Thu 5 Mar: After the Bell

Markets Slide as Middle East War Escalates and Oil Surges

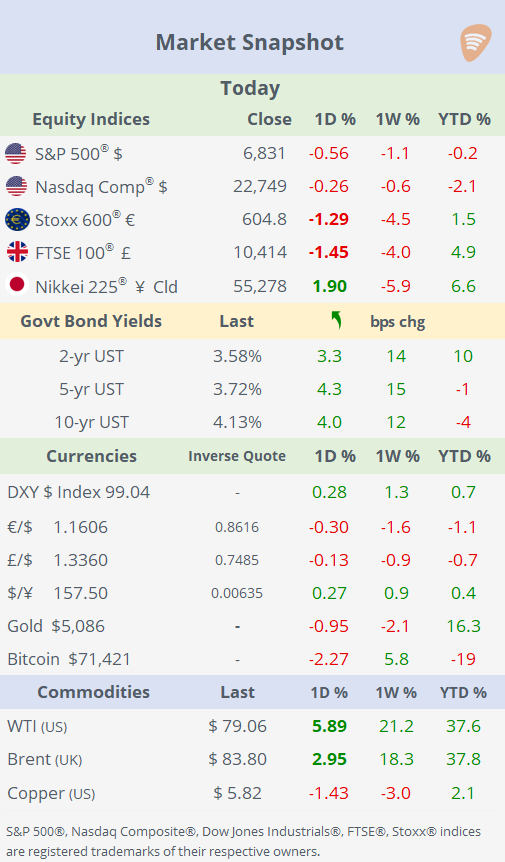

ℹ️Today’s Performance tables.

Good evening,

Risk assets continued to trade in volatile conditions amid intensifying geopolitical tensions. Stocks fell across the US and Europe, with the S&P 500 down about 1.4% at one point before trimming losses to close roughly 0.5% lower, while the Russell 2000 underperformed with a 2% decline. Benchmark bond yields moved higher, with the 2-year Treasury yield reaching a five-week high as rising oil prices and inflation concerns outweighed the usual safe-haven bid.

The market backdrop was dominated by a sharp escalation in the Middle East: Israel and Iran exchanged further attacks, Washington closed its embassy in Kuwait and urged citizens to leave, and thousands fled Beirut following a sweeping Israeli evacuation order.

The conflict also spread regionally, with Azerbaijan warning of retaliation after strikes reached its territory and Saudi Arabia intercepting missiles and drones, while Russia’s Vladimir Putin condemned the attacks but stressed the conflict was “not our war,” positioning Moscow as a potential mediator.

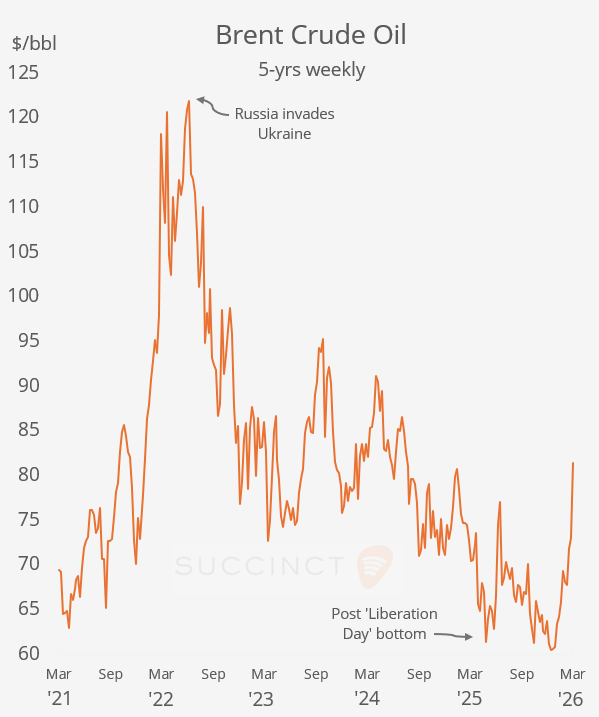

Oil prices surged, as crude hit its highest level since 2024, and front-month Brent Crude rose about 3% to $84.80, as the de facto closure of the Strait of Hormuz trapped thousands of ships and disrupted flows of roughly a fifth of the world’s oil and LNG consumption. Brent’s year-end futures trade at $71. Europe’s natural gas benchmark, the Dutch TTF contract, gained 4% to €50.7 from €32 a week ago.

Meanwhile, semiconductor stocks swung sharply after reports that the Trump administration is drafting new regulations requiring approval for AI chip exports worldwide, adding another layer of uncertainty to an already fragile market environment.

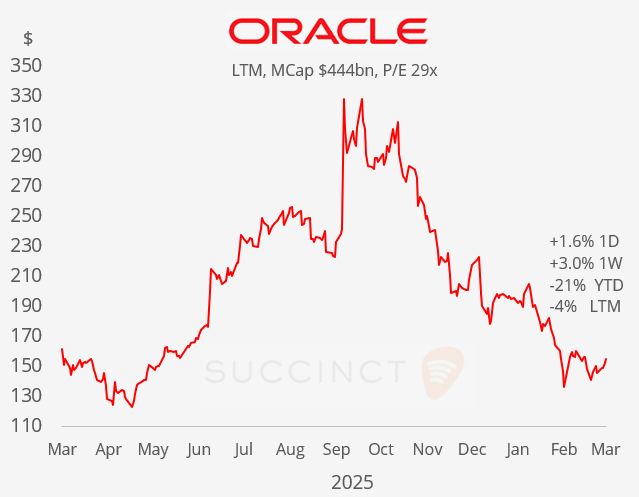

Business News: → Oracle (mcap $444bn) plans to cut thousands of jobs as it faces a cash crunch from a massive AI-focused data centre expansion. The cuts, affecting multiple divisions, reflect reduced needs in some roles and follow a broader hiring slowdown while Oracle invests heavily in cloud AI infrastructure. Shares are 21% lower YTD.

Economics: → US initial jobless claims held steady at 213k, in line with expectations and little changed from the prior week; a non-event pointing to continued stability in the labour market.

→ €-zone retail sales fell 0.1% MoM in January but rose 2.0% YoY, suggesting short-term consumer demand softened at the start of the year while the broader spending trend remains modestly positive.

Corporate Deals: Today saw very little activity in corporate deals or IPOs, with no new listings or major M&A transactions announced, a quiet day for deal flow.

Day Ahead:

Data → US non-farm payrolls (+59k exp) and retail sales; €-zone GDP estimate.

Earnings → No significant releases.

See you tomorrow.

Copyright © 2026 Succinct.

All rights reserved. This publication contains proprietary content and is intended solely for the recipient’s personal use. Disclaimer: Our service is for informational purposes only and does not constitute personal financial advice.