Tue 10 Feb: After the Bell

Markets Turn Cautious on Weak Consumer Signal, Bonds Rise ➡️

ℹ️Find more performance tables here.

Good evening,

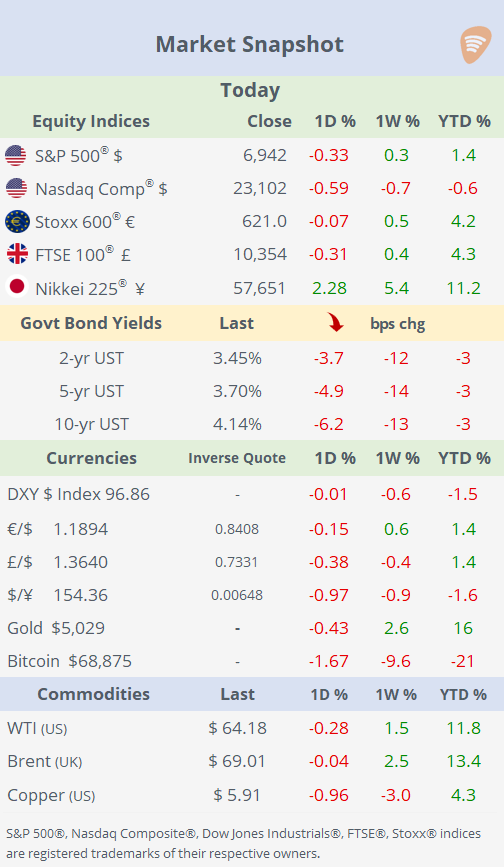

US equity indices were mostly lower, with the S&P 500 and Nasdaq retreating while the Dow Jones Industrial Average managed only a marginal gain, as investors digested a softer-than-expected December retail sales print. The data reinforced concerns about cooling consumer momentum, weighing on risk appetite and cyclicals, particularly after last week’s volatility and ahead of key labour data tomorrow and inflation on Friday.

In forex, the DXY $ index was unchanged, showing little directional conviction, though it continued to weaken against the yen as markets digest the implications of Japan’s general election. Crypto assets remained under pressure, failing to sustain a rebound as Bitcoin struggled amid tighter liquidity conditions and fading speculative momentum.

Today’s drop in Treasury yields reflected renewed demand for bonds, as investors sought safety amid softer economic signals, particularly the weak retail sales print. Long-end Treasury yields fell over 7bp with the 30-yr at 4.78%, accumulating a 12bp drop in the past week. Market pricing now reflects a 20% probability of a 25bp Fed rate cut to the 3.25–3.50% range at the mid-March meeting, up from around 9% a week ago, signalling a modest but notable shift toward a more dovish outlook.

After the bell, online broker Robinhood Markets (mcap $77bn) reported strong revenue growth with a 27% surge to $1.28bn and record trading revenue. However, the stock sank ~7% after hours as the dollar-denominated top line still missed some metrics and raised questions about sustainability amid crypto weakness and trading volatility.

Earnings: → S&P Global (-10%): Slumped on earnings that, while solid, came with softer guidance and cautious commentary on data & analytics demand, prompting investor profit-taking and concerns about near-term outlook.

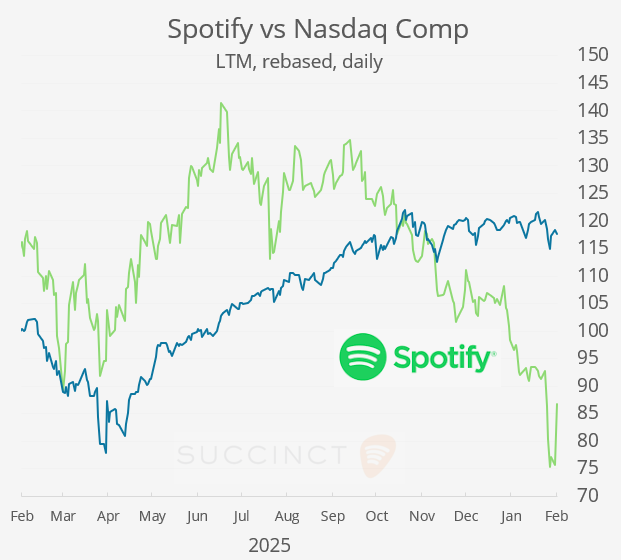

→ Spotify (+15%): Jumped sharply as the company beat subscriber and revenue expectations, highlighted strong podcasting growth and improved ad monetisation, which helped ease investor concerns over its long-term profitability path.

→ Ferrari (+9%): Rallied after reporting better-than-expected deliveries and margin expansion, reassuring investors on high-end demand and pricing power.

Other reporters with modest stock reactions included Coca-Cola, AstraZeneca and Barclays, where results were largely in line with expectations.

Economics: → US retail sales were flat in December, coming in at $735bn and missing expectations for a ~0.4% rise, signalling a soft end to holiday season spending and potential consumer fatigue as the economy heads into 2026.

→ France’s unemployment rate rose to 7.9% in Q4’25, above expectations and the highest level since Q3’21, reflecting a moderate softening in the labour market.

Corporate Deals:

→ Mubadala Capital, the alternative investment arm of Abu Dhabi’s sovereign wealth fund, together with TWG Global, agreed to acquire Clear Channel Outdoor Holdings (mcap $1.12bn), the US-based out-of-home advertising group, in a $6.2bn enterprise value deal, at a 71% premium to the indisturbed price and underscoring sovereign capital’s appetite for infrastructure-like media assets with growing digital exposure. Clean Channel rose 8% today to a three-year high.

→ Dutch ingredients supplier DSM-Firmenich (mcap €18bn) agreed to sell a majority stake in its animal nutrition and health business to CVC Capital Partners, in a €2.2bn deal, retaining 20% stakes in two carved-out entities as it completes its strategic pivot to human nutrition, health and beauty, alongside a planned €500mn share buyback. DSM shares gained 5.5% today.

→ UK bank NatWest (mcap £48bn) agreed to acquire Evelyn Partners, a UK-based wealth and asset manager, for £2.7bn incl. debt from Permira and Warburg Pincus advised funds, combining it with its private banking arm to lift fee income by ~20%, grow AUM to £127bn, and deliver £100mn in annual cost synergies.

→ In private markets, MGX, an Abu Dhabi-based AI investment firm established by the government and backed by Mubadala and G42, is nearing a commitment of hundreds of millions of dollars into Anthropic’s ongoing $20bn fundraise, underscoring sovereign capital’s growing role in funding major AI startups.

Day Ahead:

Data → US non-farm payrolls (Jan) +70k exp, unemployment rate; Japan PPI. Earnings → Cisco, McDonald’s, T-Mobile, Shopify, TotalEnergies, AppLovin, Heineken.

See you tomorrow.

Copyright © 2026 Succinct.

All rights reserved. This publication contains proprietary content and is intended solely for the recipient’s personal use. Disclaimer: Our service is for informational purposes only and does not constitute personal financial advice.