Mon 9 Feb: After the Bell

Wall Street Builds on Bounce, Eyes Jobs and Inflation Data ...

ℹ️Find more performance tables here.

Good evening,

US equities extended their rebound on Monday, building on last week’s volatile close that saw the Dow break above 50,000 for the first time, as markets brace for a slate of earnings and key macro data. The Nasdaq Composite added ~1%, with investors still debating the disruptive impact of AI on software, highlighted by a sharp 20% drop in Monday.com, while broader tech staged a recovery, led by gains of more than 3% in Nvidia and AMD, a near-10% surge in Oracle, and a 2% rise in Microsoft.

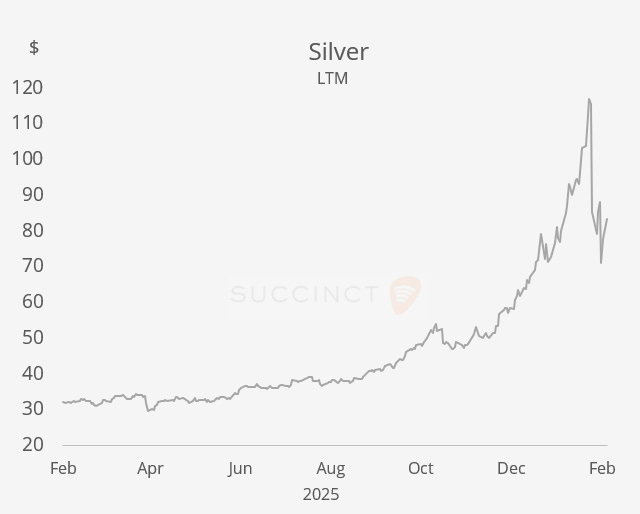

Attention now turns to macro catalysts later in the week, with markets in wait-and-see mode ahead of the delayed January US jobs report on Wednesday and CPI on Friday, while precious metals extended Friday’s rebound, with silver jumping 8% to around $83 and gold rising 2% back above $5,000.

Japan held a snap general election yesterday, and PM Takaichi secured a landslide victory, giving her ruling coalition a strong supermajority in the lower house. The Nikkei 225 gained ~4%, and the ¥ appreciated 0.8% against the $ today.

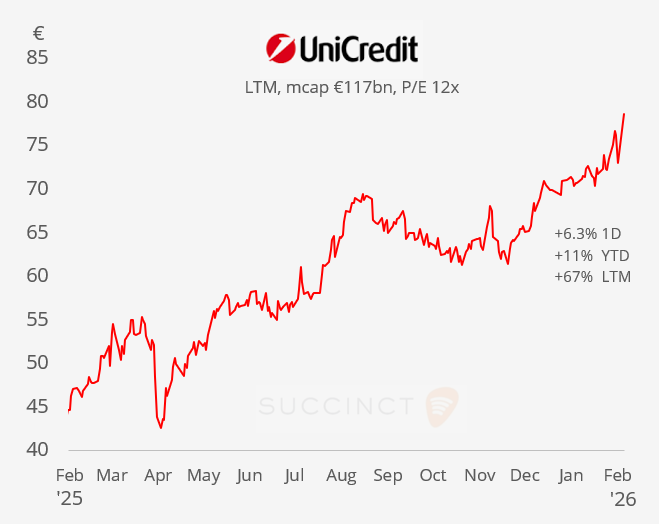

Earnings: → It was a quiet start to the week for earnings. Italian bank UniCredit (mcap €118bn) reported record 2025 results with a €10.6bn net profit (+14% YoY) and raised its medium-term profit outlook, backed by strong earnings from strategic stakes and generous shareholder distributions. The stock climbed 6% in Milan to a record high on the better-than-expected results and positive guidance.

Central Banks: → ECB’s Lagarde reaffirmed that €-zone inflation is projected to stabilise around the ECB’s 2% target over the medium term, even after a temporary dip below target, and emphasised the ECB’s meeting-by-meeting, data-dependent approach to future policy decisions.

Corporate Deals:

→ De Beers, the Anglo American-controlled diamond group with major African operations, is likely to be sold to a public-private consortium, according to Anglo CEO Duncan Wanblad, with Botswana’s government expected to increase its 15% stake. The sale process is well advanced and could be completed this year, despite a weakening global diamond market.

→ Private equity group Advent and FedEx agreed to acquire Polish parcel locker operator InPost in a €7.8bn takeover, offering €15.60/share, a 50% premium to early-January levels. The deal will see Advent and FedEx each take 37% stakes, with founder Rafał Brzoska retaining 16%, marking a return to private ownership less than four years after InPost’s €8bn IPO.

→ In the US oil & gas sector, Transocean (mcap $6.3bn) agreed to acquire Valaris (mcap $6bn) in a $5.8bn all-stock merger, creating an offshore drilling group with a combined enterprise value of $17bn and a fleet of 73 rigs. Valaris shareholders will own 47% of the combined company, with management targeting over $200mn in synergies as the deal positions the group to benefit from the offshore drilling upcycle. Valaris shares jumped 34% today.

→ In debt capital markets, Alphabet is accelerating its funding push for AI investment, lining up a rare 100-year (“century”) bond as part of its debut sterling issuance this week, alongside a $20bn dollar bond sale (upsized from $15bn on strong demand) and a planned Swiss franc deal. The move underscores Big Tech’s willingness to lock in long-dated funding to finance heavy AI capex, reviving an instrument typically seen only during ultra-low rate periods.

Day Ahead:

Data → US retail sales, ADP employment change; China CPI & PPI; Brazil CPI. Earnings → Coca-Cola, AstraZeneca, S&P Global, Gilead S, BP, Robinhood, Barclays, Spotify.

See you tomorrow.

Copyright © 2025 Succinct.

All rights reserved. This publication contains proprietary content and is intended solely for the recipient’s personal use. Disclaimer: Our service is for informational purposes only and does not constitute personal financial advice.