Thu 4 Dec: After the Bell

Quiet Session Ahead of PCE; Small Caps Hit Record High. Your 5’ evening market wrap📄📈

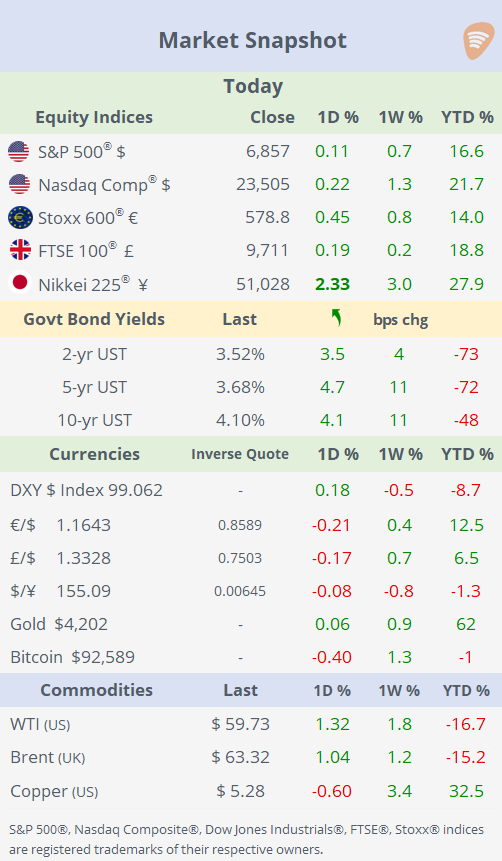

ℹ️ Today’s performance tables & charts on the ‘Market Data’ post.

Good evening,

Markets were broadly uneventful and directionless, with the Nasdaq slightly weaker and small-caps firmer as the Russell 2000 closed at an all-time high. The S&P 500 and Dow finished little changed as investors await tomorrow’s widely expected PCE inflation print — the last major data release before next week’s Fed meeting.

Intel was the notable large-cap mover, falling more than 7% on profit-taking after a multi-week rally, compounded by persistent concerns over soft server-CPU demand, competitive pressure from AMD and Nvidia in AI semiconductors, and lingering uncertainty around the company’s multi-year turnaround plan despite ongoing cost reductions. Shares remain volatile after doubling year-to-date.

In Asia, Japanese equities rallied more than 2%, driven by strong gains in robotics and technology stocks after Fanuc (mcap $32bn) announced a partnership with Nvidia to co-develop industrial robots. Fanuc jumped 13%, while Yaskawa Electric (+11.4%), Nabtesco (+11.3%), SoftBank Group (+9.2%) and other tech names posted broad strength.

Bonds weakened, with Treasury yields rising ~4bp across the curve while major currencies were little changed on the day, and the Dollar Index held steady around the 99 level.

Data: → US weekly initial jobless claims fell to 191,000 for the week ending Nov 29 — the lowest level since September 2022 and well below forecasts. The drop signals layoffs remain subdued, complicating the outlook for a rate cut by the Fed.

→ €-area retail sales rose 1.5% YoY in October, beating forecasts and improving from the prior 1.2% pace. The gain suggests that consumer spending remains resilient despite economic headwinds — a supportive sign for growth and demand outlook in the bloc.

→ Brazil’s economy grew 1.8% YoY in Q3’25, down sharply from previous quarters and registering one of the weakest YoY prints since early 2022.

Earnings: → Canadian banks TD Bank, Bank of Montreal (BMO) and CIBC all beat analyst expectations this quarter, with capital-markets businesses and interest income providing a solid boost. The outperformance lifted confidence in the Canadian banking sector, though only CIBC saw a meaningful share bump (~4%).

Deals: Thursday was a quiet day for M&A and IPOs.

→ In a rumoured deal, BP is reportedly in advanced talks to sell its lubricants unit Castrol — potentially fetching as much as $8bn from US investor Stonepeak Infrastructure Partners. The sale would form part of BP’s broader plan to raise $20bn through asset disposals.

→ In private markets, SoftBank-backed DayOne Data Centres, based in Singapore, is reportedly seeking more than $2bn in an upsized Series C round — a raise that could value the company at ~$10bn. The funding is intended to fuel DayOne’s global expansion of hyperscale data-centre infrastructure across Asia, Europe and beyond.

Day Ahead: Data → US PCE inflation, personal spending and income, Michigan Consumer Sentiment; €-zone GDP; Canada employment. Earnings → N/A

See you tomorrow.

Copyright © 2025 Succinct.

All rights reserved. This publication contains proprietary content and is intended solely for the recipient’s personal use. Disclaimer: Our service is for informational purposes only and does not constitute personal financial advice.