Tue 10 Mar: After the Bell

Stocks Pause as Oil Volatility Dominates - what you need to know

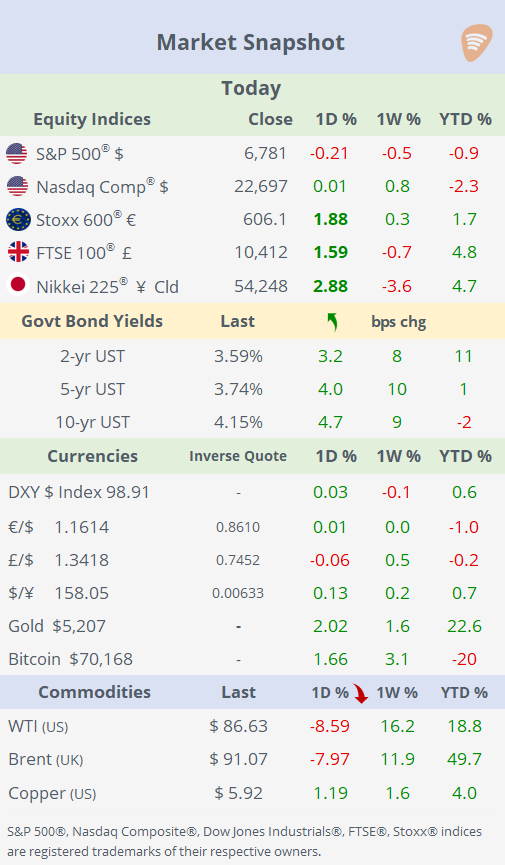

ℹ️Today’s Performance tables.

Good evening,

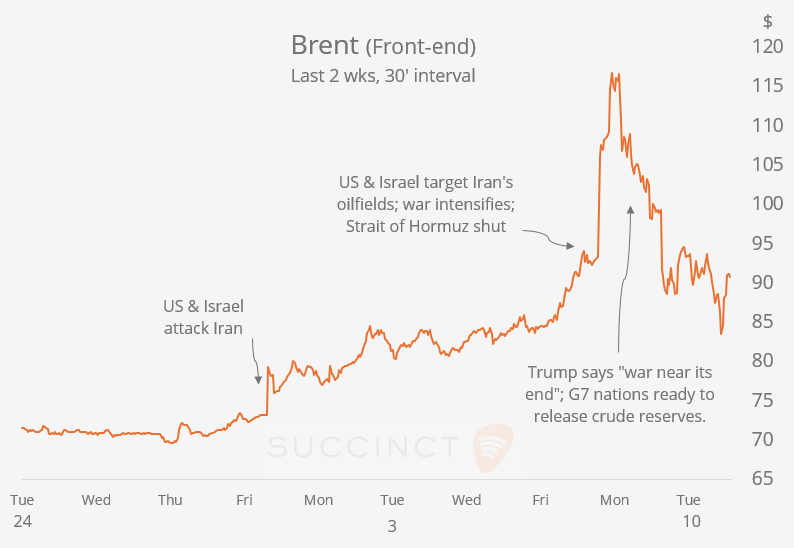

Global markets were relatively subdued on Tuesday: Equities on Wall Street finished little changed, with most sectors marginally lower and energy underperforming, while European stocks rallied, following the recovery seen in US markets yesterday. The main focus remained on oil markets, which experienced another volatile session as prices corrected sharply amid easing geopolitical fears and speculation that major economies could release strategic petroleum reserves.

At the same time, headlines from the Middle East remained mixed and at times contradictory. Saudi Aramco (mcap $1.7tn) warned of “catastrophic consequences” if the Iran conflict drags on, though the company said it could still export roughly 70% of its normal ~7mn barrels per day within days if disruptions occur. Traders also struggled to interpret conflicting signals around the Strait of Hormuz, while reports of a drone attack on the Ruwais Industrial Complex in Abu Dhabi highlighted that risks to regional energy infrastructure remain elevated.

Elsewhere, currency markets were quiet, Treasury yields moved modestly higher, while gold jumped around 2% to about $5,207, and Bitcoin hovered near $70,000.

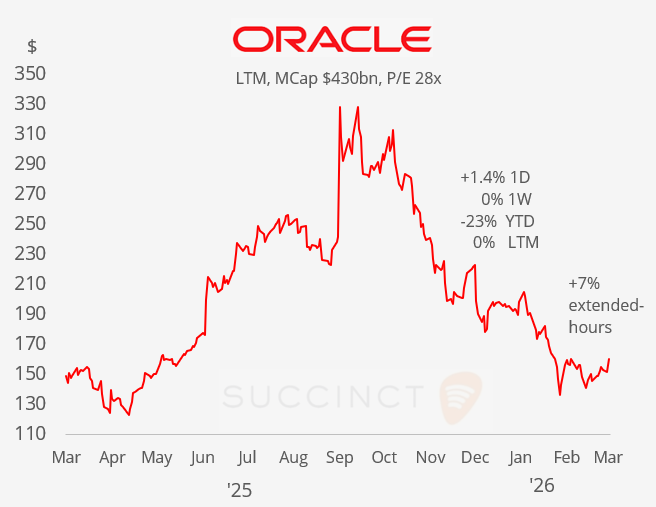

Earnings: → After the close, Oracle (mcap $430bn) beat Q3 expectations with EPS of $1.79 on $17.19bn in revenue (vs. $1.70 and $16.9bn expected), driven by stronger-than-forecast cloud infrastructure sales. The company also raised its 2027 revenue outlook to $90bn, sending the stock ~7% higher in after-hours trading as investors focused on accelerating cloud growth and heavy AI-related capex. Shares are 23% lower YTD and flat in the LTM.

Economics: → It was light data ahead of tomorrow’s US CPI update. US private payrolls (ADP) averaged +15,500/wk through Feb 21 (third straight acceleration, fastest since Nov), signalling resilient hiring momentum amid sector concentration in construction, education and health.

Corporate Deals: Tuesday was a quiet day in M&A.

→ In private markets, CVC Capital Partners’ Global Sport Group was valued at about €7bn in a financing deal after failing to sell equity at a €9bn target valuation. Instead of selling a stake, ~€3bn of capital will be injected, primarily in the form of debt and preferred equity, from KKR (via Global Atlantic) and PIMCO to fund the sports investment platform.

→ Atlas Energy Group (mcap $1.5bn) signed a $840mn deal with Caterpillar (mcap $337bn) for power-generation equipment through 2029, locking in capacity amid surging US electricity demand from AI/crypto data centres and electrification trends.

→ In IPOs, Orlando-based digital streaming aggregator and media technology provider FreeCast (CAST) listed on Nasdaq today via direct listing. It placed ~20mn shares that began trading at $33 but dropped sharply to close at $9.14, for a market value of $375mn.

→ In credit markets, Amazon (mcap $2.3tn) is leading a record US corporate bond issuance day, marketing up to ~$30bn in USD bonds plus €10bn in euros, with demand already exceeding $123bn as it funds large AI infrastructure investments. The deal is part of a broader issuance wave expected to reach $60bn in one day, with companies rushing to tap calmer markets after geopolitical tensions eased. Amazon’s senior unsecured 2034 bond, rated at AA/A1, is trading at a 4.33% yield or a Z-spread of 50bp.

Day Ahead:

Data → US CPI inflation (2.4% YoY exp); Germany inflation (final Feb). Earnings → Inditex (Zara), Foxconn, Porsche.

See you tomorrow.

Copyright © 2026 Succinct.

All rights reserved. This publication contains proprietary content and is intended solely for the recipient’s personal use. Disclaimer: Our service is for informational purposes only and does not constitute personal financial advice.