Thu 12 Mar: After the Bell

Hormuz Crisis Triggers Global Risk-Off, Geopolitics Roil Markets Ahead of Fed

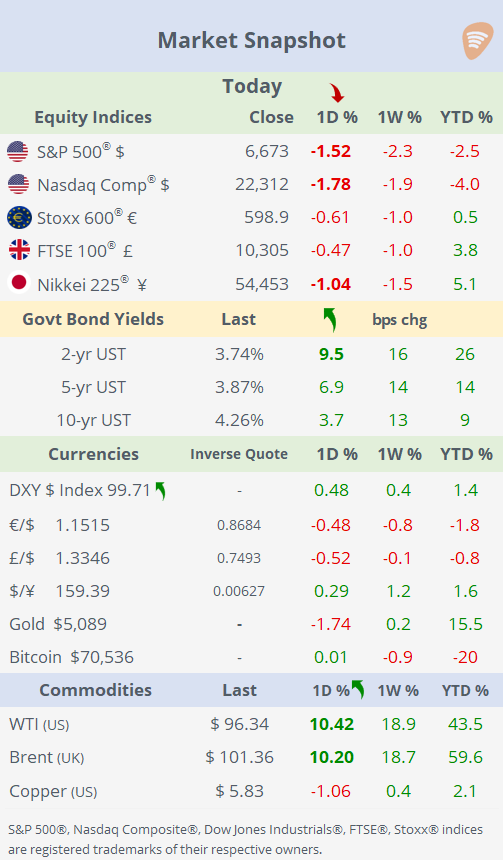

ℹ️ Today’s performance tables.

Good evening,

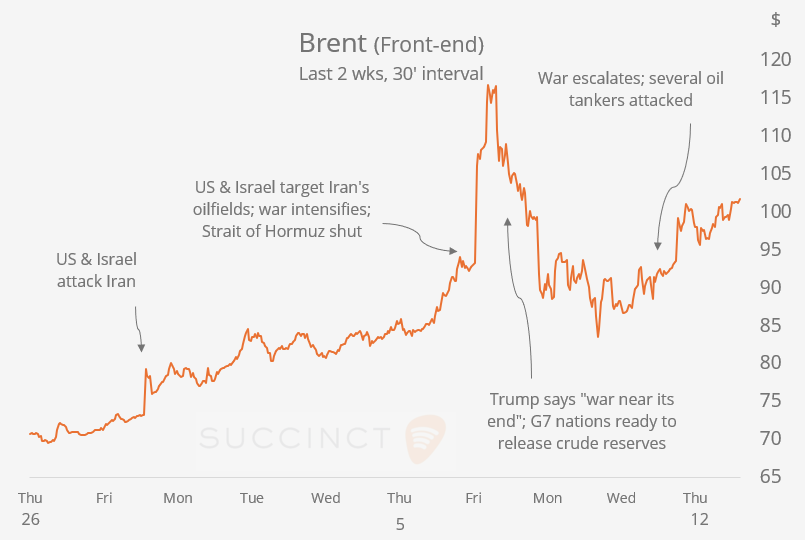

Markets turned decisively risk-off as the Iran conflict intensified, triggering a broad sell-off across global assets. US equities fell around 1.5%, with the S&P 500, Dow and Russell 2000 closing at their lowest levels of the year, while volatility spiked and the VIX jumped to 27%. At the same time, Brent crude surged back above $100 again, rising more than 10% on the day, as disruptions in the Strait of Hormuz, through which roughly 20% of global oil flows, deepened following attacks on multiple commercial vessels and widening strikes across the Gulf.

The geopolitical escalation gathered pace after Iran’s new Supreme Leader vowed to keep the Strait closed and warned of expanding the conflict, while Iranian forces continued targeting shipping and regional infrastructure. Drone and missile attacks were reported across the Gulf, including strikes involving vessels and attempted drone attacks in Kuwait, underscoring the growing regional spillover of the war.

Safe-haven flows followed: the $ index climbed to a three-month high near 100 points, while Treasury yields moved higher as investors reassessed inflation risks tied to the energy shock. Front-end yields led the move, with the 2-year Treasury rising roughly 10 bps to 3.74%, the highest since August, as markets look ahead to the Fed’s policy meeting in five days.

Economics: → US weekly initial jobless claims came in at 213,000, broadly in line with expectations, indicating a stable labour market. Housing starts rose to an annualised pace of 1.48mn units, above expectations, suggesting resilient construction activity despite elevated mortgage rates.

→ Turkey’s central bank kept its policy rate unchanged at 37%, in line with expectations, pausing its easing cycle as policymakers cited geopolitical uncertainty and rising energy prices that could pressure inflation.

Earnings: → In Europe, BMW (+1%), RWE (+4%) and Daimler Truck (+4%) reported today, with shares rising in Frankfurt as results were broadly solid and reassured investors. The positive reaction suggested few negative surprises, supporting sentiment toward German cyclicals and industrials.

Corporate Deals: → In M&A, privately-held Fertitta Entertainment is in exclusive talks to acquire Caesars Entertainment (mcap $5.8bn) for $7bn, offering ~$34 per share after topping a rival bid from Carl Icahn’s Icahn Enterprises. Shares in Caesars jumped 12% on the news, though discussions remain preliminary and may not lead to a deal.

→ In IPOs, PayPay (PAYP), a Japanese digital payments and fintech platform backed by SoftBank, priced its Nasdaq IPO at $16 per share, raising $880mn and valuing the company at $12.7bn. The stock had a positive debut, rising over 7% in early trading, as investors backed the firm’s leading position in Japan’s fast-growing cashless payments market.

Day Ahead:

Data → US PCE inflation, Michigan consumer sentiment, JOLTs jobs, durable goods; €-zone industrial production; UK GDP. Earnings → None scheduled.

See you tomorrow.

Copyright © 2026 Succinct.

All rights reserved. This publication contains proprietary content and is intended solely for the recipient’s personal use. Disclaimer: Our service is for informational purposes only and does not constitute personal financial advice.