Thu 4 Sep: After the Bell

🎙️📄+ Market Data

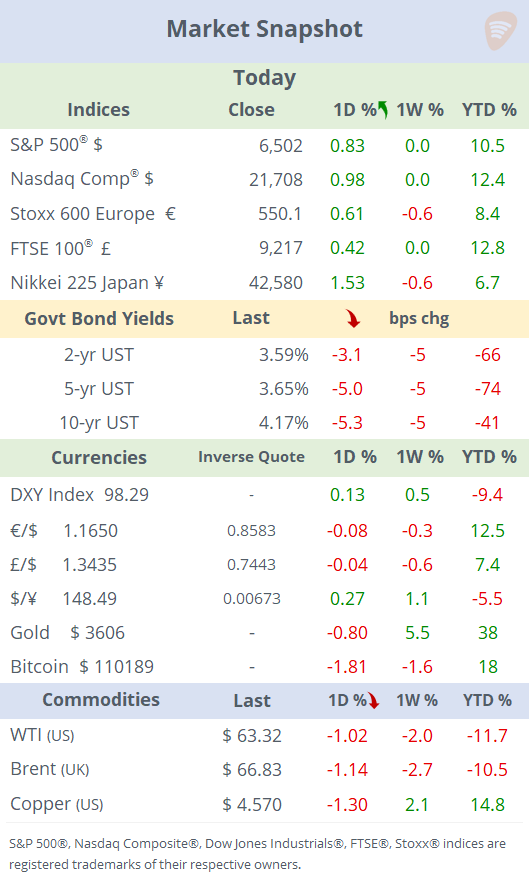

See the ‘Market Data’ post.

Good evening,

Stocks and bonds edged higher in another solid day for risk, as softer labour data and dovish remarks from Fed’s Williams reinforced expectations of upcoming rate cuts. Equities recovered to near record highs despite Trump’s warning that a Supreme Court ruling against tariffs could cause economic damage. Equity indices gained ~0.8%, 10-year Treasury yields fell another 5bp to 4.17%, the lowest close since late April, the $ closed a touch firmer, while crude oil and cryptos fell. All eyes are on tomorrow’s employment report ahead of the Fed policy meeting in two weeks.

On the tariff front, the Trump administration urged the Supreme Court to fast-track its tariff appeal, warning of economic devastation if struck down, while Treasury Secretary Bessent said the lower-court loss is already hurting trade negotiations and further delays could force unwinding $750bn–$1tn in tariffs.

Earnings: Semiconductor giant Broadcom (mcap $1.44tn) beat top and bottom estimates after the close with shares little changed in after-hours trading. Lululemon (mcap $24bn) plunged 13% in extended trading after gaining 4% during the regular session as it disappointed with its outlook by slashing full-year revenue and profit forecasts. The stock is down 46% this year.

Data: The U.S. labour market showed signs of cooling today, with ADP reporting a modest 54k private-sector jobs added in August, below expectations and down from July's revised 106k. Also, weekly initial jobless claims rose to 237k, above forecasts and the highest in 15 weeks, indicating potential softening in employment conditions. These data increased the odds of a 25bp Fed rate cut this month to 98%. Finally, the ISM Services PMI for August rose to 52, surprising analysts, indicating a return to modest expansion in the services sector.

Central Banks: New York Fed President Williams described the current central bank policy as ‘modestly restrictive’ but said gradual rate cuts could become appropriate. He expects real GDP growth of 1.25–1.5% and inflation of 3–3.25% for 2025. Also, the Justice Department opened a criminal investigation into Fed Governor Lisa Cook, whom Trump is trying to remove based on allegations of mortgage fraud, and he appointed his ally Stephen Miran to be confirmed as a new Fed official.

Corporate Deals: Goldman Sachs (mcap $224bn) has announced a strategic partnership with asset manager T. Rowe Price (mcap $24bn), involving a $1bn investment to acquire a 3.5% stake. T. Rowe shares jumped >5% but are flat YTD.

In private markets, four-year-old San Francisco-based A.I. start-up Anthropic raised $13bn at a $170bn valuation to compete with OpenAI. Investors include Iconiq Capital and Lightspeed Ventures. Also, Rithm Capital, one of the US’s biggest mortgage servicers, acquired the $17bn private credit manager Crestline Management to become a broad-based asset manager.

Private capital group Carlyle raised $20bn via its AlpInvest unit to acquire secondary private equity stakes from real money investors as private equity funds struggle to exit investments.

IPOs: Advent International is preparing for a potential U.S. listing of Innio, the Austrian power equipment manufacturer, targeting a valuation of $12bn. Transit tech firm Via Transportation targets a $3.5bn valuation to raise $460mn on the NYSE (guidance $40-44).

See you tomorrow.

Copyright © 2025 Succinct.

All rights reserved. This publication contains proprietary content and is intended solely for the recipient's personal use. Disclaimer: Our service is for informational purposes only and does not constitute personal financial advice.