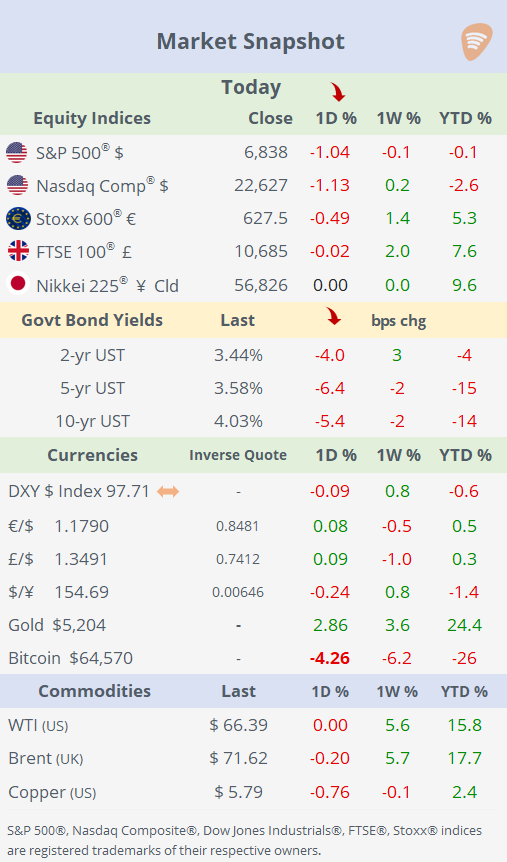

Mon 23 Feb: After the Bell

Risk-Off Monday: Equities Slide, Volatility Jumps, Safe Havens Rally

Good evening,

It was a weak start to the week for risk assets, with US equities selling off sharply amid volatility that spiked and as investors rotated toward safety. The VIX jumped above 21%, Bitcoin slid another 5%, and bonds rallied, while the $ index and crude oil were little changed. Gold and silver (+7%), meanwhile, extended Friday’s rally as risk aversion deepened.

Stocks tumbled as markets digested renewed trade uncertainty following Trump’s decision to raise global tariffs, alongside growing concerns about AI-driven disruption across multiple industries. The financial sector underperformed, dragging benchmarks lower as American Express, Visa, Mastercard, Goldman Sachs, and JPMorgan posted steep declines. Software names were hit again after a report from Citrini Research reignited fears over the economic impact of AI, with Microsoft, CrowdStrike, AppLovin, and Intuit all coming under renewed pressure.

On Friday, the Supreme Court ruled that Trump exceeded his authority by imposing sweeping global tariffs under emergency powers, prompting legal uncertainty over billions in collected duties. In response, Trump swiftly signed a new tariff order imposing a 10% global tariff, then raised it to 15% under a different trade statute to keep broad import levies in place despite the setback. It’s unclear whether the administration will refund businesses that paid levies.

Tensions between Washington and Iran remain elevated, with the US increasing military readiness in the Middle East and pulling non-essential diplomatic staff from parts of the region. Diplomatic channels remain open, but the situation is fragile, with risks of escalation still high.

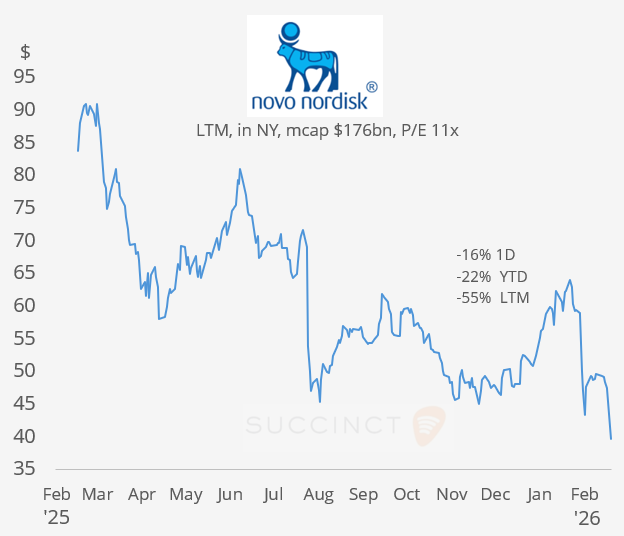

European healthcare giant Novo Nordisk (mcap $176bn) saw shares plunge 16% after trial results showed its new obesity drug CagriSema delivered less weight loss than a rival therapy from Eli Lilly, denting confidence in its next growth engine. The disappointment weighed heavily on the Danish market, underscoring Novo’s outsized importance after its blockbuster success with Ozempic and Wegovy. Novo shares in New York have lost 55% in the LTM.

Economics: → US factory orders fell 0.7% MoM in December, driven by a sharp drop in commercial aircraft bookings despite strength in other sectors, signalling mixed momentum in manufacturing demand.

→ Germany’s Ifo indicators suggest business sentiment is gradually improving, with firms reporting a more constructive view of current conditions and the outlook than in the prior month, pointing to tentative stabilisation in the economy.

Earnings: → There were no significant large-cap releases today. The next big update will be Nvidia reporting after the close on Wednesday.

Corporate Deals: → Gilead Sciences (mcap $185bn) will acquire biotech firm Arcellx (mcap $6.6bn) for up to $7.8bn, paying $115/share plus a contingent $5, a 68% premium to Arcellx’s prior 30-day average. Arcellx shares jumped 77% today. The deal underscores big pharma’s push to buy public, late-stage biotech firms with near-market oncology assets, building on Gilead’s existing CAR-T partnership with Arcellx ahead of a key FDA decision.

→ PayPal Holdings (mcap $41bn) has attracted unsolicited takeover interest after its share price decline (-25% YTD, -41% LTM), with banks and at least one major rival exploring a potential acquisition or selective asset deals, according to Bloomberg. Shares gained 5% today.

→ In private markets, KKR is set to acquire private equity-owned (TPG and Temasek) XCL Education for about $1.3bn, expanding its exposure to the UK private education market, according to Bloomberg.

Day Ahead:

Data → US house prices, CB consumer confidence, ADP weekly employment change; Australia CPI. Earnings → Home Depot, Realty Income, Bank of Nova Scotia, Constellation Energy.

See you tomorrow.

Copyright © 2026 Succinct.

All rights reserved. This publication contains proprietary content and is intended solely for the recipient’s personal use. Disclaimer: Our service is for informational purposes only and does not constitute personal financial advice.