Thu 16 Apr: After the Bell

Risk-On Mood Extends as Iran Deal Hopes Build

📈 Today’s performance tables.

Good evening,

Markets traded firmer on easing geopolitical tensions after Trump said a deal with Iran was “looking very good” and announced a 10-day Israel-Lebanon ceasefire, helping lift risk sentiment as investors also looked for progress toward reopening the strategically vital Hormuz Strait. The S&P 500 and Nasdaq edged higher to fresh records on hopes that a broader regional de-escalation could reduce energy supply risks and temper recent volatility.

On the policy front, Fed Governor Stephen Miran struck a slightly more hawkish tone, saying inflation appears stickier and the underlying composition has worsened, leaving less reason for accommodative policy than previously thought.

Separately, former Treasury Secretary Henry Paulson warned US authorities should prepare a contingency plan against a potential collapse in Treasury demand, noting that any failed funding scenario could have severe consequences and may ultimately require Federal Reserve intervention as a buyer of last resort.

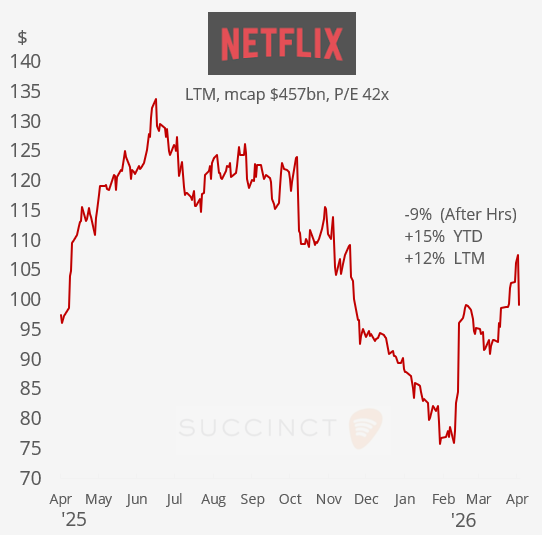

Netflix (mcap $457bn) plunged 9% in after-hours trading despite reporting Q1 revenue of $12.3bn (+16% YoY), marginally above consensus, and beat EPS estimates but disappointed on its revenue and EPS outlook for Q2.

Q1 was supported by subscriber growth, advertising revenue and recent price increases, but investors appear focused on guidance and management changes, with co-founder Reed Hastings stepping down as chairman. Recent strategic moves also include abandoning its proposed $83bn Warner Bros. Discovery assets deal (collecting a $2.8bn breakup fee) and acquiring Ben Affleck’s AI production startup InterPositive for up to $600m.

Earnings: → Financial earnings were mostly uneventful: US Bancorp and Bank of New York Mellon broadly met or modestly beat estimates, with little stock reaction.

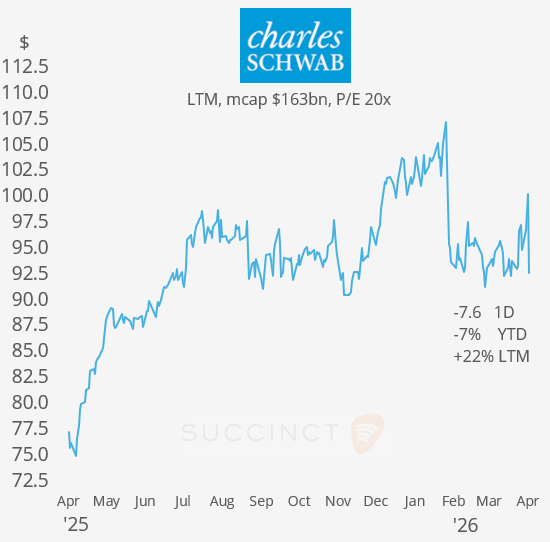

Discount broker leader Charles Schwab (mcap $161bn) was the outlier, falling about 8% despite strong headline numbers: record revenue of $6.5bn (+16% YoY), EPS of $1.43 (+38%), trading volumes up 34%, and $140bn of net new assets lifting total client assets to $11.8tn. The selloff suggests investors focused less on the quarter itself and more on slower cash-sorting normalisation, margin pressure, and softer forward net interest revenue expectations.

→ Abbott Labs (mcap $167bn) fell about 5% despite a slight earnings beat after it cut full-year profit guidance to reflect dilution from its Exact Sciences acquisition, while Q2 EPS guidance also came in light. Shares lost 23% YTD to their lowest level in nearly 3 years.

Economics: → US industrial production fell -0.5% MoM (weaker than expected), while initial jobless claims came in at 207k, below forecasts and still consistent with a resilient labour market, a mixed macro signal of softer manufacturing but ongoing employment strength.

→ China’s Q1 GDP growth of +5.0% YoY was better than expected (consensus +4.8%), accelerating from +4.5% in Q4 and landing at the top end of Beijing’s full-year target range, a near-term positive signal for markets. However, the details were mixed: industrial production +5.7% YoY beat expectations (+5.5%), but retail sales +1.7% YoY missed forecasts (+2.3%) and slowed sharply from +2.8% in Jan-Feb, suggesting the recovery remains manufacturing/export-led rather than consumer-led.

→ UK GDP (Feb) rose +0.5% MoM (vs +0.1% exp) and +1.0% YoY, the strongest monthly gain since January 2024, suggesting the economy entered Q2 with better momentum than feared.

Deals: → In the beverages sector, Sazerac Co, the privately held New Orleans owner of Buffalo Trace, is reportedly bidding around $15bn ($32/share) for Brown-Forman (mcap $13.5bn), the Louisville-based listed maker of Jack Daniel’s. France’s Pernod Ricard is also said to be in discussions, raising the prospect of a competitive takeover process for one of the sector’s best-known US names.

→ St Louis-based Industrial tech company ESCO Technologies ($7.7bn) agreed to acquire Megger Group from The Burndy Group (TBG) in a $2.35bn cash-and-stock deal, adding utility testing and grid-monitoring products to its platform in a transformational expansion of its power infrastructure business.

→ In IPOs, Madison Air Solutions, a US indoor air quality and HVAC systems manufacturer supplying ventilation, filtration and cooling solutions for data centres, healthcare and industrial facilities, raised $2.2bn at a $13.2bn valuation and was priced at $27, the high end of the guidance range. Shares rallied 18.5% on their NYSE debut, lifting their market value to roughly $15.7bn. It was the largest industrials IPO in the US since 1999.

→ Arxis, a US aerospace & defence components manufacturer supplying mission-critical electronic and mechanical parts such as sensors, RF/microwave systems, raised $1.1bn at an $11bn valuation and was priced at $28, the top end of the indicative range. Shares rallied 37% on their Nasdaq debut.

→ In upcoming IPOs, Belgium-based Belron, the world’s largest auto glass repair and replacement group (owner of Autoglass), is preparing an Amsterdam IPO at a potential €30-40bn valuation, which would rank among Europe’s biggest listings in recent years. Backed by D’Ieteren Group and Clayton Dubilier & Rice, the deal would be a welcome boost for Europe’s sluggish IPO market after shareholders reportedly favoured Amsterdam over New York.

→ X-Energy, the Maryland-based, Amazon-backed private small modular nuclear reactor developer, is targeting a $7.5bn valuation in its planned IPO, seeking to raise $815mn by selling shares at $16–19. The deal reflects rising investor interest in nuclear power tied to AI-driven data centre electricity demand.

Day Ahead:

Data → none of significance. Earnings → Truist Financial, State Street, Marsh & McL.

See you tomorrow.

Copyright © 2026 Succinct.

All rights reserved. This publication contains proprietary content and is intended solely for the recipient’s personal use. Disclaimer: Our service is for informational purposes only and does not constitute personal financial advice.