Mon 4 May: After the Bell

Oil Surges as Hormuz Tensions Reignite Risk-Off Trade

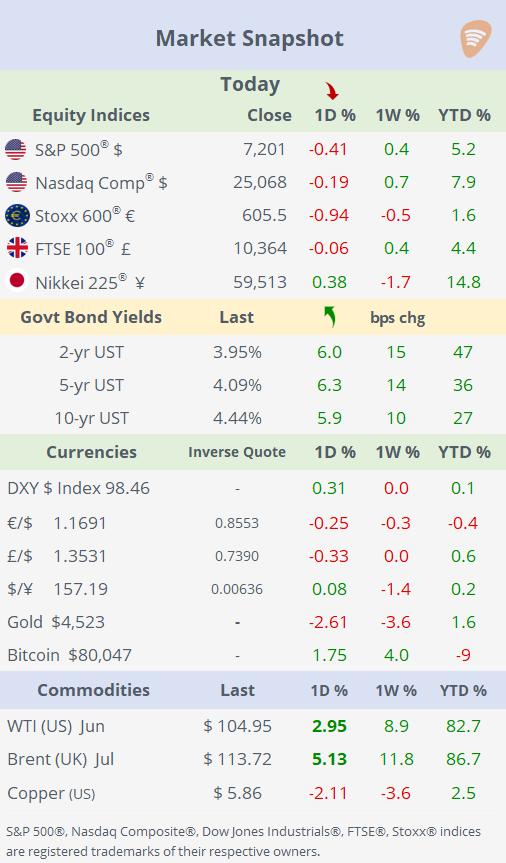

📈 Today’s performance tables.

Good evening,

Markets opened the week in risk-off mode after geopolitical tensions in the Middle East escalated sharply over the weekend, raising fears of disruption in the Strait of Hormuz. The fragile four-week ceasefire between the US and Iran appears to be unravelling. US forces reportedly intercepted Iranian drones, missiles, and fast boats while escorting two US-flagged vessels through Hormuz, while attacks also struck commercial ships and a key oil hub in the UAE.

In a Monday post, Trump said Iran had fired at “unrelated nations,” including a South Korean cargo ship, adding that US forces had destroyed seven Iranian “fast boats.” Conflicting headlines continue to emerge from the Gulf, but the direction of travel is clear: the situation has materially deteriorated.

Markets reacted swiftly. Brent crude surged over 5%, briefly trading around $114, as investors priced in higher supply disruption risk. Treasuries also sold off, with the 2-year yield rising 6bp to a six-week high, while equities moved lower globally.

European stocks underperformed after Trump separately announced tariffs on EU autos would rise to 25% from 15%, pressuring automakers. On Wall Street, losses were more contained, though the Dow fell 1%, while the VIX Index climbed to 18.3%, up from a three-month low but still well below the peak levels seen earlier this year.

For now, markets are treating this as a geopolitical risk shock rather than a systemic event, but that could change quickly if energy infrastructure or shipping flows face sustained disruption.

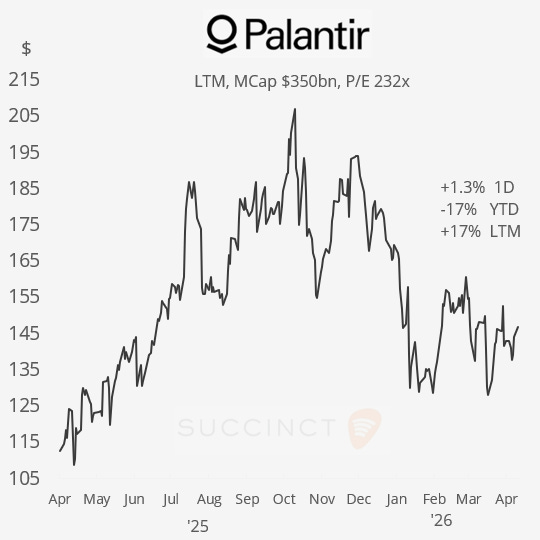

Earnings: → Palantir Technologies (mcap $350bn) reported after the close, with record Q1 revenue and profit that beat analyst estimates, driven by surging sales to commercial clients and the US government sector. Revenue jumped 85% YoY to $1.6bn, with the bulk coming from the US. Adjusted earnings per share rose over 150% YoY ($876mn net profit, 54% margin). It raised FY sales guidance by 6% to ~$7.6bn. Shares gained 1.3% during regular hours and just 0.8% in extended trading.

Economics: → It was a light start to the week on the data front. US factory orders rose 1.5% MoM in March, well above the 0.5% consensus and up from a revised 0.3% gain in February, while orders increased 3.7% YoY, the strongest monthly rise since November. The report points to improving manufacturing momentum, driven largely by surging demand for electronics and AI-related equipment, though higher energy costs and supply-chain risks tied to the Middle East remain a growing headwind.

Deals: → GameStop Corp (mcap $11bn) launched an unsolicited $56bn bid for eBay (mcap $49bn), offering $125/share (50% cash, 50% stock), a 20% premium to eBay’s undisturbed price, after quietly building a 5% stake. GameStop CEO Ryan Cohen says the deal would reposition eBay as a stronger rival to Amazon.com, backed by a TD Bank commitment for up to $20bn in debt financing. GameStop shares fell 10% while eBay gained 5% today.

→ Travel services firm Global Business Travel Group (mcap $4.9bn) agreed to be taken private by Long Lake Management in a $6.3bn deal priced at $9.50/share, a roughly 60% premium. American Express (mcap $218bn) will sell its ~30% stake as part of the transaction and expects to receive $1.5bn in proceeds. GBTG shares jumped 57% today.

→ AI company Anthropic is forming a $1.5bn joint venture with Blackstone, Hellman & Friedman, and Goldman to help private-equity-backed companies deploy AI tools. The venture will serve as Anthropic’s consulting/distribution arm, highlighting intensifying competition with OpenAI, which is reportedly exploring a similar structure.

→ Houston-based Fervo Energy launched its US IPO roadshow, targeting a valuation of up to $6.5bn and raising around $1.3bn and a guidance range of $21–24. Fervo operates in the renewable energy / geothermal power sector, using oil-and-gas style horizontal drilling technology to deliver 24/7 carbon-free electricity, benefiting from rising power demand tied to AI data centres.

Day Ahead:

Monetary Policy decisions → Reserve Bank of Australia.

Data → US trade balance, Jolts job openings, new home sales; Korea CPI.

Earnings → AMD, Arista Networks, Pfizer, Shopify, HSBC.

Copyright © 2026 Succinct.

All rights reserved. This publication contains proprietary content and is intended solely for the recipient’s personal use. Disclaimer: Our service is for informational purposes only and does not constitute personal financial advice.