Mon 2 Feb: After the Bell

Equities Firm as Commodities Unwind (Oil, Gas, Gold, Silver). Your 5’ evening market wrap....

ℹ️ Today’s tables & charts on the ‘Market Data’ post.

Good evening,

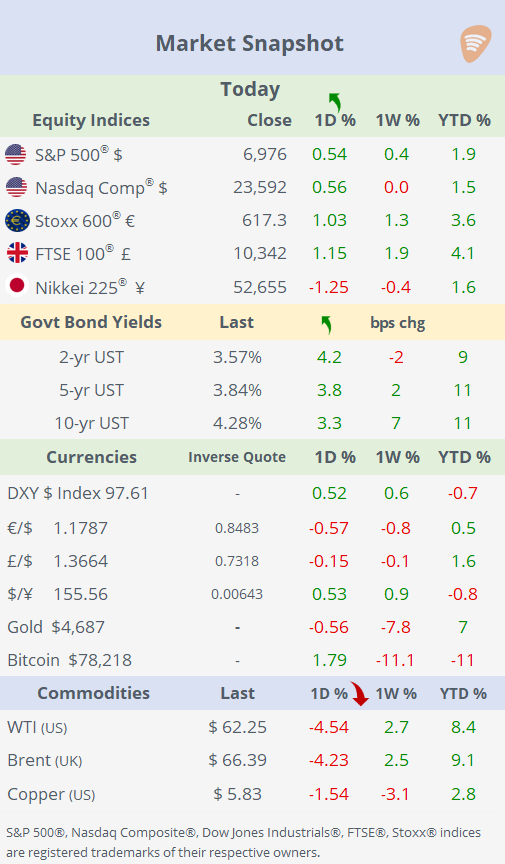

Stocks kicked off February in risk-on mode, with US equities pushing toward record highs after a strong ISM manufacturing PMI signalled a return to expansion and reinforced confidence in US growth. Geopolitical risk also eased, with renewed Iran talks and a trade agreement with India lowering tensions.

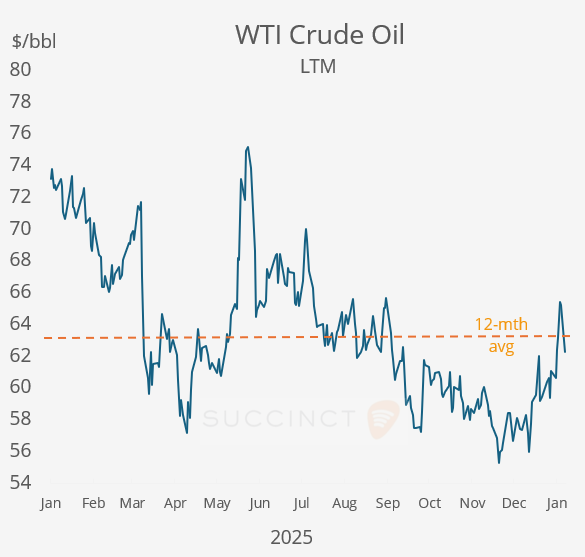

Commodities, by contrast, delivered another bout of volatility: silver whipsawed more than 20% intraday from Asian hours onward, while oil and gold sold off sharply, extending a turbulent start to the month across raw materials. Crude oil prices plunged (~5%) as markets stripped out a geopolitical risk premium following signs of renewed Washington-Tehran dialogue, easing fears of supply disruptions in the Middle East. With tensions cooling around the Strait of Hormuz, traders unwound long positions built on conflict risk, accelerating a sharp one-day selloff.

US natural gas prices crashed (-25%) as weather forecasts shifted sharply toward warmer-than-expected conditions, cutting anticipated heating demand after a recent cold-snap-driven rally and reducing near-term consumption expectations.

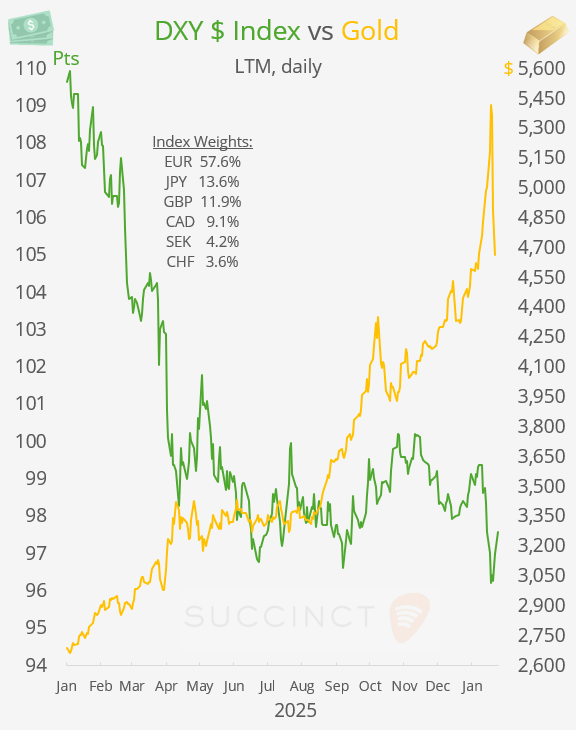

Gold (spot) slid another 4.5% as the post-rally unwind continued, with stretched positioning and crowded trades triggering forced selling after January’s parabolic run. The catalyst was Trump’s nomination of Kevin Warsh as Fed chair, which eased fears of a dovish Fed and inflation risk, reducing gold’s safe-haven appeal, even as silver began to stabilise.

Korea’s Kospi index plunged 5.2% as heavy selling hit large caps, especially semiconductor and tech names like Samsung Electronics (-6%) and SK Hynix (-8%), triggering a market safety mechanism after futures fell >5%.

On the tariffs front, the US said it will slash tariffs on Indian goods to 18% from as high as 50% after Prime Minister Modi agreed to halt purchases of Russian oil. The move ends months of trade friction and signals a broader reset, with Washington also pushing India to boost purchases of US energy and goods.

Earnings: → Despite beating earnings and revenue expectations, Disney’s (mcap $187bn) stock slid ~7% as guidance was cautious and key segments like Entertainment/Parks showed pressures, raising investor concerns about near-term growth. Weakness in international park visitation forecasts and slower operating profit in some divisions overshadowed the quarterly beat and spurred the sell-off. The stock is also down 7% YTD and 7% in the LTM. (CNBC)

→ After the close, Palantir Technologies (mcap $352bn) reported strong quarterly results that beat expectations and showed robust growth across commercial and government segments, fueling optimism around its AI-driven revenue momentum and raising guidance. As a result, the stock rallied by ~7% in extended trading, reflecting investor enthusiasm over its accelerating business performance. (Yahoo)

Economics: → The US ISM Manufacturing PMI jumped to 52.6 in January from 47.9 in December, signalling a return to expansion and marking the highest reading since August 2022. This beat expectations and reflected strong new orders and production gains, though employment remains below 50, and some tariff-related cost pressures persist.

Corporate Deals: → Devon Energy agreed to buy Coterra Energy in a $21.5bn all-stock deal (valuing the combined group at ~$58bn), creating one of the largest U.S. shale producers and a dominant Permian Basin player. Devon shareholders will own ~54% of the merged company, which targets $1bn in annual pre-tax synergies by 2027, alongside a $5bn share buyback.

→ Brookfield A.M. agreed to acquire Peakstone Realty Trust for $1.2bn in an all-cash deal, expanding its industrial real estate platform into industrial outdoor storage assets. Peakstone shareholders will receive $21 per share, a 34% premium to the last close.

→ In Canada’s mining sector, ElDorado Gold (mcap $7.8bn) agreed to acquire Foran Mining (mcap $2.4bn) for $2.8 bn including debt, creating a diversified gold and copper miner. The combined group is expected to produce 900,000 gold-equivalent ounces in 2027, with ElDorado shareholders owning 75% of the merged company. ElDorado shares fell 10% today while Foran’s lost 7%.

Day Ahead: Monetary Policy → RBA (+25bp to 3.85% expected). Data → US JOLTs jobs, France inflation. Earnings → ADM, Merck, PepsiCo, Amgen, Pfizer.

See you tomorrow.

Copyright © 2025 Succinct.

All rights reserved. This publication contains proprietary content and is intended solely for the recipient’s personal use. Disclaimer: Our service is for informational purposes only and does not constitute personal financial advice.