Mon 20 Apr: After the Bell

Markets Cautious, Oil Jumps on Renewed Middle East Stress

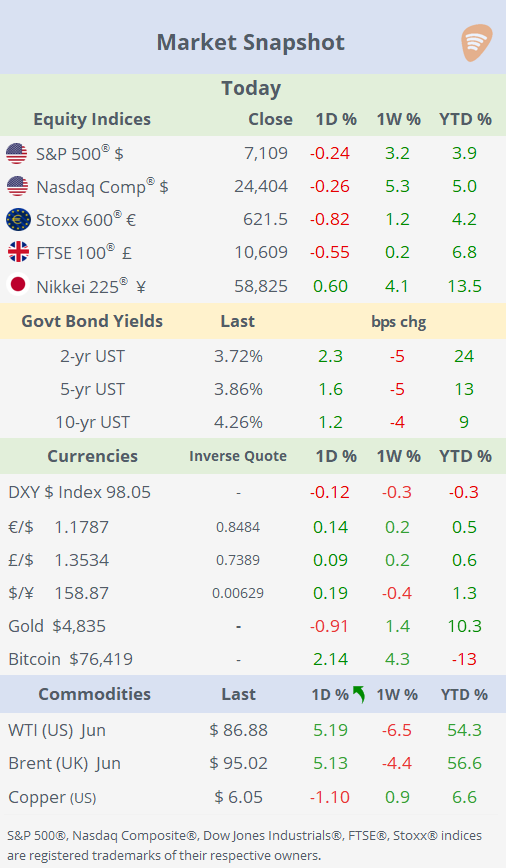

📈 Today’s performance tables.

Good evening,

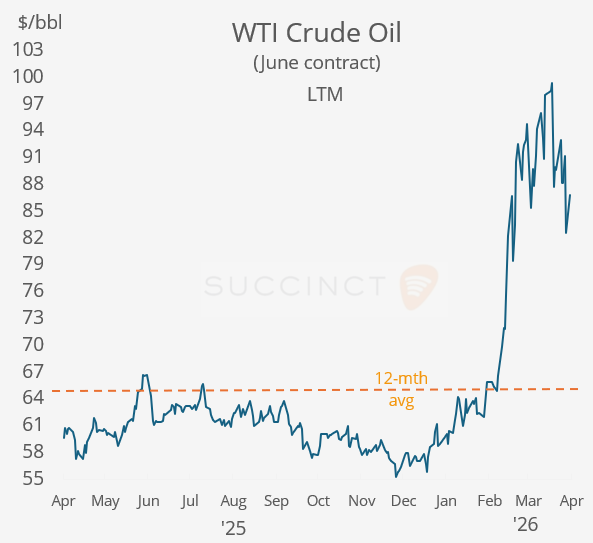

Markets began the week cautiously as renewed US-Iran tensions unsettled investors, lifting oil prices and pulling equities marginally lower. The Dow slipped while the S&P 500 and Nasdaq eased from recent record highs after a turbulent weekend in which the US reportedly seized an Iranian vessel, Iran responded by targeting ships and halting traffic through the Strait of Hormuz, and Trump said he still aims for a deal, but a truce extension appears unlikely.

Energy markets reacted immediately: crude surged ~5% on Monday, though prices remain below the $100/barrel threshold. Supply concerns intensified after Kuwait declared additional force majeure on crude and refined-product shipments, highlighting how prolonged Hormuz disruption could tighten global flows and keep inflation pressures elevated.

Investors now turn to earnings season, with nearly one-fifth of S&P 500 companies reporting this week, including major aerospace & defence names as well as Intel and Tesla. Markets are balancing strong corporate fundamentals against rising geopolitical risk, higher energy prices, and the possibility that renewed inflation pressure could complicate the rate outlook.

Business News: → Tim Cook will step down as CEO of Apple, and John Ternus, head of hardware engineering, will assume the role on Sep 1. Shares advanced 1% today and are flat YTD.

Economics: → Germany producer prices (PPI) jumped +2.5% MoM in March, the sharpest monthly rise since August 2022 and far above expectations, largely signalling a sudden rebound in industrial input costs after prior weakness. Despite the monthly spike, annual PPI was still -0.2% YoY, showing producer inflation remains below year-ago levels but is rapidly normalising.

→ Canada’s March CPI jumped to 2.4% YoY (from 1.8%) and 0.9% MoM, driven mainly by a gasoline surge tied to the Iran conflict and higher global oil prices. Still, softer-than-expected core inflation near 2.5% suggests broader domestic price pressures remain contained. Markets are likely to read this as an energy shock rather than generalised inflation, meaning the Bank of Canada can probably stay on hold unless oil-driven price gains begin spreading into services and wages.

Deals: → In US biotech, Eli Lilly & Co (mcap $826bn) agreed to acquire privately owned Kelonia Therapeutics for up to $7bn, including $3.25bn upfront cash plus milestone payments tied to clinical, regulatory, and commercial progress. Lilly is using cash flows from obesity drugs to aggressively diversify into oncology and next-generation gene/cell therapies. Kelonia’s main asset is KLN-1010, an early-stage in vivo CAR-T therapy for multiple myeloma.

→ QXO Inc (mcap $17bn), a US building-products consolidator, is buying US-based TopBuild Corp (mcap $14bn) for $17bn to gain scale in construction materials distribution and insulation services. Terms: $505/share in a mix of 45% cash and 55% QXO stock, a 23% premium to TopBuild’s prior price. The deal expands QXO into the North American housing, renovation, and commercial building supply market. TopBuild shares gained 19% today and 71% in the LTM.

→ In Canada’s real estate sector, Choice Properties REIT and KingSett Capital will acquire First Capital REIT in a CAD 9.4bn transaction including debt, with shareholders receiving cash plus stock worth an 11.7% premium to the prior close. Choice will take First Capital’s grocery-anchored retail assets (CAD5bn), while KingSett will acquire the remaining portfolio (CAD4.4bn), effectively splitting one of Canada’s major open-air shopping centre owners.

Day Ahead:

Data → US ADP employment change, retail sales, pending home sales; UK employment; Japan balance of trade.

Earnings → GE Aerospace, UnitedHealth, Raytheon Tech, BHP, Danaher, Intuitive Surgical, 3M.

USMD will take a break until next Monday.

Copyright © 2026 Succinct.

All rights reserved. This publication contains proprietary content and is intended solely for the recipient’s personal use. Disclaimer: Our service is for informational purposes only and does not constitute personal financial advice.