Thu 12 Feb: After the Bell

A.I. Anxiety and Earnings Misses Knock US Equities Lower

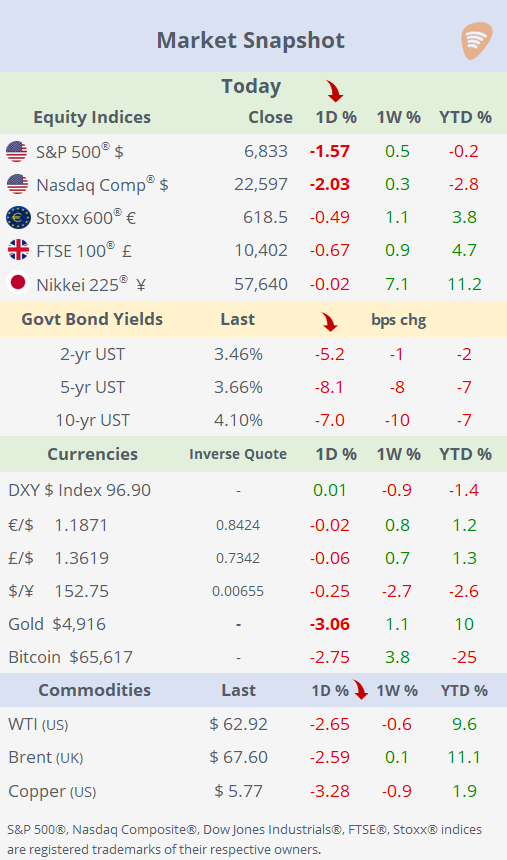

ℹ️Performance tables here.

Good evening,

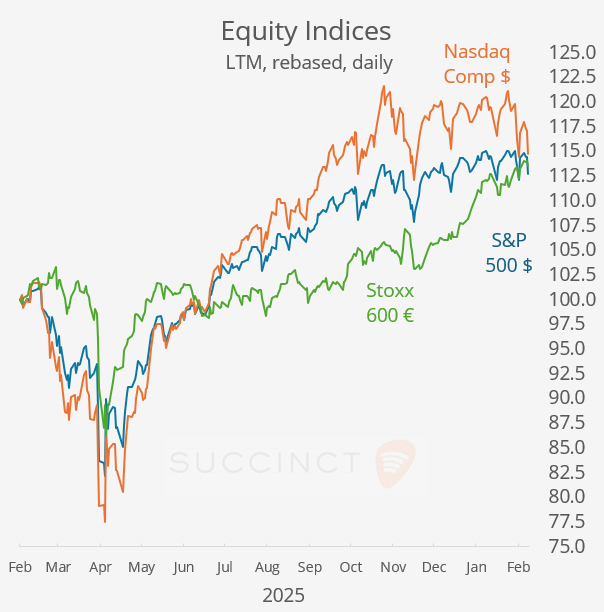

US equities sold off sharply on Thursday, with the Dow, S&P 500 and Nasdaq all retreating as Big Tech led a renewed tech rout amid resurfacing concerns over AI disruption and ahead of Friday’s key US inflation print. Apple slid 4.8% on reports of delays to core AI and Siri upgrades, while Amazon and Meta fell more than 2%, extending a rotation out of megacap tech already pressured by last week’s strong jobs data and fading rate-cut expectations. Earnings added to the unease: Cisco plunged over 11% as cautious guidance reinforced fears that parts of the software and networking ecosystem could be vulnerable to AI-driven shifts, even as capex remains strong.

After the close, sentiment was more mixed: Applied Materials jumped 10% in after-hours trading on solid results tied to ongoing AI-related chip investment, while Airbnb slipped during the session but stabilised post-earnings.

Beyond equities, Treasuries rallied sharply, with the 10-year yield falling 7bp to 4.10%, its lowest close since early December, as investors sought safety; gold and silver weakened, the dollar was broadly steady, and crypto assets extended their slide, with Bitcoin nearing $65,000 after four consecutive days of losses. Attention now turns squarely to Friday’s inflation data as the next catalyst for rates and risk sentiment.

Economics: → US existing home sales (3.9mn) fell sharply (-8.4% MoM) in January to their lowest level in four years, underscoring the continued drag from high mortgage rates and poor affordability. The weak print highlights ongoing stress in the housing market and reinforces expectations that restrictive financial conditions are still biting the real economy.

→ The UK economy barely expanded in Q4’25 (+0.1% QoQ), with weak year-on-year momentum reinforcing a stagnation narrative, compounded by a December contraction in industrial (-0.9% MoM) and manufacturing (-0.5% MoM) production, strengthening expectations that the Bank of England will need to keep easing policy, potentially as soon as March.

Earnings: → In European earnings, blue-chip names including Hermès, Siemens and L’Oréal reported results, but shares saw only muted reactions, with earnings broadly in line and lacking major new catalysts.

Corporate Deals: → Schroders, the UK asset manager with £824bn in AUM, agreed to a £9.9bn takeover by US investment manager Nuveen at 612p per share, a 35% premium to the previous close, ending the independence of one of the City’s oldest firms as industry consolidation accelerates and private markets scale becomes increasingly critical. Schroders shares jumped 29% today. (Guardian)

→ SoftBank Group ramped up leverage to fund its $34.6bn investment in OpenAI, raising $27bn in new debt and selling $3.5bn of T-Mobile shares, marking Masayoshi Son’s largest-ever bet as the group also explores a potential additional $30bn investment despite OpenAI’s heavy cash burn. (FT)

→ In IPOs, in a direct listing on Nasdaq, Braiin Limited (BRAI), an Australia-based AI and machine-learning platform spanning AgTech, CXaaS and PropTech, began trading at $39, more than doubled on its debut but closed 15% higher, giving the company an implied market valuation of roughly $5.6bn.

→ Arko Petroleum (APC), a US-based independent fuel and convenience retailer, raised $200mn in its IPO priced at $18 per share, implying a valuation of approximately $808mn at pricing as its shares began trading on Nasdaq. Shares closed a touch weaker on their debut day.

Day Ahead:

Data → US CPI (Jan) 2.5% expected; Germany PPI. Earnings → Safran, NatWest, Enbridge.

See you tomorrow.

Copyright © 2026 Succinct.

All rights reserved. This publication contains proprietary content and is intended solely for the recipient’s personal use. Disclaimer: Our service is for informational purposes only and does not constitute personal financial advice.