Thu 7 May: After the Bell

Stocks Slip Ahead of Jobs Data as Iran Deal Hopes Fade

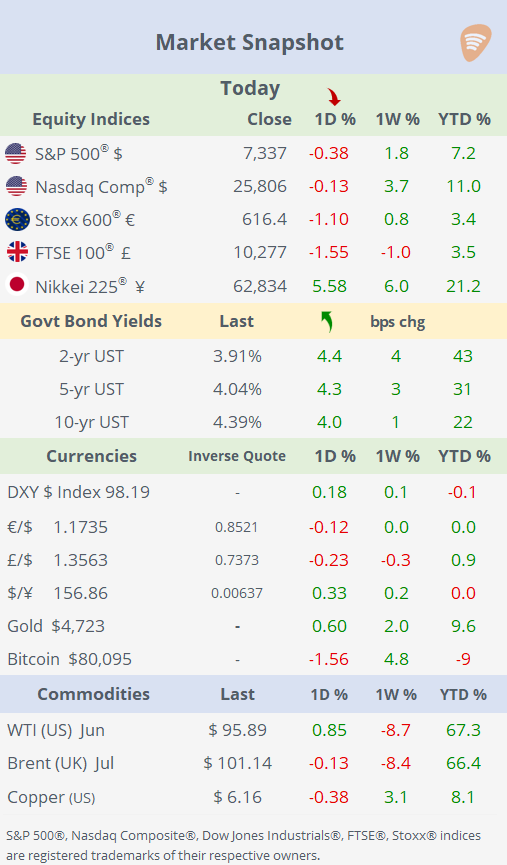

📈 Today’s performance tables.

Good evening,

Geopolitics remained the key driver of sentiment on Thursday as doubts over an imminent US-Iran deal, alongside renewed Israeli strikes in Lebanon, kept investors cautious. US equities closed lower, with small- and mid-cap stocks leading declines, while European markets also ended notably weaker ahead of Friday’s US jobs report.

Elsewhere, markets were relatively calm: currencies, bond yields and crude oil saw limited moves, while cocoa was the standout commodity mover, plunging ~7% as improving harvest prospects in the Ivory Coast, Ghana and Brazil eased supply concerns. Separately, the IMF warned that advanced AI models could pose systemic financial risks through potential “correlated failures” and cyber shocks.

Korea’s Samsung Electronics surpassed a $1tn market value, becoming only the second East Asian company after Taiwan’s TSMC to reach the milestone, as investors continue piling into AI-linked semiconductor stocks. Shares jumped 14% to a record high, while SK Hynix gained over 10%, fueled by surging demand for high-bandwidth memory chips used in AI infrastructure.

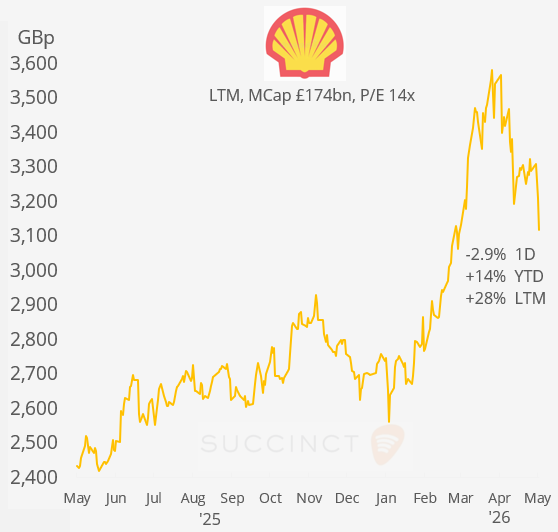

Earnings: → Shell Plc (mcap £174bn) posted $6.9bn in adjusted earnings and $17.2bn in operating cash flow in Q1, with CEO Sawan citing “unprecedented disruption in global energy markets.” The oil major also announced another $3bn share buyback, underscoring resilient cash generation despite volatile commodity prices. Shares fell 3% today but remain 14% higher YTD.

Economics: → Germany’s factory orders rose 5.0% MoM in March, well above expectations and rebounding sharply from the prior month, signalling improved momentum in the country’s industrial sector. The upside surprise may ease concerns over manufacturing weakness, though broader sentiment remains cautious given soft European growth and trade uncertainty.

→ €-zone retail sales fell 0.1% MoM in March, slightly better than forecasts but marking a third consecutive monthly decline, pointing to continued weakness in consumer demand. The data reinforces concerns that household spending remains soft despite easing inflation and lower interest rates across Europe.

Monetary Policy: → Banco de México cut its benchmark rate by 25bp to 6.50%, in line with expectations and the lowest level in four years, extending its easing cycle despite persistent inflation pressures. Policymakers said the balance of inflation risks remains skewed to the upside, signalling a cautious path for future rate cuts.

Deals: → In the biotech sector, Catalyst Pharmaceuticals (mcap $3.8bn), a rare disease drugmaker, agreed to be acquired by privately held Angelini Pharma in a $4.1bn all-cash deal. Angelini will pay $31.50/share, a 21% premium and an all-time high for Catalyst, to expand its rare-disease platform by combining Catalyst’s commercial portfolio with its own neuroscience expertise.

→ Roche Holding (mcap $328bn) agreed to acquire US-based PathAI (private) for up to $1.05bn, expanding its diagnostics business with AI-powered pathology tools. The deal builds on a partnership launched in 2021 and aims to improve lab efficiency while accelerating drug discovery and clinical development.

→ In IPO’s, Suja Life, an Oceanside, California-based maker of organic juices, wellness shots and functional sodas, fell 14% in its Nasdaq debut after pricing its IPO at $21 per share, the low end of its marketed range, raising $187mn. The weak debut valued the company at roughly $700mn, highlighting continued investor selectivity toward consumer IPOs despite a reopening issuance market.

→ HawkEye 360, a Virginia-based space intelligence company, was priced at $26 (top of its range), raising $416mn, initially valuing the company at $2.5bn. Shares then jumped about 30% in their NYSE debut, pushing its market value closer to $3.2bn. HawkEye operates a constellation of 30+ satellites that track radio-frequency emissions globally for US defence and intelligence agencies, another sign that defence/space-tech IPOs remain one of the hottest pockets of the market right now.

Day Ahead:

Data → US non-farm payrolls, unemployment rate, avg earnings; Germany trade; Spain industrial production.

Earnings → Intesa Sanpaolo (Italy), Commerzbank (Germany), Ubiquiti Networks (US).

Copyright © 2026 Succinct.

All rights reserved. This publication contains proprietary content and is intended solely for the recipient’s personal use. Disclaimer: Our service is for informational purposes only and does not constitute personal financial advice.