Thu 26 Mar: After the Bell

Selloff Accelerates as Oil Shock Hits Global Markets and Yields Climb

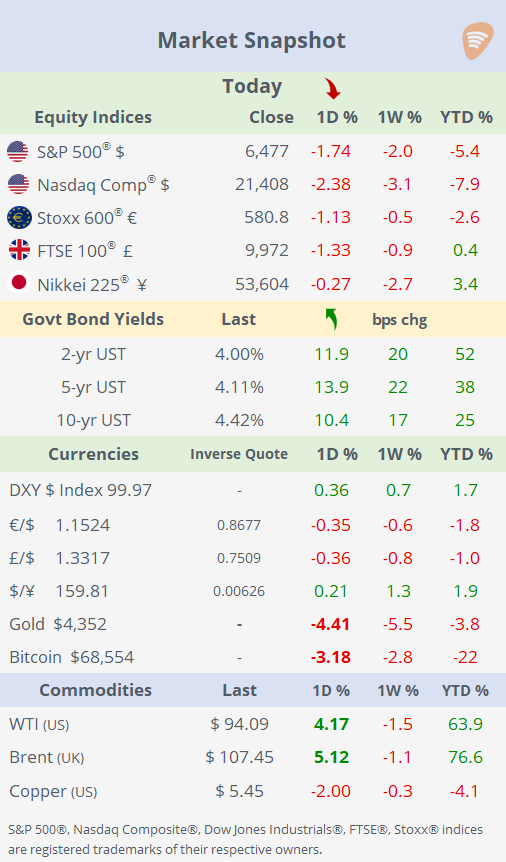

📈 Today’s performance tables.

Good evening,

Risk assets sold off sharply today as geopolitical tensions in the Middle East intensified, with fading hopes for a ceasefire driving a broad risk-off move across markets. Brent surged more than 5% to $107.50, as conflicting signals between Trump and Iran, alongside an approaching deadline for a potential deal, deepened uncertainty and kept markets on edge.

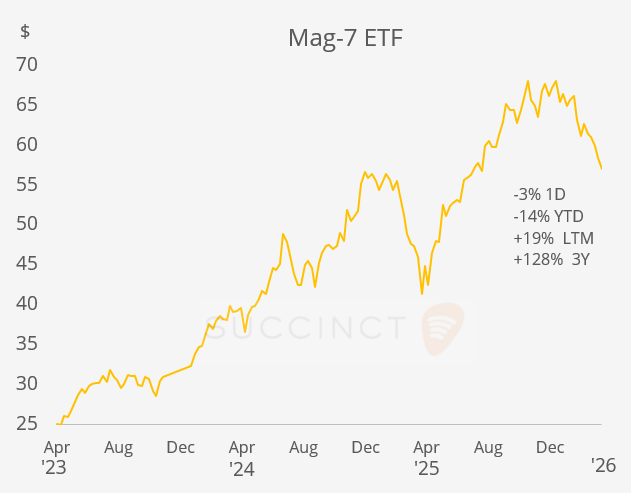

Equities fell globally, with US tech leading losses: the “Magnificent 7” dropped over 3%, while the Philadelphia Semiconductor Index plunged nearly 5%, highlighting the sensitivity of growth assets to rising rates and geopolitical risk.

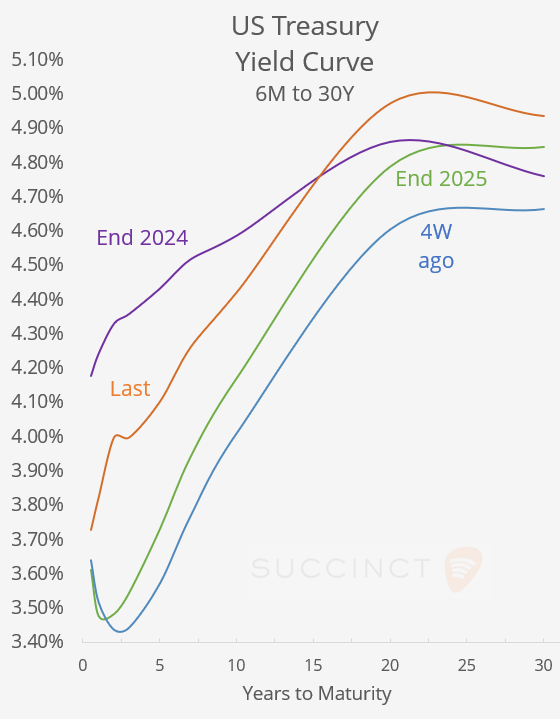

Fixed income also came under pressure, with the 2-year Treasury yield climbing back toward 4%, its highest level since June, reflecting a sharp repricing of inflation and rate expectations as higher oil prices feed through the macro-outlook. Overall, the session was defined by broad-based declines across equities, bonds, precious metals and cryptos, underscoring a market driven by uncertainty, policy risk, and energy-driven inflation fears.

Further highlighting liquidity pressures in private funds, UBS has gated withdrawals from its €400mn Euroinvest real estate fund for up to three years, citing insufficient liquidity to meet rising redemption requests. The move highlights growing stress in property funds as investors pull capital amid deteriorating economic conditions linked to geopolitical tensions.

Monetary Policy: → Banco de México cut its policy rate by 25bp to 6.75%, the lowest level in four years, surprising markets that were expecting a hold and resuming its easing cycle despite inflation still running above target. The move signals a greater focus on weakening growth and external risks, even as it raises questions about the inflation outlook and policy credibility.

→ South African Reserve Bank kept its policy rate unchanged at 6.75%, in line with expectations, as rising energy prices tied to geopolitical tensions are seen pushing inflation higher. The hold reflects a more cautious stance, with policymakers prioritising inflation risks over growth and signalling a likely pause in the easing cycle amid global uncertainty.

Deals: → Equitable (mcap $11bn) and Corebridge Financial (mcap $12bn) are set to merge in an all-stock deal, creating a $22bn retirement, asset and wealth management group with greater scale. The tie-up reflects ongoing consolidation in insurance-linked asset management, as firms seek lower cost of capital and growth via managing insurer balance sheets.

→ German household goods company Henkel (mcap €27bn) has agreed to acquire Nasdaq-listed Olaplex Holdings (mcap $1.3bn) for $1.4bn ($2.06/share, ~55% premium), continuing its acquisition push in beauty. Olaplex makes premium haircare products focused on repairing and strengthening damaged hair. The deal comes after Olaplex’s post-IPO decline, with Henkel targeting a turnaround opportunity amid weaker sales and rising competition. Olaplex shares jumped 51% on Thursday. It was listed in 2021 at $21.

→ In debt markets, New York City (rated Aa/Aa2) has scaled back a planned “mega” municipal bond issuance amid volatile market conditions, with the deal reportedly involving tax-exempt municipal debt used to fund city capital projects (infrastructure, housing, etc.). The transaction was initially expected to be one of the city’s largest but was downsized due to weak demand and rising yields, highlighting how recent market turmoil is tightening financing conditions even for high-grade public issuers. Moody’s and Fitch issued a negative outlook for the Big Apple’s debt a few days ago.

→ In IPOs, Greenland Energy Company (GLND) began trading on Nasdaq today following a $215mn SPAC merger with Pelican Acquisition Corp, Greenland Exploration Limited, and March GL. The company focuses on developing large oil and gas resources in East Greenland’s Jameson Land Basin.

Day Ahead:

Data → US Michigan consumer sentiment, UK retail sales, Spain inflation.

Earnings → PetroChina and major Chinese banks.

See you tomorrow.

Copyright © 2026 Succinct.

All rights reserved. This publication contains proprietary content and is intended solely for the recipient’s personal use. Disclaimer: Our service is for informational purposes only and does not constitute personal financial advice.