Thu 19 Mar: After the Bell

Oil, Gas and Rates: Markets Struggle to Price the Shock

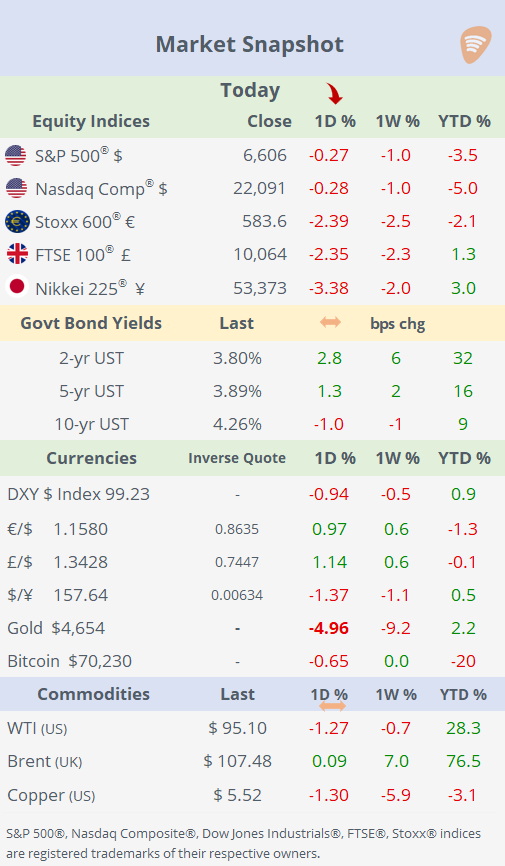

ℹ️ Today’s performance tables.

Good evening,

Global markets endured a highly volatile session on Thursday, driven by a sharp escalation in the Middle East conflict and a heavy slate of central bank decisions. Risk assets swung aggressively throughout the day, with US equities opening sharply lower before staging a partial recovery, while European and Asian indices fell more firmly, reflecting a broader risk-off tone as investors struggled to price a rapidly evolving geopolitical backdrop alongside shifting monetary policy expectations.

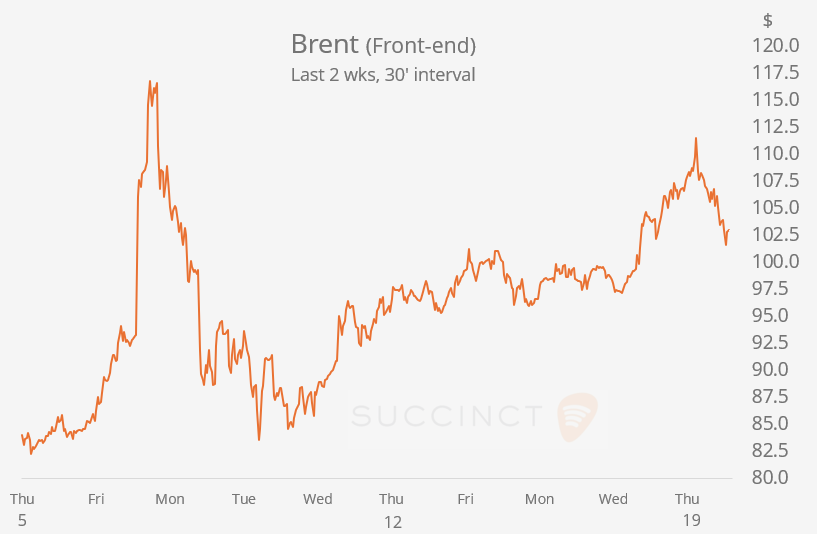

The conflict moved decisively toward energy infrastructure, amplifying market stress. Iranian strikes on Qatar’s Ras Laffan complex, the world’s largest LNG facility, responsible for roughly a fifth of global supply, raised fears of severe disruption, while earlier attacks on Iran’s South Pars field underscored the vulnerability of key supply hubs. Oil prices reflected the uncertainty, with Brent surging as much as 9% intraday to briefly touch $119 before pulling back to around $109. In gas markets, Europe’s benchmark Dutch TTF contract jumped ~11% to €60.75, the highest level in three years, highlighting the growing risk premium across energy markets.

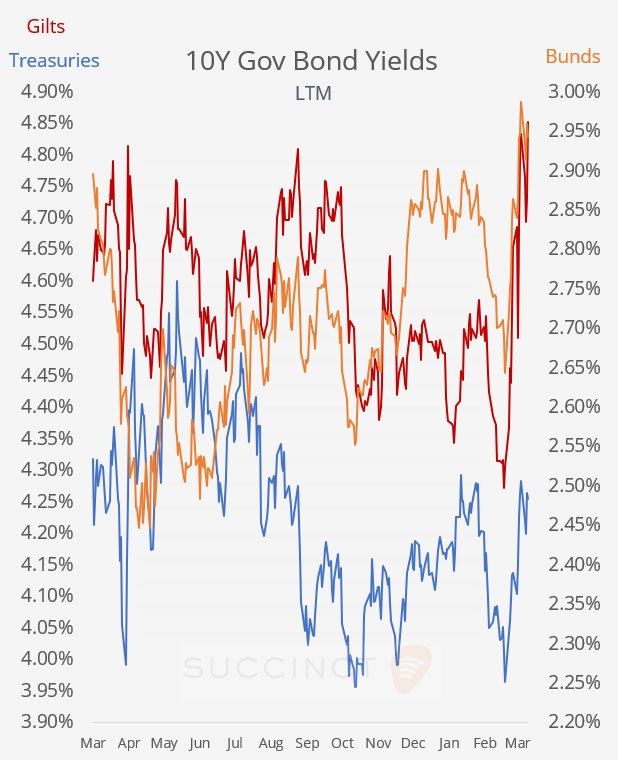

At the same time, central banks added another layer of complexity. Yesterday, the Fed; today, the ECB, Bank of England, Bank of Japan, and Swiss National Bank, all highlighted rising inflation risks tied to energy prices, reinforcing concerns that a prolonged shock could delay or even reverse the path toward rate cuts. Bond markets reacted accordingly, with yields spiking; 2-year Treasuries briefly approached 4% (up 32 bp in the past 4 weeks) before retracing into the close.

Across asset classes, the price action reflected both macro and geopolitical stress. The $ weakened sharply, reversing recent gains, while gold (-5%) and silver (-8%) sold off despite the risk backdrop, pointing to tighter financial conditions and rising real yields. Overall, markets are increasingly trading a protracted energy shock, where volatility remains elevated, and both growth and inflation expectations are being repriced in real time.

Monetary Policy: → The ECB kept rates unchanged (deposit at 2%, refinancing at 2.15%) as expected, for a sixth straight meeting, but struck a more cautious tone, warning that the surge in energy prices will have a “material impact” on near-term inflation. Officials, led by Christine Lagarde, highlighted that the Middle East conflict has significantly increased uncertainty, creating upside risks to inflation and downside risks to growth.

Updated projections reinforced the shift: inflation is now seen at ~2.6% (vs. 1.9% prior), while growth was downgraded to ~0.9%, pointing to a more stagflationary near-term backdrop even as inflation is still expected to return to target over the medium term.

→ The Bank of England held rates unchanged at 3.75%, as anticipated, but delivered a more hawkish message, warning that a prolonged energy shock from the Middle East could push inflation higher and potentially require tighter policy. While Governor Bailey struck a slightly more cautious tone, noting it was too early to draw firm conclusions, the MPC signalled that rate cuts are no longer in view, and hikes are a possibility if price pressures persist.

Markets reacted sharply: UK Gilts sold off aggressively, with 2-year yields jumping to ~4.4% (one of the biggest moves in years) and 10-year UKT yields nearing 4.86% (+54bp in the last 4 weeks), as investors repriced toward a more hawkish path; the £ also strengthened significantly (+1.5%) on the shift in expectations.

→ The Bank of Japan held its policy rate unchanged at 0.75%, extending its pause since December, as policymakers adopt a wait-and-see approach amid Middle East tensions and volatile energy markets. Despite the hold, the bank maintained a tightening bias, with Governor Ueda signalling that further hikes remain likely if inflation evolves as expected, and some board members already pushing for an earlier move toward higher rates. The ¥ appreciated ~1.4% to 157.6 today.

→ The Swiss National Bank held its policy rate at 0% for a third consecutive meeting, as expected, while highlighting ongoing risks from Swiss franc strength driven by safe-haven flows. Policymakers signalled a readiness to intervene in FX markets, and even consider negative rates again, to counter excessive appreciation and protect price stability amid geopolitical uncertainty.

Earnings: → Alibaba (mcap $300bn) shares fell ~7% after missing revenue expectations and reporting a sharp drop in net income (-66% YoY), as heavy spending and competitive pressures weighed on margins. While cloud and AI segments showed strong growth, the market focused on weak core e-commerce performance and deteriorating profitability. Overall, the results raised concerns that growth is coming at the expense of earnings, with limited near-term visibility on margin recovery.

Business News: → Uber (mcap $157bn) will invest up to $1.25bn in Rivian Automotive (mcap $19bn) and purchase up to 50k autonomous vehicles, as it accelerates its shift toward robotaxi fleets. The partnership includes an initial rollout starting in 2028, with plans to scale across multiple cities, positioning Uber as a platform and fleet operator rather than a developer of self-driving technology. Rivian’s stock advanced ~2.5% but remains 20% lower this year.

→ The Federal Reserve proposed easing bank regulations, cutting capital requirements for large US lenders by 4.8%, reversing part of the post-2008 GFC tightening. The move is expected to boost lending, share buybacks, and consolidation, with smaller banks benefiting even more from the proposed reductions.

Corporate Deals: → In the US industrials sector, 3M (mcap $74bn) and Bain Capital agreed to acquire Madison Fire & Rescue for $1.95bn, a unit of privately held Madison Industries, combining it with 3M’s Scott Safety unit to form a new fire and safety platform. 3M will hold a 50.1% stake and receive $700m in cash, with Bain owning the remainder.

→ In the chemicals sector, Ecolab (mcap $72bn) is nearing a deal to acquire CoolIT Systems from KKR for $4.5–5bn, in a transaction that could be announced as soon as next week but remains unconfirmed. The target, backed by KKR and Mubadala Investment Co, provides liquid-cooling solutions for AI-driven data centres, marking a sharp valuation increase since 2023 and highlighting strong demand for AI infrastructure.

Day Ahead:

Monetary Policy → Russia. Data → Canada PPI and retail sales; Germany PPI. Earnings → None.

See you tomorrow.

Copyright © 2026 Succinct.

All rights reserved. This publication contains proprietary content and is intended solely for the recipient’s personal use. Disclaimer: Our service is for informational purposes only and does not constitute personal financial advice.