Mon 8 Sep: After the Bell

🎙️📄+ Market Data

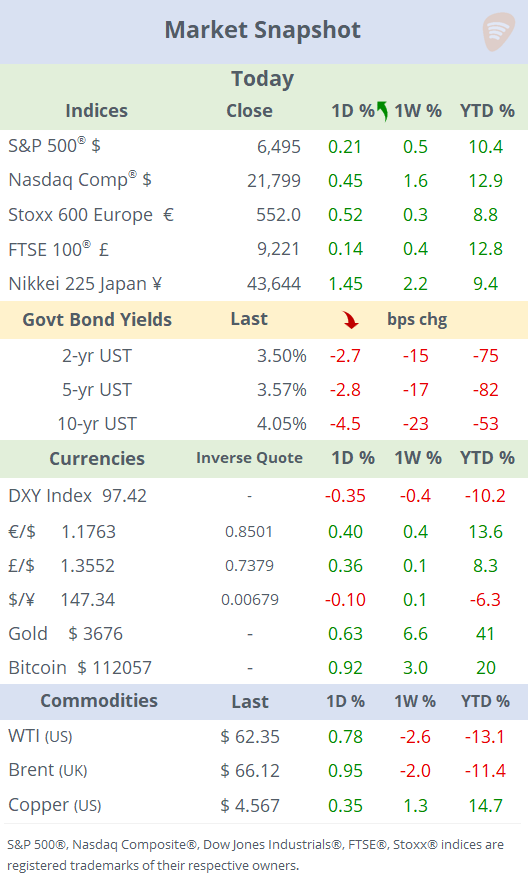

See the ‘Market Data’ post.

Good evening,

Stocks and bonds kicked off the week on a positive note, with major indices climbing around 0.4%, including the Nasdaq hitting an intraday record high. Benchmark 10-year Treasuries fell to a five-month low of 4.05% after a strong four-day rally fueled by growing expectations of faster Fed policy easing following the poor employment report on Friday.

The probability of a half-point rate cut by the Fed next week has risen to 12% versus 88% for a quarter-point reduction. Traders also see a roughly 66% chance that Fed fund rates will end the year at 3.625% compared to today’s 4.375%. This pulled the $ lower with the DXY index reaching its lowest level in seven weeks ahead of crucial market-moving events, including U.S. CPI inflation and the ECB’s policy meeting on Thursday.

In commodities, OPEC+ agreed yesterday to raise oil production by 137,000 barrels per day starting in October. This decision marks a shift from previous months' larger output hikes and reflects the group's strategy to regain market share. Oil prices gained today following Russia's strikes on Ukraine, which fueled expectations of further sanctions. Brent gained nearly 1% on Monday to $66.

Geopolitics: Russia launched its largest aerial assault on Ukraine during the weekend, targeting Kyiv with over 800 drones and missiles.

Japanese Prime Minister Ishiba resigned less than a year after he assumed office following his party's historic defeat in July's parliamentary elections, leading to a leadership vacuum and political uncertainty. The Nikkei 225 gained nearly 1.5% driven by a strong GDP update.

French PM Bayrou lost a confidence vote in parliament, leading to his resignation and highlighting ongoing political instability amid contentious austerity measures. 10-year French bond yields fell today in line with other sovereigns to 3.41% (76bp over Bunds).

Data: China released trade figures with exports in August rising 4.4% YoY, below estimates and the weakest print since February. Imports advanced 1.3% YoY, well below forecasts, but August was one of three positive months this year. This deceleration reflects waning effects from the U.S. tariff truce and persistent domestic demand challenges.

Also, Japan's economy grew at an annualised rate of 2.2% in Q2’25, up from the initial estimate of 1%, driven by stronger private consumption and improved inventory data.

Deals: In US regional banking, PNC Financial (mcap $80bn) will acquire privately owned Colorado-based FirstBank Holding for $4.1bn, significantly expanding its presence in Colorado and Arizona. The purchase will put PNC closer in size to Capital One and U.S. Bank.

In the Italian banking sector, Monte dei Paschi di Siena (mcap $9.3bn) has secured over 46% of Mediobanca's (mcap €15.7bn) shares in its €13.5bn takeover bid, surpassing the 35% minimum threshold and nearing its 50% target. Mediobanca shares gained 38% YTD.

In private markets, Elon Musk’s SpaceX announced it will acquire wireless spectrum licenses from EchoStar (mcap $22bn) for approximately $17bn, a pivotal move aimed at expanding Starlink’s emerging 5G connectivity business. EchoStar shares jumped 15% today (+237% YTD) to an all-time high.

No major earnings were released today, but Oracle is scheduled to report after the close tomorrow.

See you tomorrow.

Copyright © 2025 Succinct.

All rights reserved. This publication contains proprietary content and is intended solely for the recipient's personal use. Disclaimer: Our service is for informational purposes only and does not constitute personal financial advice.