Thu 2 Apr: After the Bell

War Clouds Persist: Oil Spikes Again and Markets Search for Direction

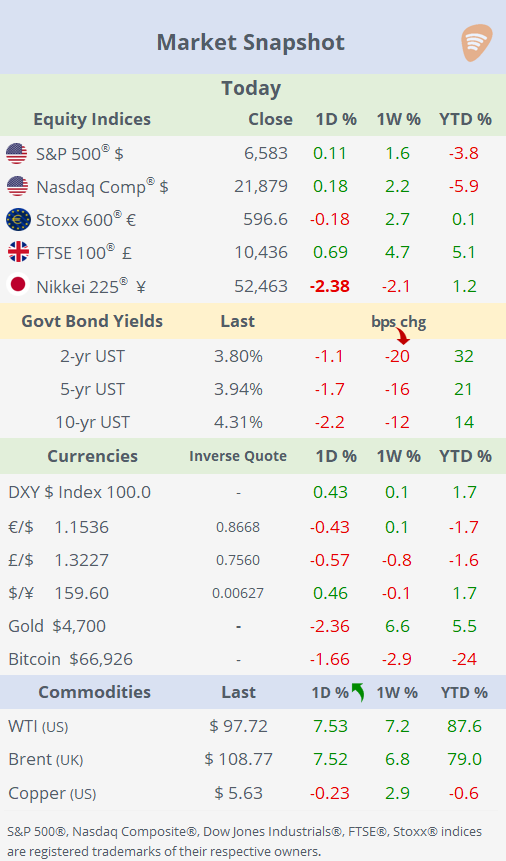

📈 Today’s performance tables.

Good evening,

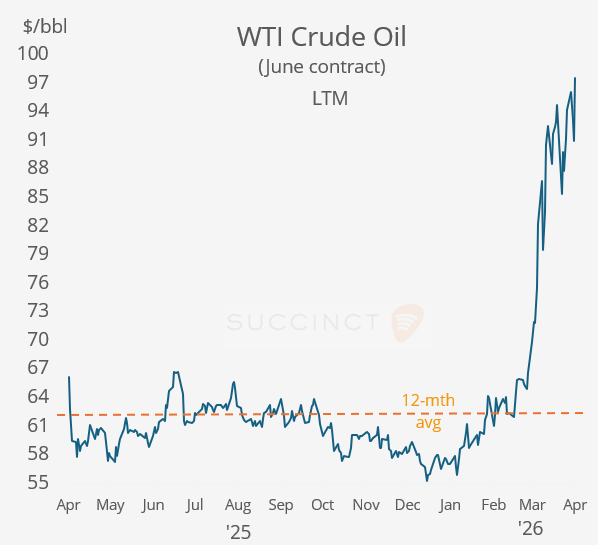

Geopolitics remained firmly in the driver’s seat, with the ongoing US-Israeli conflict with Iran continuing to rattle global markets. Front-month (May) oil futures surged above $110 amid fears of a prolonged disruption, as uncertainty around the Strait of Hormuz kept investors on edge, with some warning that a sustained closure could tip the €-zone into recession.

Market sentiment deteriorated after Trump’s primetime address last night offered little clarity on how the conflict would be wound down over the next two to three weeks, despite claims that military objectives were “nearing completion.” The lack of a clear timeline weighed on risk assets early in the session, reinforcing concerns that the war, and its economic fallout, could drag on.

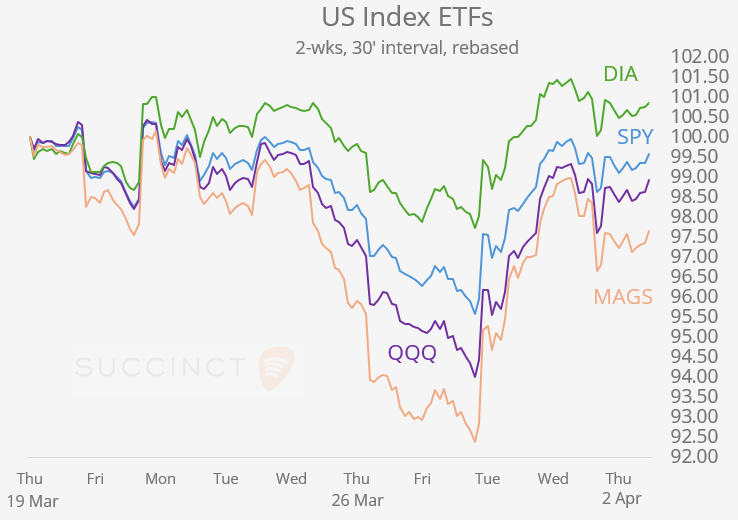

US equities initially sold off sharply but staged a recovery to finish modestly higher on the day, supported by signs of potential de-escalation after Iran indicated it was working with Oman on a protocol to manage traffic through the Strait of Hormuz. The rebound highlighted how sensitive markets remain to any headlines suggesting even a partial reopening of key energy routes.

Looking ahead, liquidity is set to thin significantly with markets closed for Good Friday across the US and Europe, leaving only parts of Asia, notably Tokyo and Shanghai exchanges, open, which could amplify volatility around any further geopolitical developments.

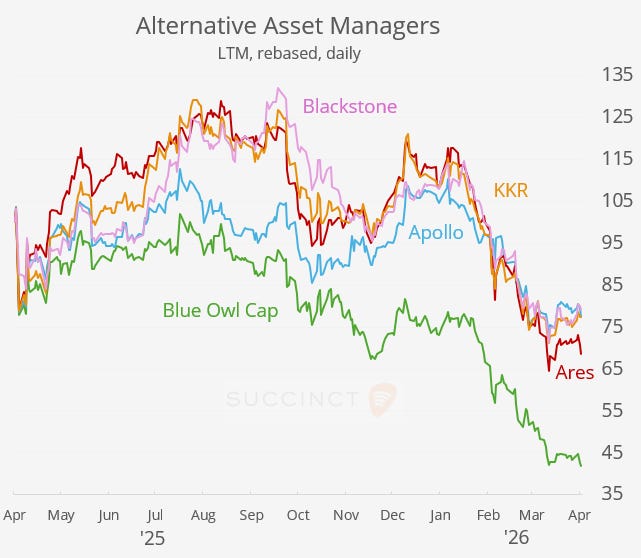

→ In the private credit sector, Blue Owl Capital (mcap $13bn) faced $5.4bn in redemption requests in Q1 across two private credit funds (22% and 41% of assets), forcing it to cap withdrawals at 5% as outflows accelerate. The scale of redemptions highlights mounting liquidity pressure in private credit, drawing regulatory attention and raising concerns over sustained outflows and fee income erosion. Blue Owl Cap shares are down 43% YTD and -60% in the LTM.

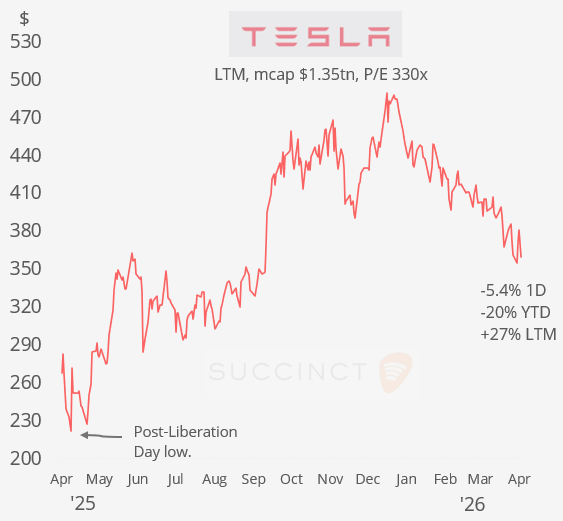

→ Tesla reported Q1 deliveries of 358k vehicles, missing expectations and marking one of its weakest quarters in years, with a record build-up in inventory. The data reinforces a deepening demand slowdown amid rising competition and fading EV incentives, weighing on sentiment despite Tesla’s pivot toward AI, robotics and autonomous driving. Shares fell ~6% today and are -20% YTD.

Economics: → US initial jobless claims fell to 202k, below estimates, signalling a still-resilient labour market and supporting a modestly positive risk sentiment.

→ Swiss inflation rose to 0.3% YoY, the highest in a year, but came in below expectations, pointing to mild price pressures that remain contained and unlikely to shift policy near term.

Deals: → Global M&A surged to $1.2tn in Q1, with a record 22 mega-deals above $10bn, marking a third consecutive $1tn+ quarter despite geopolitical tensions and AI-driven uncertainty. Activity was led by the US ($630bn) and a sharp rebound in Europe (+82% YoY), with large transactions spanning energy, healthcare and consumer sectors. Momentum remains strong as corporates stay active, but risks from Middle East conflict, elevated oil prices and softer tech dealmaking could temper activity ahead. Deals included Unilever–McCormick, Sysco–Jetro Restaurant Depot, Devon Energy–Coterra Energy and GIP+EQT–AES Corp.

→ KKR raised $23bn for its North America-focused private equity fund (NAX4), its largest regional vehicle, targeting opportunistic deals as companies stay private longer. The strong raise underscores sustained investor demand for private markets, with KKR highlighting ~23% gross returns from prior funds and private equity AUM growing to $229bn. Private equity exits fell 36% YoY to $103bn in Q1’26 amid AI-driven volatility and geopolitical risks, highlighting a tougher exit environment and delaying capital recycling for sponsors.

→ Amazon is reportedly in talks to acquire mobile satellite company Globalstar (mcap $9.5bn) for ~$9bn, aiming to accelerate its low-earth-orbit satellite strategy and compete with SpaceX’s Starlink network. The move follows SpaceX’s confidential IPO filing, where Starlink is seen as a key driver of a potential ~$1.75tn valuation, underscoring intensifying competition in satellite internet. GSAT shares gained 8% today and 21% YTD.

→ Goldman Sachs completed its $2bn acquisition of Innovator Capital Management, boosting its ETF platform to $90bn in assets and expanding into the fast-growing active ETF segment. The deal strengthens Goldman’s push into outcome-oriented strategies, as active ETFs gain traction amid rising demand for flexibility and cost efficiency versus traditional passive products.

Day Ahead:

Data → US non-farm payrolls. Earnings → n/a

Happy Easter🐰, see you next week.

Copyright © 2026 Succinct.

All rights reserved. This publication contains proprietary content and is intended solely for the recipient’s personal use. Disclaimer: Our service is for informational purposes only and does not constitute personal financial advice.