Mon 16 Mar: After the Bell

Stocks Rally as Oil Drops and AI Optimism Lifts Tech

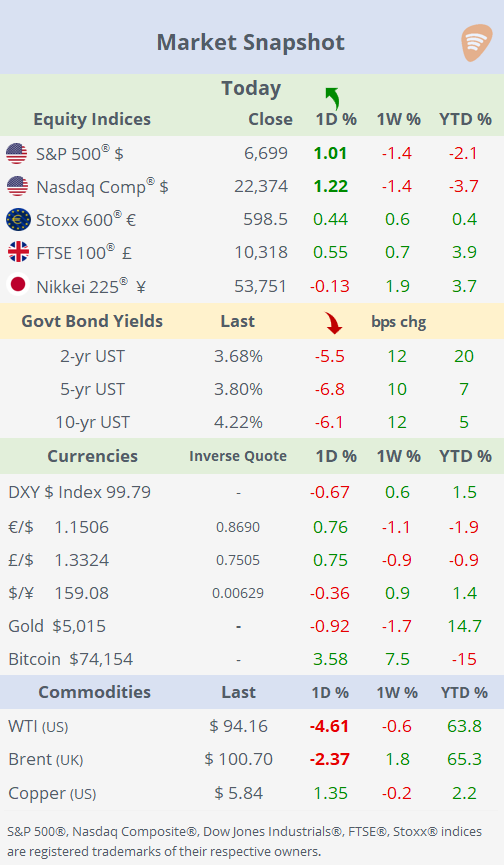

ℹ️ Today’s performance tables.

Good evening,

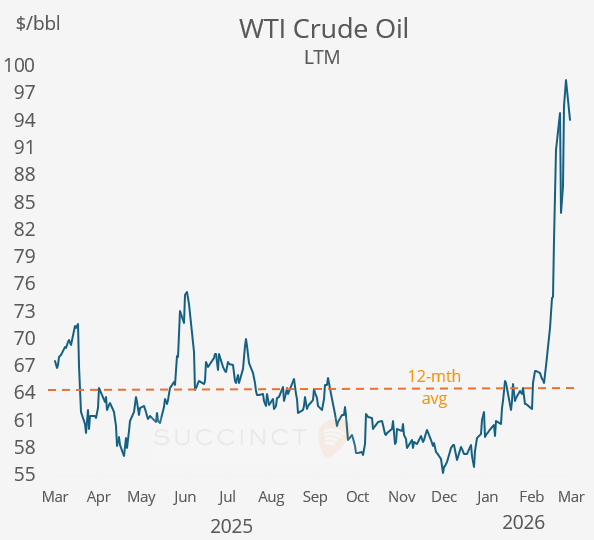

US equities rallied on Monday as oil prices retreated and investors embraced a broader risk-on tone across markets. WTI crude fell about 5% after a volatile session, as efforts intensified to restore oil flows through the Strait of Hormuz, the critical waterway that Iran has effectively closed. Trump said “numerous countries” were moving to help reopen the passage, though allies including Germany and the UK signalled reluctance to be drawn deeper into the conflict, while Japan and France dismissed the prospect of sending naval vessels to the region.

The geopolitical backdrop will remain front and centre for policymakers this week, which brings a dense calendar of central-bank decisions from the Fed, the ECB, the BoJ and the BoE. Trump also renewed pressure on the Fed, urging chair Powell to cut rates “right now” and suggesting the central bank hold an emergency meeting to ease policy.

Technology stocks led the market higher as investors focused on the start of Nvidia GTC, where CEO Jensen Huang unveiled a series of AI updates, including a space-optimised version of the Vera Rubin data-centre chip and reiterated expectations that AI chips could generate $1 trillion in revenue by 2027. The bullish outlook lifted the information-technology sector and reinforced risk appetite across markets: the DXY Index slipped below 100, while Treasury yields jumped after several sessions of declines.

Economics: → On Sunday, China released macro data. Its latest activity showed a stronger-than-expected start to the year, with industrial production rising 6.3% YoY in Jan–Feb, accelerating from 5.2% previously and beating forecasts of around 5%. Retail sales increased 2.8% YoY, also above expectations and up from 0.9% in December, helped in part by Lunar New Year spending. The figures suggest manufacturing momentum remains solid, though consumption growth, while improving, continues to lag, underscoring the still uneven nature of China’s economic recovery.

→ Canada’s February inflation data came in softer than expected, with headline CPI rising 1.8% YoY, down from 2.3% in January and slightly below the 1.9% consensus. Core inflation also cooled, with the Bank of Canada’s preferred core measures easing to around 2.3% YoY from 2.6%, broadly undershooting expectations. The data point to moderating price pressures and mark the slowest headline inflation since mid-2025, helped by energy price declines and base effects, keeping inflation comfortably within the Bank of Canada’s 1–3% target range.

→ US industrial production rose 0.2% MoM in February, slowing from 0.7% in January but slightly beating expectations of around 0.1%. Output increased 1.4% YoY, easing from about 2.3% previously, pointing to modest but still positive industrial momentum. The gain was supported by increases in manufacturing and mining output, though the broader trend suggests steady but not accelerating growth in the industrial sector.

Corporate Deals: → In Europe’s banking sector, UniCredit Spa (mcap €92bn) launched a €35bn takeover bid for Commerzbank AG (mcap €36bn), at €30.8 per share (~4% premium) as CEO Andrea Orcel pushes to build a cross-border European banking group. The Italian lender already holds ~29% of Commerzbank but faces opposition from both the bank’s management and the German government, which still owns over 12% and prefers the bank to remain independent. CBK shares gained >8% in Frankfurt but remain 11% lower this year.

→ In America’s storage sector, Public Storage (mcap $51bn) agreed to acquire National Storage Affiliates (mcap $6bn) in a $5.6bn all-stock deal ($10.5bn including debt), creating a self-storage group with a $57bn market value. The transaction will add 1,000+ properties across 37 US states and Puerto Rico, expanding Public Storage’s footprint in high-growth regions such as the Sun Belt; closing is expected in Q3. National shares jumped 30% today to the highest level since Sep 2024.

→ Nasdaq-listed Nebius Group (mcap $33bn), a Netherlands-based AI infrastructure provider spun out of Yandex, signed a five-year deal worth up to $27bn to supply AI data-centre capacity to Meta. The agreement includes $12bn of dedicated compute capacity plus up to $15bn of additional capacity, with Nebius deploying next-generation AI systems from Nvidia as Meta scales its global AI infrastructure. Nebius rallied 15% today to an all-time high and accumulated a 55% YTD gain.

Day Ahead:

Data → RBA and Bank Indonesia rate decision; US ADP employment change, pending home sales. Earnings → Lululemon.

See you tomorrow.

Copyright © 2026 Succinct.

All rights reserved. This publication contains proprietary content and is intended solely for the recipient’s personal use. Disclaimer: Our service is for informational purposes only and does not constitute personal financial advice.