Thu 9 Apr: After the Bell

Markets Whipsaw as Ceasefire Holds, For Now …

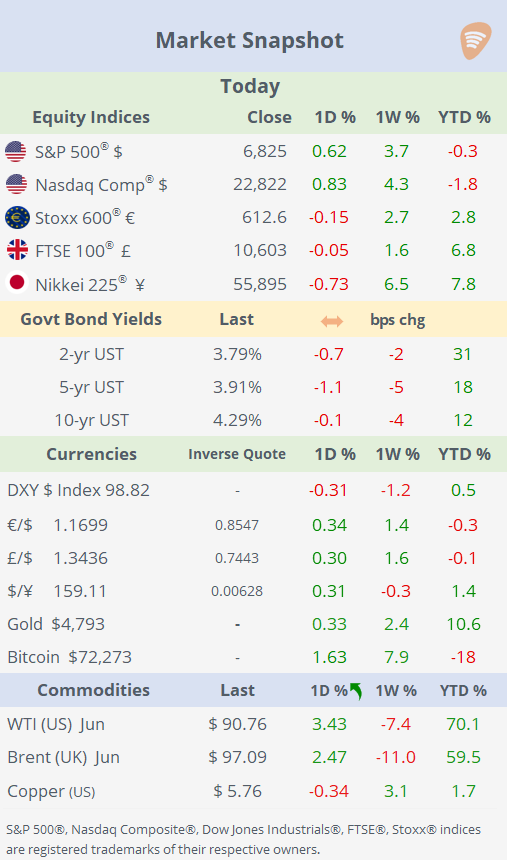

📈 Today’s performance tables.

Evening,

Markets remain highly volatile as investors grapple with the fragility of the US–Iran ceasefire, with renewed tensions spilling into Lebanon. Despite the agreement brokered by Trump, Israel continued airstrikes, with Prime Minister Netanyahu making clear the deal does not extend to Lebanon. The situation remains fluid, with both Washington and Tehran accusing each other of breaches, while the reopening of the Strait of Hormuz remains unresolved.

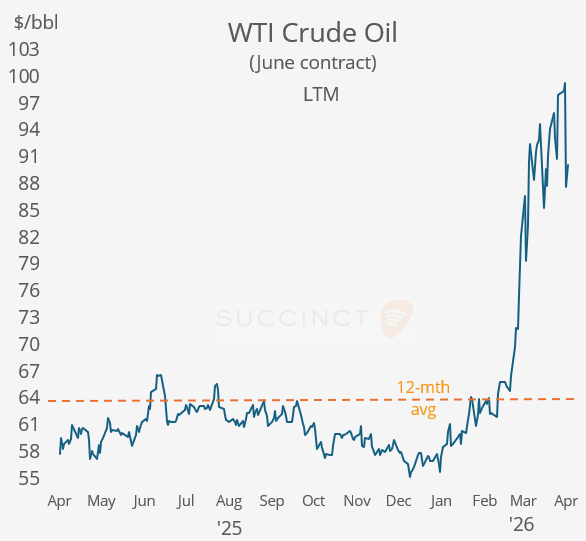

Oil markets continue to reflect this uncertainty, with WTI (May) briefly moving back above $100 before easing into the close, as headlines oscillated between escalation risks and tentative diplomatic progress. Ongoing disruptions to tanker traffic through Hormuz and the prospect of prolonged regional instability are keeping energy markets highly reactive to every development.

Equity markets, however, staged a notable rebound. After early weakness and declines across Europe and Asia, US indices recovered into the close, supported by hopes that negotiations between Israel and Lebanon could help contain broader escalation. Optimism was further reinforced by Trump’s comments expressing confidence in a potential peace deal, alongside US efforts to pressure Israel to scale back strikes.

On the economics front, the latest US Personal Consumption Expenditures confirmed that inflation remains elevated, though the data offers limited insight into the potential impact of the ongoing conflict on price dynamics.

→ Notable mega-cap mover: Amazon shares jumped 5.6% after CEO Andy Jassy’s shareholder letter reassured investors on aggressive AI investment, highlighting strong growth in AWS AI revenues (~$15bn run-rate) and future upside from its chip business. The move also reflects renewed confidence in Amazon’s positioning in the AI race, with investors increasingly viewing AWS as a key long-term beneficiary of surging enterprise demand for compute and AI infrastructure.

Economics: → US PCE inflation, the Fed’s preferred inflation indicator, showed headline PCE (February print) at +0.4% MoM and +2.8% YoY, with core at +0.4% MoM and ~3.0% YoY, broadly in line with expectations and unchanged from January’s pace. While not a surprise, the data highlights sticky underlying inflation, with core running at 3% for a third straight month, reinforcing a “higher for longer” Fed stance amid still-elevated price pressures.

→ Mexico’s CPI rose 4.59% YoY in March, accelerating from ~4.0% previously and marking the highest level since late 2024, driven largely by energy and food prices. The pickup keeps inflation above the central bank’s target range, complicating the easing cycle and reinforcing a more cautious policy outlook amid rising geopolitical-driven price pressures.

Deals: → Louisiana-based privately held Sazerac is exploring a potential deal for Brown-Forman Corp (mcap $14bn), a family-controlled alcohol beverages company, emerging as a rival bidder alongside France’s Pernod Ricard. The situation points to potential multi-bidder consolidation in global spirits, as incumbents pursue scale amid slowing demand and shifting consumption trends, with Brown-Forman viewed as a scarce, high-quality asset. Brown-Forman shares gained 14% today but remains 10% in the LTM.

→ Alternative investment manager Ares Management will acquire Whitestone REIT (mcap $985mn, P/E 20x) in an all-cash $1.7bn deal, offering $19/share (~12% premium), with closing expected in Q3. The transaction highlights continued private capital interest in public real estate, with Ares targeting income-generating assets amid dislocated REIT valuations. Whitestone REIT develops and manages open-air retail centres located in some of the fastest-growing markets in the country: Phoenix, Austin, Dallas-Fort Worth, Houston and San Antonio. Shares advanced 12% today.

→ Cloud infrastructure technology company CoreWeave (mcap $49bn) and Meta Platforms signed a $21bn long-term agreement for AI cloud infrastructure, with CoreWeave supplying high-performance computing capacity (GPU-based data centres) through 2032 to power Meta’s AI models and inference workloads. The deal, on top of a prior $14bn contract, reflects the massive scale of AI infrastructure spending, as Big Tech races to secure scarce compute capacity, positioning “neocloud” providers like CoreWeave as critical enablers in the AI arms race.

→ In IPOs, Swiss-based Terra Quantum, which develops quantum algorithms, software, and security solutions used across industries such as defence, finance, and pharma, plans to go public via a SPAC merger with Nasdaq-listed Mountain Lake Acquisition Corp II at a $3.25bn valuation. The deal highlights continued investor appetite for next-generation computing/AI-adjacent technologies, with proceeds aimed at scaling IP-driven, recurring-revenue models and accelerating product development and M&A.

→ In SPAC deals, Suncrete (symbol RMIX), a US ready-mix concrete logistics and distribution platform, went public via a SPAC merger with Haymaker Acquisition Corp. IV, in a $226m deal implying a $970m enterprise value and $700–800m of market cap. RMIX shares rose 18% above their opening trade this morning.

Day Ahead:

Data → US CPI, factory orders, Michigan consumer sentiment; Russia, Brazil inflation.

Earnings → none of relevance.

Copyright © 2026 Succinct.

All rights reserved. This publication contains proprietary content and is intended solely for the recipient’s personal use. Disclaimer: Our service is for informational purposes only and does not constitute personal financial advice.