retail sales slowed sharply to 1.3% YoY, underscoring weak domestic demand. Fixed-asset investment also came in soft, signalling subdued momentum in infrastructure and property spending. Overall, the figures reinforce concerns about an uneven recovery and strengthen the case for further policy support.

→ Canada’s November CPI rose 2.2% YoY, matching October’s pace and slightly below the 2.3% consensus forecast. The loonie did not move today and remains ~4% stronger YTD.

Deals: → Italian football club Juventus shares surged up to 17% to value the club at €980mn after Tether, the parent of the USDT crypto stablecoin, proposed an all-cash bid for Exor’s 65.4% stake plus €1bn investment. Exor, the Agnelli family holding company, unanimously rejected the unsolicited offer. Juventus shares are 15% lower this year.

→ Zoetis, the leading animal health company (mcap $53bn), plans to raise $1.75bn (plus $250mn greenshoe) via 3.5-year convertible senior notes due 2029. Shares advanced 2% today, but are 26% lower YTD.

→ Japan’s MUFG (mcap $187bn) is in final talks to acquire a 20% stake in India’s Shriram Finance (mcap $17bn) for over $3.2bn, with an announcement possible this week, according to Bloomberg. Japanese banks pursue overseas growth amid a shrinking domestic market. Shriram shares surged 48% YTD.

Day Ahead: → Data: US non-farm payrolls, unemployment rate (Nov), retail sales, housing starts; EU & US Flash PMIs; UK unemployment rate.

See you tomorrow.

Copyright © 2025 Succinct.

All rights reserved. This publication contains proprietary content and is intended solely for the recipient’s personal use. Disclaimer: Our service is for informational purposes only and does not constitute personal financial advice.