Tue 14 Apr: After the Bell

Risk-On Revival: Nasdaq Near Record as Oil Slides

📈 Today’s performance tables.

Good evening,

Tuesday delivered a strong risk-on session, with equities surging and oil retreating sharply as investors grew more confident that the fragile US–Iran ceasefire can be extended beyond next week. Optimism increased after Trump signalled openness to further talks, while reports said Tehran may pause shipments through the Strait of Hormuz to facilitate new negotiations. Meanwhile, the US said no ships passed the Iranian blockade in its first 24 hours, with more than 10,000 personnel, a dozen warships and aircraft involved in the operation.

Wall Street rallied toward record territory, with the Nasdaq rising for a 10th straight day and sitting just 1.5% below its all-time high. The Magnificent-7 ETF jumped 3%, led by gains of nearly 4% in Nvidia, Amazon and Tesla, underscoring renewed appetite for growth and AI-linked names.

Macro data also helped sentiment, as March PPI rose more slowly than expected, easing some inflation concerns despite the recent energy shock. In rates and FX, the DXY $ Index fell to a six-week low, the 10-year Treasury yield touched a four-week low, while gold rose again and is now up 10% over the past 12 sessions, highlighting a broader reversal of the defensive trends that had dominated since the conflict began.

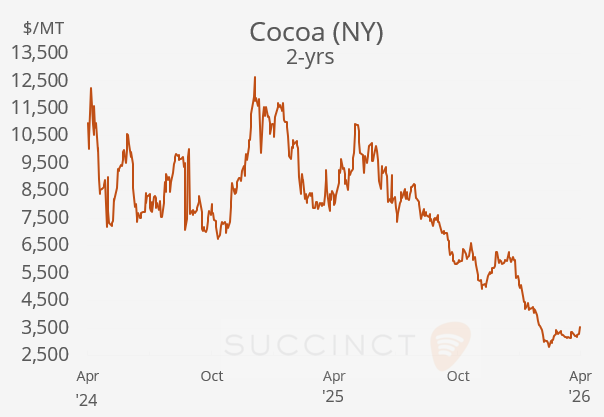

Another notable mover in commodities today was cocoa. Prices jumped 8%, driven primarily by the drop in the $, which lowers the effective cost of dollar-priced cocoa for overseas buyers and tends to boost commodity demand. The weaker $ also triggered aggressive short-covering, as funds were heavily bearish on cocoa, turning today’s move into more of a technical squeeze than a fresh supply-driven rally.

The IMF cut this year’s global growth forecast to 3.1% from 3.3% while raising inflation estimates, warning that the Iran war and energy shock have abruptly darkened the outlook. The scenario is stagflationary and risk-negative, especially if oil disruptions persist. It projects US CPI inflation at 3.0% in 2026, up from its prior estimate of 2.5%, reflecting the recent energy shock and firmer price pressures.

Central Banks: → The main inflation and rates takeaway today from Fed speeches came from Chicago Fed President Goolsbee, who said rate cuts could be delayed until 2027 if elevated oil prices from the Iran conflict keep inflation from returning to the Fed’s 2% target. That was interpreted as a hawkish higher-for-longer signal.

→ ECB’s Lagarde said policymakers have not yet decided whether rates need to rise, adding it is still too early to assess the inflation impact of the Iran war. The message was cautious and data-dependent, suggesting the ECB is monitoring the energy shock closely but is not ready to signal imminent tightening.

Both the Fed and the ECB will hold policy meetings at the end of April.

Economics: → US PPI or wholesale inflation rose 0.5% MoM in March and 4.0% YoY (below estimates), accelerating from 3.3% in February and marking the highest annual wholesale inflation rate in three years, largely driven by a sharp jump in energy costs as gasoline prices surged 15.7%.

The release carries a hawkish to negative inflation signal, coming just days after strong CPI data, as pipeline price pressures suggest businesses are facing higher input costs that could pass through to consumers in the coming months. While the Iran-related oil shock was a key catalyst, underlying producer inflation had already been firming for several months, reinforcing expectations that the Fed may need to keep rates higher for longer.

→ The US ADP Employment change (weekly) rose to +39k jobs for late March (4-wk average), up from +26k previously and the highest reading since the series began in September 2025, signalling a modest re-acceleration in private hiring. Sentiment is mildly positive for growth, suggesting labour demand remains resilient despite geopolitical uncertainty, though the gain is still modest versus historical payroll trends and unlikely to materially shift Fed expectations on its own.

→ China’s March trade data showed a sharp divergence: exports rose just 2.5% YoY, slowing markedly from +22% in Jan-Feb and missing expectations (8%), while imports surged 27.8% YoY, the strongest gain since late 2021. The softer export print suggests external demand and shipping conditions were hit by the Middle East energy shock, while the jump in imports points to firmer domestic demand, AI-related chip purchases and commodity restocking.

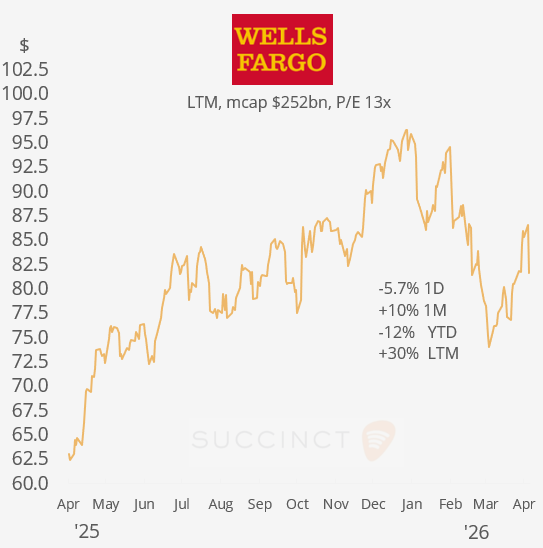

Earnings: → Today’s US earnings slate was solid but mixed in market reaction: major banks and J&J (+1%) mostly beat expectations, but investors focused more on outlooks than backwards-looking results. JPMorgan Chase (-0.8%), Citigroup (+2.7%) and BlackRock (+3%)were viewed positively, while Wells Fargo (-5.7%) lagged. Banks benefited from strong trading and investment-banking activity amid volatile markets. Citigroup rose on strong fees, BlackRock gained on profit and ETF inflows, while Wells Fargo fell after softer net interest income.

Bottom line: constructive but cautious sentiment, good results partly offset by concerns over oil, inflation and Middle East risks to growth.

Deals: → Amazon agreed to acquire Louisiana-based satellite communications operator Globalstar (mcap $10bn) for $11.6bn, one of its largest-ever deals, accelerating Amazon’s push into low-Earth-orbit satellite internet and intensifying competition with SpaceX’s Starlink. The acquisition gives Seattle-based Amazon immediate access to Globalstar’s satellite network and valuable spectrum rights, supporting future direct-to-device mobile connectivity services beyond traditional broadband. GSAT shares jumped ~10% today and 31% YTD.

→ In Australia’s mining sector, Yancoal Australia Ltd (mcap $6.1bn) agreed to buy an 80% stake in the Kestrel coking coal mine in Queensland for up to $2.4bn, strengthening its position in Australia’s premium metallurgical coal sector.

Day Ahead: Data → €-zone industrial production; China retail sales, industrial production, GDP growth. Earnings → Bank of America, Morgan Stanley, PNC, Hermes.

See you tomorrow.

Copyright © 2026 Succinct.

All rights reserved. This publication contains proprietary content and is intended solely for the recipient’s personal use. Disclaimer: Our service is for informational purposes only and does not constitute personal financial advice.