Mon 9 Mar: After the Bell

Oil Shock Sends Markets on a Wild Ride. +Gilts Selloff, China's Inflation Jump.

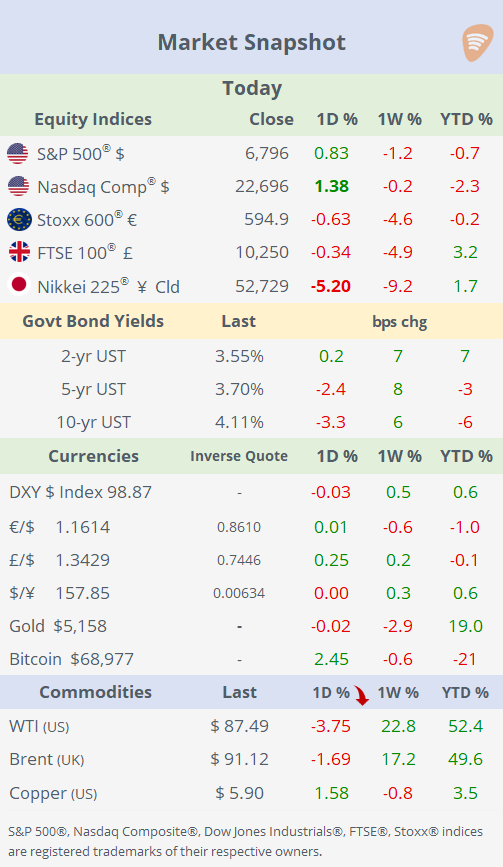

ℹ️Today’s Performance tables.

Good evening,

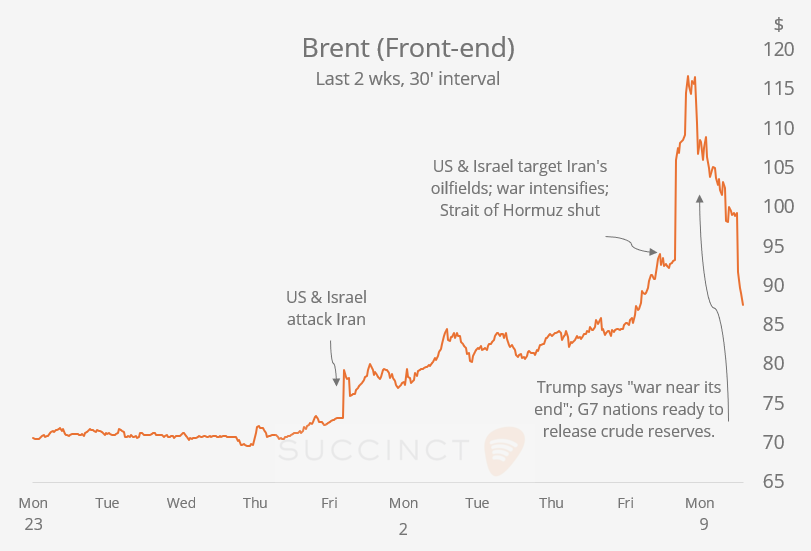

Markets experienced extreme volatility on Monday, driven primarily by dramatic swings in oil prices amid fast-moving developments in the Middle East conflict. Brent crude surged as much as 28% at the open to $119 per barrel following escalating strikes between the US, Israel and Iran over the weekend, but later reversed sharply to close near $90 after comments from Trump suggesting the war could be nearing its conclusion.

Energy markets remain the central focus for investors, with concerns around shipping disruptions in the Strait of Hormuz, potential supply losses across Gulf producers and the broader inflation impact of higher oil prices dominating sentiment. The sudden spike in crude has quickly altered the macro-outlook, complicating the Fed’s policy calculus, as sustained energy shocks could simultaneously push inflation higher while weighing on global growth.

Over the weekend, US and Israeli forces intensified air strikes across Iran, including attacks on fuel storage facilities in Tehran, while several Gulf producers reduced output or shut down fields. Qatar warned the conflict could halt oil and gas exports from the region within days, prompting G7 finance ministers to signal readiness to release emergency oil reserves if needed. The energy shock is expected to weigh more heavily on Europe and Asia, while the US, as a net energy exporter, remains relatively more insulated from the fallout.

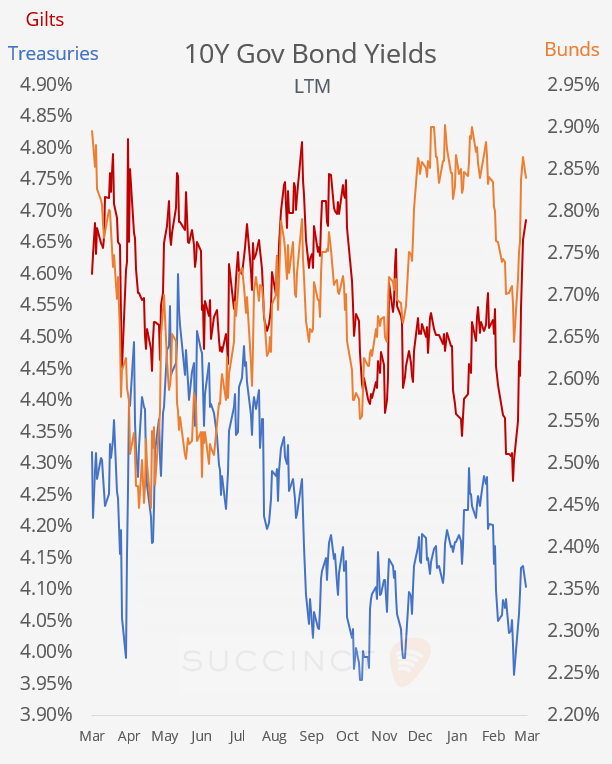

In rates markets, war-driven inflation fears triggered a sell-off in global bonds, with debt assets posting their worst week since October 2024 as traders unwind bets on interest rate cuts. UK gilts have been hit hardest, suffering their worst week since the 2022 pension crisis and pushing the 10-year yield to 4.68%.

Gilts have underperformed partly because more rate cuts were priced in before the conflict than in other economies such as the Eurozone, and because the UK’s energy mix leaves it more exposed to rising gas prices. Before the conflict, markets fully priced two quarter-point Bank of England cuts this year from the current 3.75% rate; they now see only about a 50% chance of a single cut.

Economics: → China’s inflation surprised to the upside, with CPI rising 1.0% MoM and 1.3% YoY in February, the strongest annual pace in over three years after a sharp rebound from January’s 0.2%. However, producer prices remained in deflation at −0.9% YoY, though the decline narrowed, signalling ongoing weakness in industrial demand. The data suggest that consumer prices are stabilising, partly due to Lunar New Year spending, while the manufacturing sector continues to face persistent deflationary pressures.

Corporate Deals: → Shell (mcap $244bn) agreed to sell US auto-service chain Jiffy Lube (based in Houston) to private equity firm Monomoy Capital for $1.3bn, more than two decades after acquiring the business. The deal includes the Jiffy Lube brand, the franchisee Premium Velocity Auto, and its network of franchised stores, while Shell retains its lubricants brands, including Pennzoil, Quaker State, and Rotella.

→ Private equity firm Lone Star Funds agreed to acquire the capsules and health ingredients unit of Swiss-listed life sciences group Lonza (mcap 45bn) in a deal valuing the business at CHF2.3bn (~$3bn). Lonza will retain a 40% minority stake in the unit and receive about CHF1.7bn upfront, as part of its strategy to streamline operations and focus on its core contract drug manufacturing business.

→ In private markets, KKR is exploring a potential $3bn sale of CoolIT Systems, a Canadian data-centre cooling technology provider, aiming for a 10× return on its 2023 investment amid strong demand for AI infrastructure; Mubadala holds a minority stake.

Day Ahead:

Data → US ADP weekly employment change, existing home sales; China, Germany and France trade. Earnings → Oracle, VW.

See you tomorrow.

Copyright © 2026 Succinct.

All rights reserved. This publication contains proprietary content and is intended solely for the recipient’s personal use. Disclaimer: Our service is for informational purposes only and does not constitute personal financial advice.