Mon 6 Oct: After the Bell

🎙️📄+ Market Data

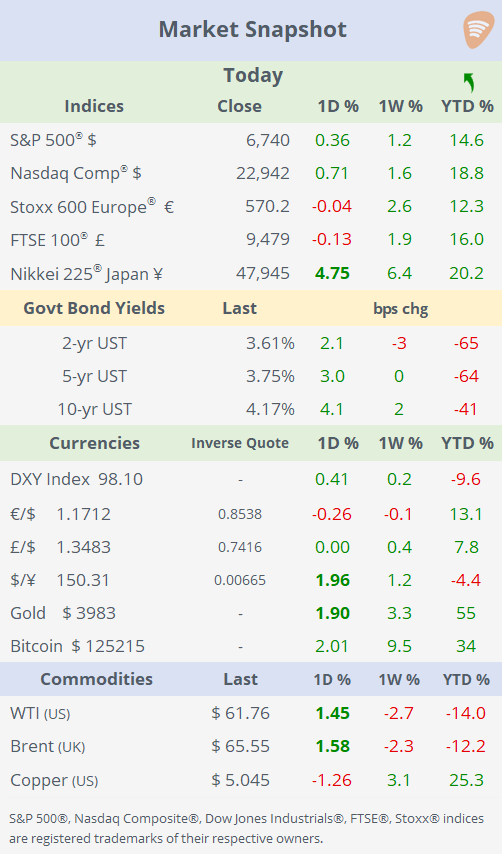

See the ‘Market Data’ post for tables & charts.❗

Good evening,

Wall Street kicked off the week with an active session, as benchmark indices enjoyed a strong day, led by Nasdaq’s outperformance on AMD’s massive rally. Both the S&P 500 and Nasdaq Composite closed at fresh record highs, underscoring the resilient mood in equities despite the government shutdown entering its sixth day. The S&P 500 accumulated a 14.5% gain this year, while the Nasdaq Composite is 19% higher. Europe’s broad Stoxx 600 index advanced 12% but the € appreciated 13% against the $.

Over the weekend, JPMorgan analysts highlighted a surge in precious metals and cryptos, describing the phenomenon as “dollar debasement”. Gold is racing toward an all-time high near $4,000, while Bitcoin has climbed above $125,000 following last week’s steep rally.

In forex markets, the DXY dollar index reversed recent weakness, gaining 0.4%, largely due to the sharp depreciation of the Japanese yen (~2%). The ¥ weakened after Japan’s ruling Liberal Democratic Party unexpectedly elected Sanae Takaichi as the next prime minister. Seen as a fiscal dove, Takaichi supports government stimulus measures to drive economic growth, fueling market concerns about fiscal and political stability. The Nikkei 225 rallied nearly 5% on Monday.

Core bond yields extended Friday’s upward momentum, moving a few basis points higher, with the 10-year UST yield reaching 4.17%.

Politics: France’s Prime Minister Lecornu has resigned after less than a month in office, following widespread criticism of his appointment. The resignation comes after Macron unveiled a largely unchanged cabinet lineup, sparking backlash over continuity and political strategy. Paris CAC 40 index fell 1.3% and the yield on 10-year French OATs closed 5bp higher today at 3.57%, the highest since 2011, and 85bp over Bunds.

On Sunday, OPEC+ decided to raise oil production by 137,000 barrels per day starting in November. This increase mirrors the modest hike implemented in October and is part of a gradual unwinding of previous production cuts. The decision comes amid concerns over a potential supply glut, especially as global demand shows signs of weakening and geopolitical tensions persist. This move is part of a broader strategy by OPEC+ to gradually reverse over 5mnbp in voluntary cuts initiated in 2022. Oil futures partially reversed their recent steep fall and recovered 1.5% today, as the decision was already priced in.

Data: €-zone retail sales rose 1% YoY in September, coming in below expectations and marking the weakest growth since mid-2024. The slowdown reflects softer consumer spending amid persistent inflationary pressures and economic uncertainty.

Central Banks: ECB President Christine Lagarde said the €-zone economy grew 0.7% in H1’25, supported by resilient domestic demand, though weaker exports are expected to temper growth later. She reaffirmed the central bank’s 2% inflation target, noting the current outlook is benign.

Deals: OpenAI has struck a multibillion-dollar deal with AMD (mcap $350bn) to secure hundreds of thousands of AI chips and obtain a warrant to buy up to 10% of AMD at one cent per share. The agreement positions OpenAI at the core of a massive AI infrastructure buildout. AMD forecasts over $100bn in revenue from OpenAI and related demand, as the stock jumps 24% to an all-time high and accumulates a 73% rally this year.

Regional bank Fifth Third Bancorp (mcap $28bn) announced an all-stock acquisition of Comerica Inc. (mcap $10bn) valued at $11bn, aiming to create the ninth-largest US bank with $288bn in assets. It’s the biggest banking deal of the year. Comerica shares jumped 13% to a 3-year high.

BASF SE (mcap €39bn) is close to agreeing a roughly €7bn deal to sell its coatings division, which has about €3.8bn in sales and 10k staff, to Carlyle. This divestment is part of BASF’s strategy to shore up capital amid energy cost pressures and could enable a share buyback sooner than previously planned.

In private markets, French investment firm Ardian is acquiring Ireland’s Energia Group from I Squared Capital for €2.5bn, in a move that bets on surging electricity demand driven by AI data centres and renewable energy growth.

IPOs: Private equity owners BC Partners and Pollen Street are gearing up to take Shawbrook public, as the British specialist lender announces plans for a London IPO that could value the company at up to £2bn.

Day Ahead: US trade balance; Germany factory orders; UK house prices; Speeches by four Fed governors.

See you tomorrow.

Copyright © 2025 Succinct.

All rights reserved. This publication contains proprietary content and is intended solely for the recipient’s personal use. Disclaimer: Our service is for informational purposes only and does not constitute personal financial advice.