Thu 26 Feb: After the Bell

Tech Slips on AI Fears as Investors Rotate to Bonds

Good evening,

Wall Street’s focus remains squarely on AI valuations and IT earnings, but the market’s tolerance for upside surprises is clearly shrinking. Nvidia’s blockbuster quarter, reported last night, failed to reassure investors, reinforcing concerns that expectations and bubble fears remain elevated for AI-linked stocks. The Nasdaq led declines, with Nvidia shares down 5.5% despite stellar results, underscoring how high the bar has become for the sector’s bellwether.

Nvidia’s standout results did little to calm investor nerves. Despite posting blockbuster results, with Q4 revenue surging 73% to $68.1bn and guidance beating expectations by the widest margin in two years, shares fell today (after rising 3% in extended trading yesterday) as investor focus shifted from earnings strength to concerns over AI-driven spending sustainability and valuation risk. The sell-off highlights lingering fears that surging AI investment could be forming a bubble, even as Nvidia remains the undisputed leader in AI computing.

After the close today, earnings were mixed: Dell Technologies jumped 10%, while CoreWeave fell 5%; Intuit also reported (-2%). Meanwhile, fintech Block (mcap $33bn) announced a 40% headcount reduction, sending shares 20% higher in extended trading.

In macro markets, bonds rallied on a flight to quality, pulling the US 10-year Treasury yield down to 4%, its lowest since late November, while the dollar index and crude oil were little changed.

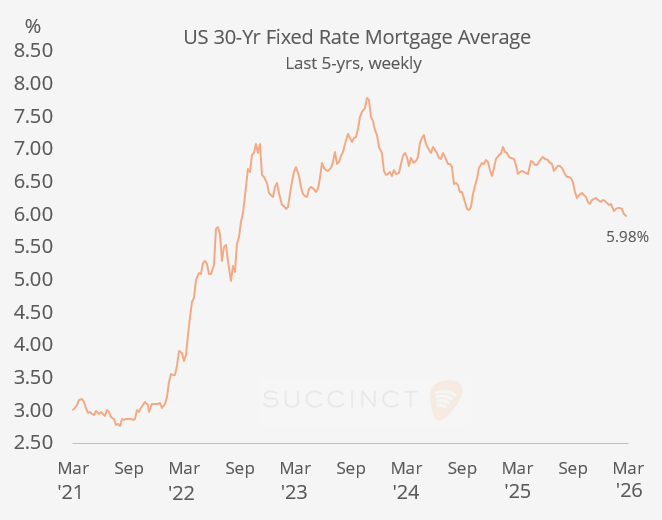

US 30-year fixed mortgage rates fell to 5.98%, dropping below 6% for the first time since September 2022, a key psychological level likely to support spring homebuying and refinancing activity, according to Freddie Mac. The decline reflects cooling inflation, economic uncertainty, and recent rate cuts by the Fed.

Earnings: → European insurers and Canadian banks reported earnings with little stock movement, while the London Stock Exchange Group surged about 9% after reporting strong 2025 results and unveiling a £3bn share buyback alongside improved profit and guidance, boosting investor confidence.

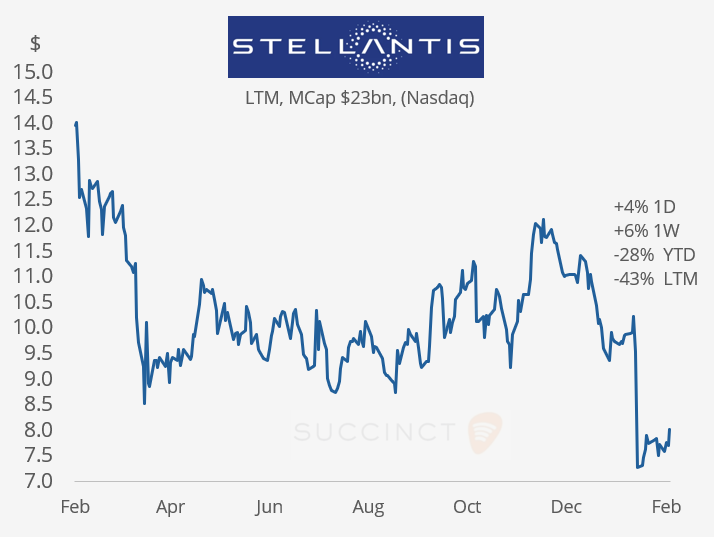

→ Italo-American carmaker Stellantis (mcap $23bn) reported an annual net loss of €22.3bn ($26bn) after taking €25.4bn in charges tied to a strategic reset, including cancelled EV projects and reduced battery manufacturing capacity. It is scaling back its EV ambitions in favour of a broader mix of electric, hybrid, and internal-combustion models, citing slower-than-expected consumer adoption of EVs. The company will issue bonds, pause shareholder payouts, and warned of a further earnings hit from Trump’s trade war as it pivots back toward petrol and diesel models in the US and Europe. Shares rose 4%, though they remain down 28% in 2026.

Data: → US weekly initial jobless claims rose modestly to 212,000, slightly below expectations, signalling a stable labour market with layoffs remaining at historically low levels.

Corporate Deals: → Texas-based investment firm Victory Capital (mcap $4.7bn) said it has submitted a rival bid for Janus Henderson (mcap $8bn) that exceeds the $7.4bn offer made in December by Nelson Peltz’s Trian Fund Management and venture firm General Catalyst. Janus shares jumped 6% today and are 12% higher YTD, while Victory’s dropped 7%.

→ Dubai Aerospace Enterprise agreed to acquire Macquarie AirFinance for $7bn from Macquarie Asset Mgt and partners, creating a 1,029-aircraft fleet across 79 countries, following a competitive bidding process that underscores strong investor appetite for aircraft assets as Boeing and Airbus struggle to ramp up production.

→ In private markets, San Francisco-based fintech Plaid was valued at about $8bn via a secondary/tender offer that provided liquidity to employees and existing investors, rather than a new VC growth round. This new valuation is up from a $6bn mark in 2025 but still below the $13.4bn peak it reached in 2021 amid the fintech boom.

Day Ahead:

Data → US PPI; Canada and India GDP; Germany, France and Spain inflation. Earnings → Holcim, BASF.

Copyright © 2026 Succinct.

All rights reserved. This publication contains proprietary content and is intended solely for the recipient’s personal use. Disclaimer: Our service is for informational purposes only and does not constitute personal financial advice.