Mon 6 Apr: After the Bell

Geopolitics vs Macro: Markets Resilient Amid Hormuz Crisis

📈 Today’s performance tables.

Good evening,

Geopolitics dominated the Easter weekend, with the Middle East conflict and the blockade of the Strait of Hormuz continuing to drive oil prices and investor sentiment. Trump escalated rhetoric, warning Iran must agree to reopen the strait as part of a ceasefire deal by Tuesday or face potential military strikes on key infrastructure, while Tehran rejected the proposal and threatened more “crushing” retaliation; tensions were further heightened by the reported downing of two US fighter jets in Irani territory and failed attempts by Qatar’s LNG tankers to transit the strait.

Despite the escalation, markets showed resilience, with US equities recovering early losses as reports of diplomatic efforts, including a ceasefire framework involving Pakistan, revived hopes for de-escalation and a reopening of Hormuz. European markets remained closed for Easter Monday, while investor focus now turns to US CPI on Friday and a light earnings calendar, including Delta Air Lines on Wednesday, as macro data and geopolitics continue to set the tone.

Economics: → On Friday, the US released labour data for March. Non-farm payrolls rose by 178k with unemployment at 4.3%, both beating expectations (60k and 4.4%) and signalling a rebound. However, February was revised sharply lower to -133k jobs (from -92k initially), highlighting prior weakness and volatility in the labour market. The upside surprise in March was driven by healthcare and construction, but details were softer (lower participation, modest wages), suggesting uneven momentum. Overall sentiment: headline strong but quality mixed, reinforcing a cautious Fed stance as the labour market stabilises but remains fragile beneath the surface.

→ Today’s US ISM Services PMI came in at 54, in line with expectations but down from February, signalling continued expansion in services, albeit with some moderation in momentum.

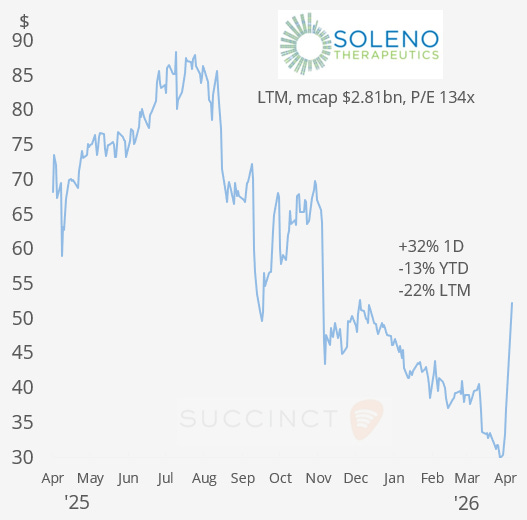

Deals: → California-based biotech Neurocrine Biosciences (mcap $13bn) will acquire Soleno Therapeutics (mcap $2.8bn) for $2.9bn (+34% premium), adding the only approved treatment for Prader-Willi syndrome to expand its rare-disease/endocrinology portfolio. The deal centres on Soleno’s Vykat XR, a newly launched drug generating ~$190m in 2025 sales, with Neurocrine funding the acquisition via cash and modest debt and targeting closing within ~90 days. Soleno shares jumped 32% today, 13% YTD, but remain 22% lower in the LTM.

→ French oil & gas giant TotalEnergies (mcap $197bn) and UAE-based renewable energy company Masdar are forming a $2.2bn 50/50 JV focused on onshore solar, wind and battery storage across nine Asian markets. The venture starts with 3GW operational capacity and targets 6GW by 2030, serving as the partners’ exclusive platform to capture Asia’s growing power demand.

Day Ahead:

Data → US durable goods and ADP employment change; €-zone Services PMI.

Earnings → n/a. See you tomorrow.

Copyright © 2026 Succinct.

All rights reserved. This publication contains proprietary content and is intended solely for the recipient’s personal use. Disclaimer: Our service is for informational purposes only and does not constitute personal financial advice.