Thu 22 Jan: After the Bell

Risk Assets Gain on Calmer Backdrop, Gold Rally Persists; Your 5’ evening market wrap

ℹ️ Today’s performance tables & charts on the ‘Market Data’ post.

Good evening,

Global equities advanced on Thursday as solid US data and a moderation in geopolitical tensions supported risk appetite, with most US sectors ending higher. Communication Services outperformed, led by a strong rally in Meta shares, while Intel weighed on sentiment after the close, sliding about 6% on a weaker earnings outlook.

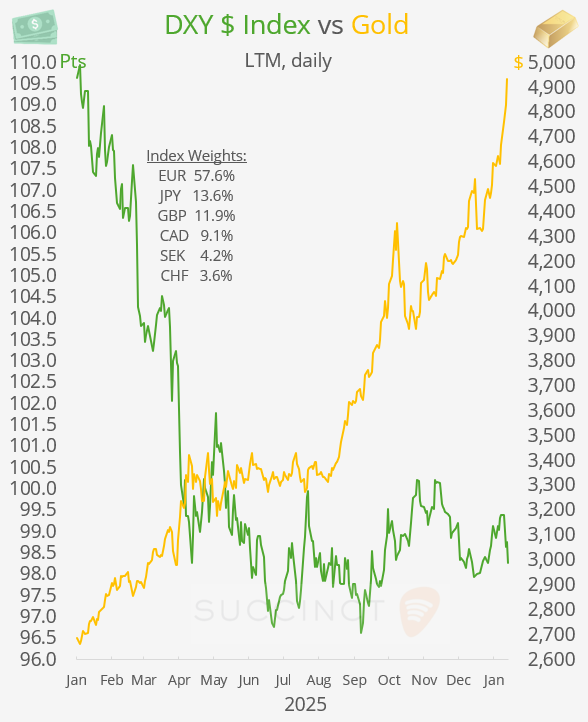

Safe-haven demand nonetheless remained firm, with precious metals extending their rally: gold traded just shy of $5,000 and silver moved closer to $100, after Goldman Sachs raised its year-end gold target to $5,400.

In FX, the $ weakened broadly, falling most against the €, £, the Australian dollar and the Swiss franc, leaving the DXY Index near its lowest level of the month. Core bond yields were little changed, with the 10-year Treasury closing around 4.25% as markets continue to price a roughly 95% probability that the Fed will keep rates unchanged at its meeting in five days.

The mega-cap notable mover today was Meta (mcap $1.6tn), which rallied >5% after a bullish analyst note from Jefferies reiterated a strong buy and touted Meta as undervalued relative to its tech peers.

Abbott Labs (mcap $190bn) fell 10% after its Q4 revenue missed consensus estimates despite EPS meeting expectations, with weakness in its nutrition and diagnostics segments weighing on the top line. The miss, along with mixed guidance and ongoing segment pressure, overshadowed otherwise solid earnings and dampened investor sentiment.

A headline making noise today is Trump’s $5bn lawsuit against JPMorgan Chase, alleging the bank improperly closed family-business accounts after the 2021 Capitol riot for political reasons. JPM dismissed the claims as meritless, saying it does not discriminate based on political beliefs.

Earnings: → GE Aerospace (mcap $312bn) beat Q4 earnings and revenue expectations and reported a robust order growth, but shares fell over 7% as investors reacted to a softer near-term revenue outlook and signs of slowing growth momentum. Despite a strong backlog and solid earnings beat, the market appeared disappointed with the implied moderation in future top-line acceleration, tempering sentiment. GE shares have rallied 57% in the LTM.

→ Intel reported after the close on Thursday. Shares fell about 6% in after-hours trading after the company reported a wider-than-expected Q4 net loss of $333m, as heavy spending to ramp up next-generation chip production weighed on results. Revenue declined to $13.7bn from $14.3bn a year earlier. Looking ahead, Intel guided to another loss in Q1’26, forecasting a 21c per-share loss and revenue of ~$12bn, reinforcing concerns over near-term profitability.

→ Procter & Gamble’s (mcap $351bn) results were generally well received, and its shares traded slightly firmer (+2%), but today’s corporate earnings overall did not meaningfully drive broader market sentiment. PG is down 9% in the LTM.

Economics: → The final US Q3’25 GDP reading showed the economy expanded 4.4% annualized, above the prior estimate of 4.3% and topping expectations, marking the strongest growth in two years. The upward revision reflected stronger exports and business investment, with solid consumer spending underpinning momentum, signalling continued resilience in the economy.

On the inflation front, the delayed US PCE inflation data for October and November showed headline inflation steady at 2.7% and 2.8% YoY, with core PCE holding near 2.8% YoY, broadly in line with expectations. The figures reinforce the view that inflation is stable but sticky, keeping the Fed cautious as it approaches its next policy meeting.

In the labour market, US weekly jobless claims came in at 200k, slightly below expectations and consistent with a still-resilient labour market.

→ Turkey’s central bank cut its key policy rate by 100 bp to 37%, marking its fifth consecutive reduction as part of an ongoing easing cycle amid slowing inflation. However, the cut was smaller than market expectations. The decision reflects a cautious approach given lingering inflation risk and follows signs that the underlying inflation trend has eased but remains volatile. The Turkish lira barely moved and is 21% weaker over the last twelve months.

Corporate Deals: → In the European finance sector, Swedish buyout group EQT agreed to acquire UK-based secondaries specialist Coller Capital for up to $3.7bn, paying $3.2bn upfront with a further $500mn earn-out, in a landmark move to expand into the fast-growing market for ageing private capital assets.

The deal gives EQT immediate scale in private market secondaries, with Coller managing nearly $50bn AUM, as liquidity pressures push pension funds and other LPs to sell legacy private equity and credit fund stakes.

→ Deutsche Börse (mcap €39bn) agreed to acquire fund distribution platform Allfunds (mcap €5.2bn) for ~€5.3bn, offering a 32.5% premium via a mix of cash, DB shares and a special dividend, with financing fully committed. The deal strengthens Deutsche Börse’s post-trade and fund services franchise.

→ In IPOs, BitGo Holdings, a leading US crypto custody firm, priced its initial public offering at $18 per share, above the marketed range, raising about $213mn and valuing the company at roughly $2bn. The IPO marks one of the first major digital asset company listings of 2026 and tests investor appetite in the crypto sector amid regulatory uncertainty and recent market volatility. Goldman and Citi led the offering, with trading set to begin on the NYSE under the ticker “BTGO.”

Day Ahead:

→ Data: G7 PMIs (Flash Jan), US Michigan consumer sentiment, UK retail sales. → Monetary Policy: Bank of Japan (unch at 0.75% expected). → Earnings: Schlumberger.

See you tomorrow.

Copyright © 2025 Succinct.

All rights reserved. This publication contains proprietary content and is intended solely for the recipient’s personal use. Disclaimer: Our service is for informational purposes only and does not constitute personal financial advice.