Thu 5 Feb: After the Bell

AI-Led Selloff Deepens as Risk Appetite Fades: What you need to know

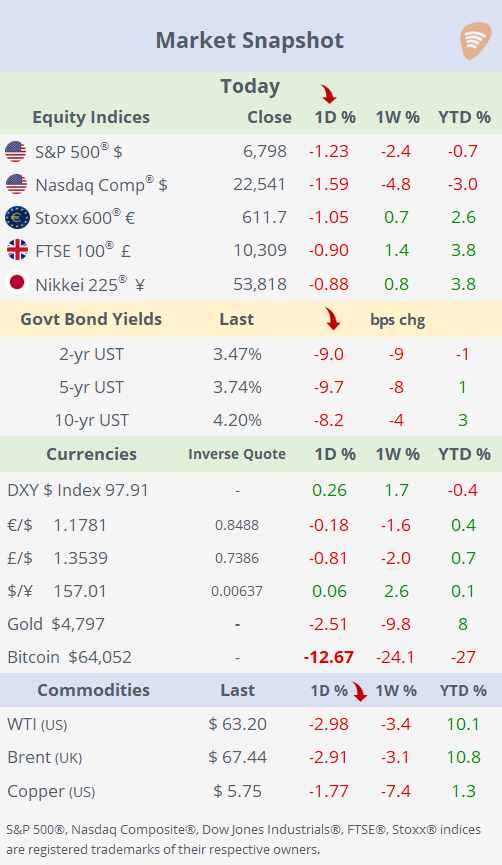

ℹ️Find more performance tables here.

Feel free to email us with ideas & feedback: usmarketsdaily@succinct.info

Risk-off sentiment deepened across markets, led by another sharp unwind in AI and software stocks. Mega-caps such as Microsoft, Amazon and Oracle fell between 4% and 7%, pushing the Nasdaq Composite down 1.6% on the day and roughly 5% over the past week, marking a third consecutive session of heavy losses. Markets remain hypersensitive to anything that challenges the AI capex narrative and stretched software valuations, with today’s catalyst coming from softer-than-expected US labour data, including higher jobless claims and weaker job openings.

Earnings added fuel to the sell-off after the close, as Amazon shares gapped lower by as much as 11% following a mixed quarterly report and the announcement of AI capital spending set to surge to $200bn, far above expectations, compounding the stock’s 4% decline during regular trading.

The risk aversion spilt into other asset classes: silver plunged 14% after days of extreme volatility, gold fell 4%, and crypto markets saw renewed deleveraging, with Bitcoin sliding 13% to around $64k, a 15-month low and roughly 50% below its October peak. Safe-haven demand drove Treasuries higher, pulling the 10-year yield down 8bp to 4.20% as the curve bull-flattened, while the dollar extended its rebound from late-January lows.

The session also featured a busy central bank calendar, with the ECB, Bank of England and Banxico all holding policy meetings, alongside several notable IPO debuts.

Earnings: → Releases across the US and Europe (Shell, Unilever, BNP, BBVA, Linde and ConocoPhillips) were met with mostly weaker share price reactions, reflecting cautious guidance and elevated expectations. BBVA stood out on the downside, plunging ~9% in Madrid, despite reporting strong headline profits, as investors focused on higher loan-loss provisions, a softer capital ratio trajectory and conservative 2026 guidance, which disappointed hopes for continued capital upside and distributions. Overall, the sell-off highlights a market that is increasingly unforgiving toward banks and cyclicals, where forward visibility and capital strength fall short of expectations.

Monetary Policy: → The ECB kept policy unchanged, holding the deposit rate at 2% and the main refinancing rate at 2.15%, in line with expectations as growth proved more resilient than forecast. Policymakers reinforced a patient, data-dependent stance, with Lagarde saying inflation is “in a good place” after headline inflation fell to 1.7% and core to 2.2%, supporting the view that price pressures should stabilise around the target.

→ The Bank of England held the Bank Rate at 3.75%, but a narrow 5–4 vote and dovish communication signalled that a rate cut as early as March is increasingly likely, with markets lifting the implied probability to around 50%. Policymakers emphasised improving inflation dynamics, expecting CPI to return to the 2% target from April, while weaker growth and a softening labour market were cited as creating scope for further easing, albeit cautiously and data-dependent.

→ Mexico’s central bank, Banxico, kept its policy rate unchanged at 7%, in line with expectations, as policymakers opted for caution amid still-elevated underlying inflation risks. The central bank reiterated a data-dependent bias, signalling that further easing will require clearer confirmation that disinflation is firmly entrenched and consistent with convergence toward the 3% target.

Economics: → US weekly initial jobless claims unexpectedly rose to 231k, above forecasts and the highest in two months, signalling some softening in labour market resilience amid rising layoffs and weather disruptions. Meanwhile, JOLTS job openings came in at 6.54mn, well below expectations and the lowest in over five years, pointing to weaker labour demand and adding to evidence of cooling hiring momentum.

Together, these softer figures reinforce a narrative of a mildly deteriorating job market that could weigh on sentiment and support a more cautious Fed outlook.

→ €-zone retail sales fell 0.5% MoM in December, worse than expected and the first notable contraction in months, signalling a meaningful softening in consumer spending. Annual growth at +1.3% YoY also undershot forecasts, pointing to slowing household demand that could add to concerns about uneven growth momentum and weigh modestly on the ECB’s inflation outlook.

→ Germany’s factory orders jumped 7.8% MoM, the strongest gain since late 2023, signalling a notable uptick in industrial demand and potential momentum for manufacturing activity.

Corporate Deals: → Rio Tinto and Glencore abandoned merger talks that would have created the world’s largest mining group, valued at over $200bn, underscoring the complexity and risk of megadeals despite a boom in sector M&A. Shares fell on the news, with Glencore down 7% and Rio Tinto off 5%, even as mining deal activity hit a 13-year high in 2025, driven by copper expansion.

→ In IPOs, Minnesota-based power equipment maker Forgent Power Solutions priced its IPO at $27 per share and began trading on the NYSE today under the ticker FPS. It raised $1.5bn, at a market valuation of ~$8.2bn. Shares gained 9% on their debut.

→ California-based Eikon Therapeutics, a late-stage biopharmaceutical company focused on developing cancer therapies, raised $381mn in its upsized IPO at $18 apiece on the Nasdaq under the ticker EIKN, at an implied valuation near $860mn at pricing. Shares fell sharply on their debut (-17%).

→ Finally, Bob’s Discount Furniture (BOBS) also did its IPO today on the NYSE, pricing at $17 and raising about $331mn. At the offer price, the Connecticut-based home furnishings retailer was valued at $2.2bn heading into its debut. Shares closed flat.

Day Ahead:

Monetary Policy → India (unch at 5.25% exp). Data → US Michigan consumer confidence, no NFP data tomorrow; Canada employment report; Germany industrial production. Earnings → Philip Morris, SocGen, Ubiquity N.

See you tomorrow.

Copyright © 2025 Succinct.

All rights reserved. This publication contains proprietary content and is intended solely for the recipient’s personal use. Disclaimer: Our service is for informational purposes only and does not constitute personal financial advice.