Mon 23 Mar: After the Bell

Relief Rally: Trump Signals Pause, Risk Assets Surge

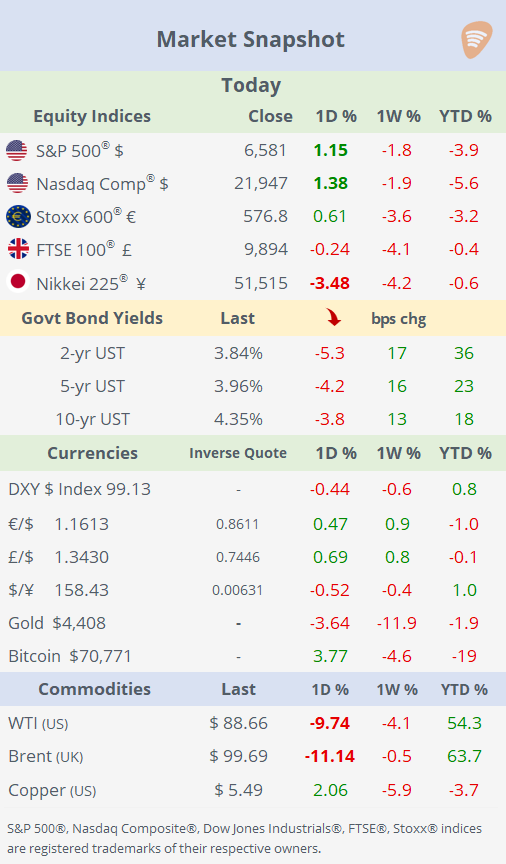

📈 Today’s performance tables.

Good evening,

Risk assets staged a strong rebound on Monday in an otherwise quiet session for data and earnings, with markets once again driven almost entirely by geopolitics and developments around the war. Sentiment improved sharply after Trump signalled a potential pause in attacks and cited “productive” negotiations, including a five-day delay on strikes targeting Iranian energy infrastructure. However, Iran pushed back, denying any direct talks with Washington, highlighting the fragility and uncertainty of the situation.

Markets reacted with a classic relief rally: crude oil plunged more than 10% as fears of supply disruption eased, equities rallied across the US and Europe (after earlier weakness in Asia, particularly Korea), and bond yields edged lower by a few basis points.

The $ index weakened slightly today but remains somewhat directionless and below 100 points, while precious metals sold off, with gold falling below 4,500 and touching intraday lows near 4,100, its weakest level since late November, as risk appetite improved.

Corporate Deals:

→ In Italy, the Poste Italiane (mcap €26bn) bid ~€11bn (cash + stock) for Telecom Italia (mcap €13.5bn), implying a ~9% premium and potentially bringing the telecom group back under state influence. The deal aims to create a national champion (incl. AI ambitions), but Poste shares fell sharply (7%) on dilution concerns while Telecom Italia rose; the target continues restructuring and deleveraging efforts.

→ In biotech, Gilead Sciences (mcap $170bn) is nearing a deal to acquire privately held Ouro Medicines for up to ~$2bn ($1.5bn upfront + milestones), expanding into autoimmune therapies. The move signals renewed M&A activity supported by a strong share price, following its recent ~$7.8bn acquisition of Arcellx.

Day Ahead:

Data → US ADP employment (weekly) change; Australia inflation; US, UK and EU PMIs. Earnings → China Telecom.

See you tomorrow.

Copyright © 2026 Succinct.

All rights reserved. This publication contains proprietary content and is intended solely for the recipient’s personal use. Disclaimer: Our service is for informational purposes only and does not constitute personal financial advice.