Thu 19 Feb: After the Bell

Rising Tensions, Credit Concerns Push Markets Lower. All in 4 mins.

Good evening,

Markets turned risk-averse as heightened geopolitical tensions, mixed corporate earnings, and a negative headline in private credit weighed on sentiment, pushing equities lower across both the US and Europe. Energy was the clear outlier, with oil rallying again on rising Middle East risk, while bond yields were little changed and the $ climbed to a four-week high. Notably, gold showed only a muted response despite the Iran-related headlines, suggesting positioning fatigue rather than a full-blown flight to safety.

In geopolitics, Trump said the US will decide within 10 days whether to strike Iran or pursue a deal, as a major US military build-up in the Middle East pushed Brent crude up over 6% in the past week to a six-month high on rising conflict risk.

Credit fund manager Blue Owl Capital (mcap $18bn) has restricted investor withdrawals from its retail-focused private credit fund (OBDC II) and shifted to periodic capital returns, triggering a 6% sell-off in its stock and broader private credit names (Blackstone & Apollo -5%, Ares -3%) as liquidity and valuation concerns in the rapidly-expanding private credit market were reignited.

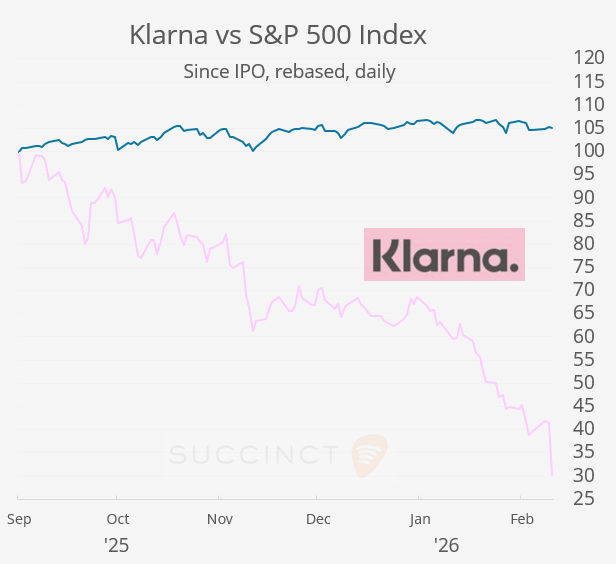

A notable mover today was Swedish fintech Klarna (mcap $5bn), with shares plunging 27% after it reported a $273m net loss for 2025 and sharply higher credit provisions, as loan losses rose alongside the expansion of longer-term, interest-bearing products that require upfront provisioning. The sell-off deepens Klarna’s post-IPO slump to ~66% since its September New York listing, reflecting investor concern that rising credit risk is undermining its pivot from buy-now-pay-later toward a broader neobank model.

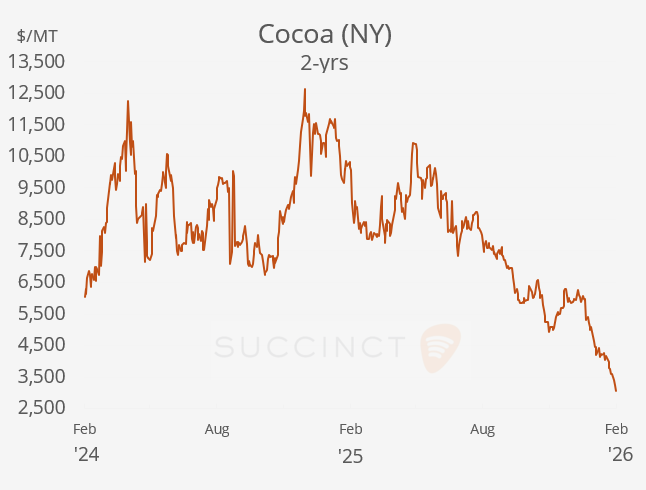

In other commodity markets, cocoa futures (May) fell 8% today to their lowest levels since mid-2023, driven by a broad selloff as ample stockpiles in the Ivory Coast, softer global demand, and buyer resistance at current prices overwhelmed buying interest.

Earnings: → Airbus: Shares fell 7% after it cut its full-year guidance and flagged persistent supply chain bottlenecks and execution risks, disappointing investors who had been expecting a smoother ramp-up in deliveries. Stock is down 6% YTD.

→ Deere & Co: rallied 13% after beating revenue and profit expectations and raised its outlook, driven by robust demand in its core farm equipment segment and better pricing power, a clear bullish surprise for investors. Deere’s stock is 44% higher this year.

→ Walmart (higher revenues in grocery and online) and Alibaba also reported results today. Still, their shares showed little reaction, as earnings and outlooks were largely in line with expectations and didn’t contain standout catalysts for stock moves.

Economics: → The US trade deficit widened sharply in December to about $70bn, materially worse than expected, largely driven by a steep drop in gold exports rather than a broad-based deterioration in trade flows. For 2025 as a whole, the deficit was essentially flat at ~$902bn versus 2024, despite record imports, underscoring that tariff changes reshuffled timing and composition of trade but did little to alter America’s structural role as a large net importer.

US weekly initial jobless claims fell to 206k, below expectations, reinforcing the picture of a resilient labour market with layoffs remaining subdued despite broader signs of economic cooling.

Corporate Deals: → US digital health operator Hims & Hers Health (mcap $3.6bn) agreed to buy Australia-based and privately held Eucalyptus for $1.15bn, expanding its presence in the telehealth/wellness sector into Australia, Japan and bolstering reach in the UK, Germany and Canada. The deal extends Hims & Hers’ international footprint even as the company navigates a patent lawsuit related to its weight-loss drug offerings.

→ US steelmaker Steel Dynamics (mcap $28bn) and Australian conglomerate SGH submitted a sweetened “best and final” bid for Australian steelmaker BlueScope Steel, valuing the company at $11bn, a ~56% premium to its 52-week VWAP. Under the structure, SGH would acquire all assets and on-sell BlueScope’s North American operations to Steel Dynamics, reflecting strategic demand for domestic steel capacity amid import tariffs.

Day Ahead:

Data → US PCE inflation, personal income and spending, new home sales, Michigan consumer sentiment, GDP growth prelim; UK retail sales; developed countries PMIs. Earnings → Warner Bros Disc, Anglo American, Air Liquide.

❗USMD will take a break tomorrow and return on Monday.

Copyright © 2026 Succinct.

All rights reserved. This publication contains proprietary content and is intended solely for the recipient’s personal use. Disclaimer: Our service is for informational purposes only and does not constitute personal financial advice.