Thu 29 Jan: After the Bell

Microsoft Shock Jolts Markets, but the S&P 500 Stages Late Rebound in a Volatile Session.

ℹ️ Today’s tables & charts on the ‘Market Data’ post.

Good evening,

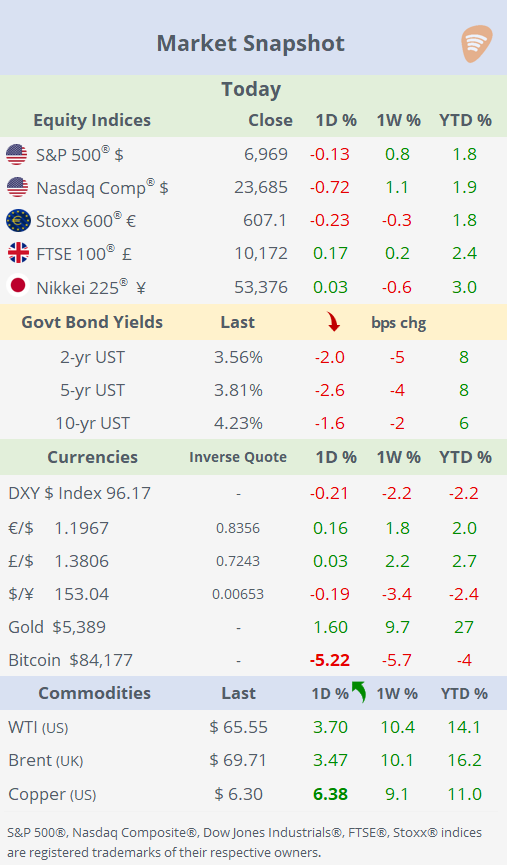

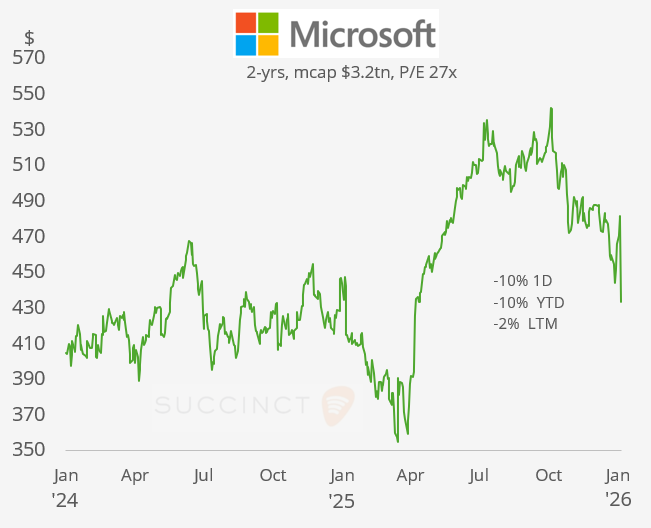

Risk assets sold off sharply in a volatile session, led by Microsoft, which slid 10% (worst day since ‘20 and erasing $400bn of value) despite beating revenue and profit expectations, as investors focused on slowing cloud momentum and surging AI-related capital spending. While Azure (cloud) revenues topped $50bn for the first time, guidance and cost intensity reignited concerns that AI monetisation may lag heavy upfront investment, with CEO Satya Nadella warning that payback will take time, dragging the broader tech complex lower, including Salesforce, ServiceNow and Workday.

Major indices fell as much as 2.5% before a strong late rebound, with the S&P 500 recovering from its intraday lows to finish almost flat, reflecting a rotation into other mega-cap names (Meta gained 10%) that held up better on earnings rather than a shift in overall sentiment.

Apple reported strong earnings after the close, posting a new all-time high EPS, citing unprecedented iPhone demand, robust figures across regions and business segments, with shares rising over 2% in extended trading. Guidance will be provided at this evening’s press conference.

The risk-off tone during the trading day spilled into crypto, with Bitcoin down 5% to ~$84k, while forex markets were largely unchanged and gold briefly surged to $5,600 before easing.

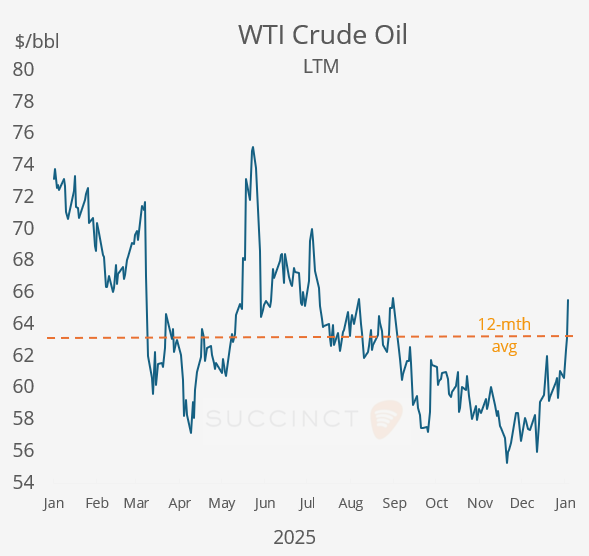

In energy markets, crude oil jumped nearly 4% to a four-month high Brent above $70, as traders rapidly repriced geopolitical risk amid escalating US-Iran tensions and fears of potential disruptions to Middle East oil supplies.

In the metals space, copper futures rallied nearly 4% today and hit fresh record highs as a surge of speculative buying, particularly from Chinese investors, helped push prices above $14,000/ton, in a metals complex rally fueled by tight supply expectations, a weak dollar and broader flight-to-hard-assets sentiment.

In emerging markets, Indonesian equities sold off sharply, with the Jakarta Composite plunging up to 10% after MSCI warned of investability issues that could trigger a downgrade from emerging to frontier market status.

In politics, Trump said a deal is close with Democrats to avert a government shutdown, with talks centring on splitting Homeland Security funding to allow further negotiations on immigration enforcement.

Earnings: → Caterpillar and Mastercard both rose 3–4% after delivering solid results and guidance, a relatively positive reaction given today’s broader market sell-off. → Germany’s software group SAP (mcap €191bn) plunged 16% after results disappointed expectations, with investors reacting negatively to a weaker outlook and concerns around cloud growth momentum and margins, triggering a sharp de-rating despite the company’s strong long-term positioning.

Economics: → US exports fell 3.6% to $292bn while imports rose 5.0% to $349bn, contributing to a sharp widening of the trade deficit to $56.8bn, the largest monthly increase in decades as higher imports outpaced weaker foreign sales. → US factory orders rebounded in November, rising 2.7% MoM, well above the 1.6% expected and reversing the prior month’s decline, with a 3.4% YoY gain, signalling improved manufacturing demand.

Business News: → In private markets, Amazon is in talks to invest up to $50bn in OpenAI at an $830bn valuation, according to the WSJ.

Corporate Deals: → Coterra Energy (mcap $22bn) and Devon Energy (mcap $26bn) are in advanced talks to merge in a near $60bn merger of equals, potentially forming the largest US shale tie-up in almost two years, with a deal possible as early as next week. The combination would strengthen their Permian Basin footprint and improve scale as shale producers face pressure from lower oil prices. Shares gained 4% and 2% respectively today.

→ Apple has agreed to acquire Israeli AI start-up Q.AI (private) for close to $2bn, marking one of its largest-ever deals as it steps up investment in AI-driven devices. The acquisition adds facial-expression and “silent speech” technology, aimed at accelerating Apple’s push into next-generation wearables and narrowing the gap with Meta, Google and OpenAI.

→ Florida-based VSE Corp (mcap $5bn), a provider of aviation aftermarket parts distribution and maintenance services, agreed to acquire private equity-owned Precision Aviation Group for ~$2bn as it accelerates the build-out of its aviation aftermarket services business.

→ In IPOs, Denver-based York Space Systems, a space and defense satellite manufacturer, priced its US IPO at $34 and raised $630mn, debuting today on the NYSE under ticker YSS at a ~$4.5bn valuation. Shares finished flat.

Day Ahead: