Mon 2 Mar: After the Bell

Oil Surges, Havens Falter as Geopolitics Drive Cross-Asset Moves

Good evening,

Geopolitics and the escalating situation in the Middle East dominated weekend headlines and set the tone for Monday’s trading, though market reactions were more nuanced than expected. US equities opened sharply lower before stabilising, with the S&P 500 finishing flat and the Nasdaq Composite edging higher, helped by a strong rally in the energy sector. The Nasdaq opened at the lowest level in three months but recovered during the session, while the VIX index traded as high as 25.2% before easing to close at 21.4%.

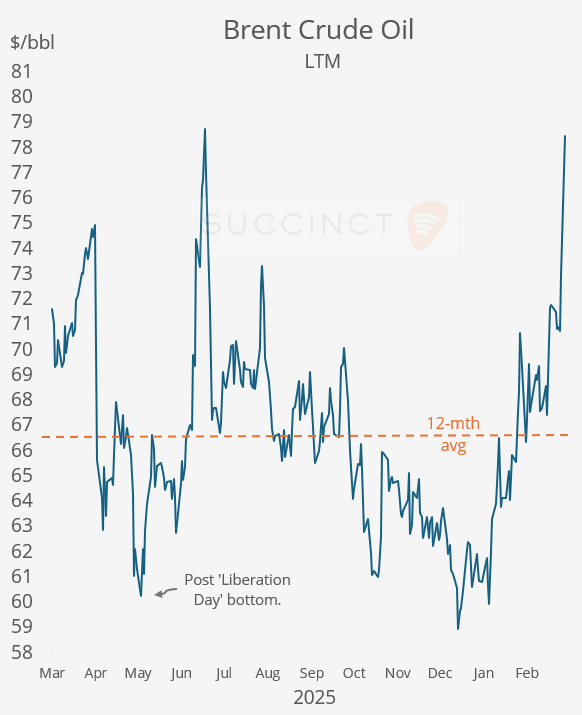

European and Asian markets largely sold off, with airlines among the hardest hit, while other risk assets such as Bitcoin posted gains. Brent crude surged 7.7%, its largest one-day move since June, on fears of prolonged disruptions to the Strait of Hormuz and escalating attacks on regional energy infrastructure.

Treasury yields moved higher rather than acting as a safe haven, with the 10-year ending at 4.04%, as inflation concerns tied to higher oil prices outweighed risk-off demand. Currency markets saw sharp intraday volatility, ultimately closing with a stronger $ as traditional havens, the Swiss franc and Japanese ¥, fell materially. The DXY $ index jumped to the highest level in six weeks.

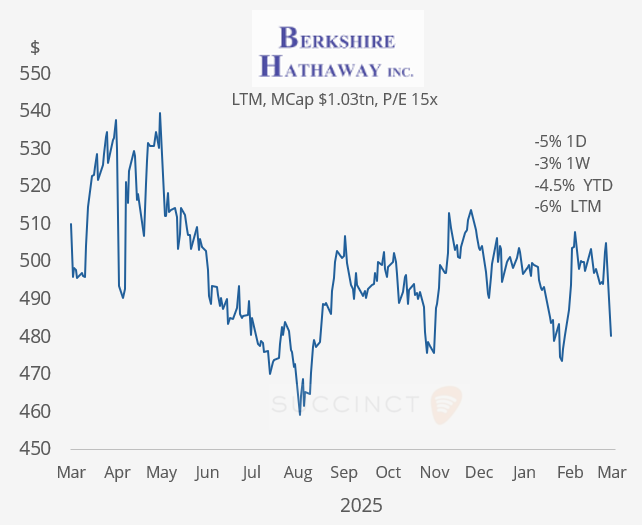

Earnings: → Berkshire Hathaway reported on Saturday, and shares fell 5% today as Q4 results missed expectations, with operating profit down ~30% and insurance underwriting income off more than 50%, signalling tougher conditions in core P&C. While Greg Abel struck the right tone in his first shareholder letter, there was no change in capital allocation—no buybacks, no dividend signal. Cash hit a record $373bn, reinforcing the market’s concern about near-term returns absent a major acquisition or valuation reset. Shares are 4% lower YTD and -6% in the LTM.

Corporate Deals: → BlackRock (via Global Infrastructure Partners) and EQT have agreed to acquire AES Corporation (mcap $10bn) for $10.7bn, paying $15 per share, a ~40% premium to the prior 30-day VWAP but well below Friday’s close. The deal provides growth capital to expand US power generation as AI-driven data-centre demand accelerates electricity needs, easing pressure on AES’s balance sheet and future dividends. AES shares plunged 18% today.

→ BlackRock is selling its remaining 11.4% stake in Spain’s Naturgy Energy Group via an accelerated bookbuild, following a prior ~7% disposal last year, effectively completing its exit. Naturgy, valued at around €26bn, operates across the gas value chain, including supply, liquefaction, regasification, transport, storage, distribution, and sales.

→ In private markets, Warburg Pincus will invest up to $1bn in Global Eggs, a privately owned and controlled Brazilian company, at an $8bn valuation via its Capital Solutions Founders Fund. Founded in 2018, Global Eggs operates 50+ farms across the US, South America and Europe, producing 15bn+ eggs annually under a vertically integrated model, with proceeds funding international expansion and efficiency gains.

Day Ahead:

Data → €-zone and Turkey inflation; Brazil GDP. Earnings → CrowdStrike, Autozone, Target, Ross Stores, Best Buy.

See you tomorrow.

Copyright © 2026 Succinct.

All rights reserved. This publication contains proprietary content and is intended solely for the recipient’s personal use. Disclaimer: Our service is for informational purposes only and does not constitute personal financial advice.