Mon 27 Apr: After the Bell

Calm Start to the Week: Equities Firmer, Crude Surges

📈 Today’s performance tables.

Good evening,

Global markets began the week in relatively calm fashion, with US equities edging to fresh record highs despite a dramatic weekend assassination attempt on President Trump in Washington and lingering geopolitical uncertainty. Investors appeared encouraged by further signs of possible Middle East de-escalation, as Iran reportedly floated a proposal to halt attacks in the Strait of Hormuz in exchange for an end to hostilities and relief from US pressure measures.

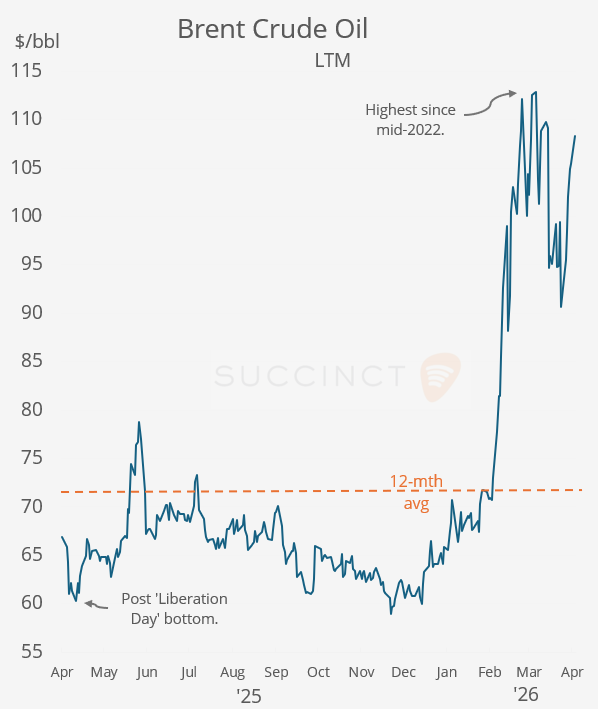

Crude oil nonetheless climbed roughly 3%, supported by continued supply-risk pricing around Hormuz and reports that major banks, including JPMorgan, raised their oil forecasts. Elsewhere, Treasury yields moved modestly higher, the dollar was little changed, and FX markets were broadly quiet. In Washington, the DOJ’s decision to end its probe into Fed Chair Powell also helped clear the path for Kevin Warsh to succeed him next month, with Powell’s future board role now the remaining policy wildcard.

→ Canadian PM Mark Carney launched the CAD25bn ($18bn) Canada Strong Fund, the country’s first federal sovereign wealth fund, to co-finance strategic infrastructure and national projects. The move aims to boost growth, attract private capital, and strengthen Canada’s economy amid U.S. tariff pressure.

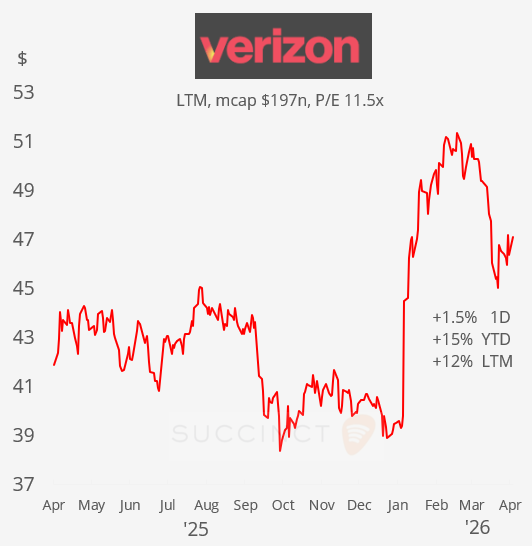

Earnings: → Monday was a quiet day for corporate results. Verizon Comm (mcap $198bn) rose 1.5% after reporting EPS above estimates, unexpected positive postpaid phone subscriber adds and raising full-year profit guidance. Investors looked past a small revenue miss, focusing on improving wireless momentum and a stronger outlook. Shares are 16% higher this year.

Deals: → In the energy sector, Shell agreed to acquire Canada’s natural gas producer ARC Resources (mcap $13bn) for $16.4bn (cash, shares and assumed debt), marking its largest deal since the BG Group takeover a decade ago. The acquisition boosts Shell’s shale output and growth profile, addressing investor concerns over limited production expansion. ARC shares jumped 21% today and and is 20% higher YTD.

→ In the pharma sector, India’s Sun Pharma will acquire New Jersey-based Organon & Co (mcap $3.4bn) for a total enterprise value of $11.75bn in cash, paying $14 per share to buy the Merck spinoff with operations across 140 countries. The deal transforms Sun into a top-three global women’s health player and a top-seven biosimilars company, expanding beyond its core generics franchise. Organon shares jumped 17% today.

→ In the healthcare sector, Thermo Fisher (mcap $173bn) will sell its microbiology business to European private-equity firm Astorg for $1.1bn. The unit generated $645mn of revenue last year, implying a sale at roughly 1.7x sales.

Day Ahead:

Data → US ADP employment change, Australia CPI.

Monetary Policy → Bank of Japan rate decision (unch at 0.75% exp)

Earnings → Visa, Coca-Cola, T-Mobile, Airbus, Booking H, GM, Starbucks, UPS, BP, Barclays, Mondelez.

Copyright © 2026 Succinct.

All rights reserved. This publication contains proprietary content and is intended solely for the recipient’s personal use. Disclaimer: Our service is for informational purposes only and does not constitute personal financial advice.