Mon 30 Mar: After the Bell

Risk-Off Extends: Oil Jumps, Stocks Fall, Bonds Rally

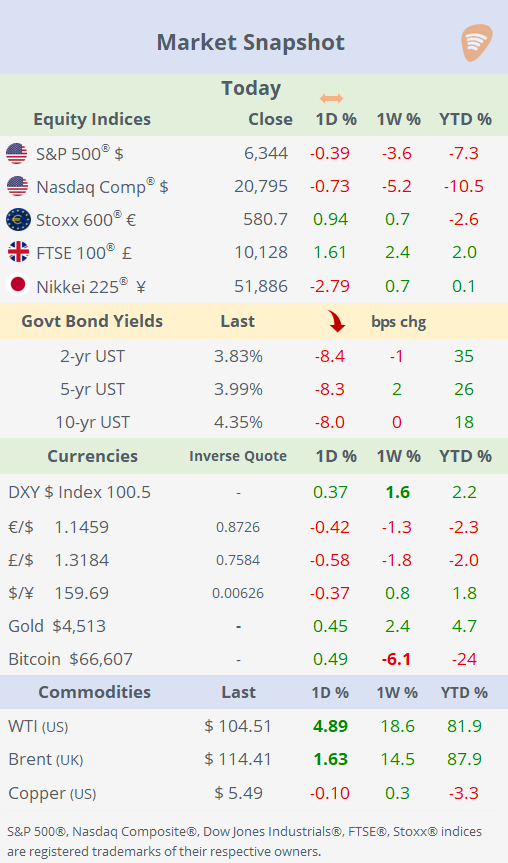

📈 Today’s performance tables.

Good evening,

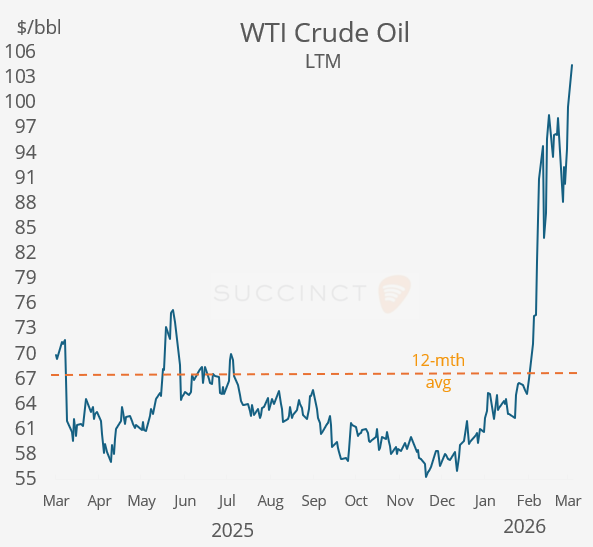

Another weak session to start the week, driven by higher oil prices, conflicting signals on the Middle East conflict and cautious messaging from central banks. WTI oil rose ~5% on the day, extending its weekly rally to +18%, as Trump oscillated between signaling diplomatic progress with Iran and renewing threats of strikes on energy infrastructure, keeping markets on edge. Equities on Wall Street declined globally, with the Nasdaq Composite now firmly in correction territory, while IT and industrials led losses and financials outperformed.

Within tech, the Philadelphia Semiconductor Index (SOX) dropped 4% on the day, down ~8% over the past week and 12% over the past month, with memory names under heavy pressure (Micron Tech -10%, Western Digital -9%).

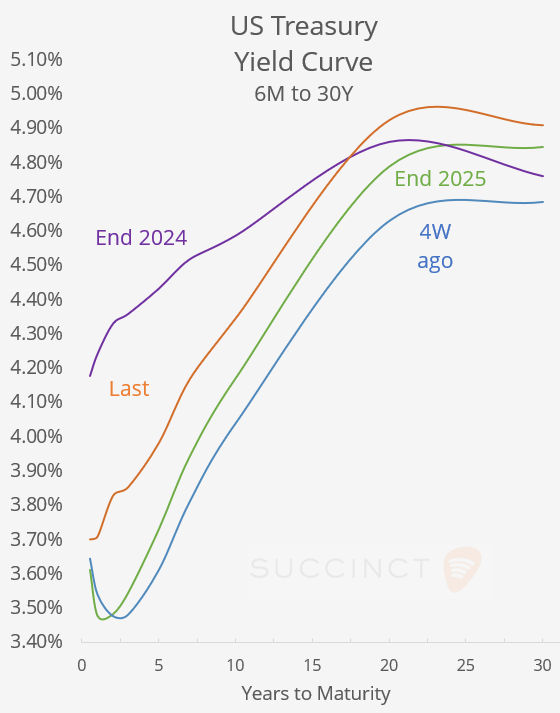

Fixed income saw a notable reversal, with Treasury yields across the 2 to 10-year segment falling 8 bp following remarks from Jerome Powell, supporting a bond rally as investors reassessed the policy outlook.

Overall, markets remain highly sensitive to geopolitical headlines, with oil acting as the key transmission channel into inflation expectations, rates, and broader risk sentiment.

Central Banks: → In Fed talk today, Jerome Powell struck a measured tone, reiterating a “wait-and-see” approach as inflation remains above target while the central bank assesses the impact of geopolitical shocks, particularly oil. He noted that tariffs would likely result in a one-off price bump and emphasised that the Federal Reserve has limited control over supply-driven inflation, adding that longer-term inflation expectations remain well anchored.

Markets reacted with a bond rally, as traders reassessed the policy path, with year-end futures pricing shifting sharply; the implied probability of a rate hike by December fell from 22% on Friday to ~4% today, reinforcing expectations that the Fed will remain on hold unless inflation re-accelerates materially.

Economics: → Germany’s preliminary CPI for March came in at +1.1% MoM and +2.7% YoY, with the monthly jump largely reflecting energy-related pressures, while the annual rate remains moderately above the ECB’s target. In terms of trend, inflation is broadly stabilising with a slight upward bias after prior easing, suggesting disinflation has slowed. The overall signal is mixed: while not alarming, the data points to sticky price pressures, particularly from energy, which may keep the European Central Bank cautious on the pace of rate cuts.

Business News: → Government-controlled mortgage providers Fannie Mae (mcap $8bn) and Freddie Mac (mcap $4bn) stocks surged ~50% today, following bullish comments from investor Bill Ackman (Pershing Square Capital), who described the mortgage giants as “stupidly cheap” and possessing massive “10x” upside potential. The rally was driven by renewed investor optimism regarding a potential end to government control, despite the stocks remaining well below previous highs.

Deals: → Houston-based Sysco Corp (mcap $33bn), the biggest US food distributor to restaurants, hospitals and schools, has agreed to acquire privately-owned Jetro Restaurant Depot, based in NY, for ~$29bn (incl. debt; $21.6bn cash + stock), marking a major expansion into the cash-and-carry segment. The deal targets higher-margin, resilient small-business customers, strengthening Sysco’s positioning across economic cycles and broadening its local distribution footprint. Sysco shares plunged 15% today and are ~6% lower YTD.

→ Swiss food giant Nestlé SA (mcap $250bn) is advancing the sale of a 50% stake in its European water division (incl. Perrier and San Pellegrino), with bids from KKR, Clayton Dubilier & Rice and PAI Partners valuing the unit at €5bn. The deal is part of Nestlé’s broader portfolio overhaul, as it pivots toward core segments and taps private equity to monetize non-core assets.

→ In private markets, Apollo is nearing a ~$10bn deal to acquire Atlantic Aviation from KKR, in partnership with Singapore’s GIC, with KKR expected to retain a minority stake. The transaction highlights continued strong demand for infrastructure-like assets, with Atlantic Aviation, a large US network of private jet service bases, offering stable, cash-generative exposure to business aviation.

Day Ahead:

Data → €-zone, France, Italy inflation; Canada GDP; US Jolts openings; Germany retail sales.

Earnings → Nike (PM). See you tomorrow.

Copyright © 2026 Succinct.

All rights reserved. This publication contains proprietary content and is intended solely for the recipient’s personal use. Disclaimer: Our service is for informational purposes only and does not constitute personal financial advice.