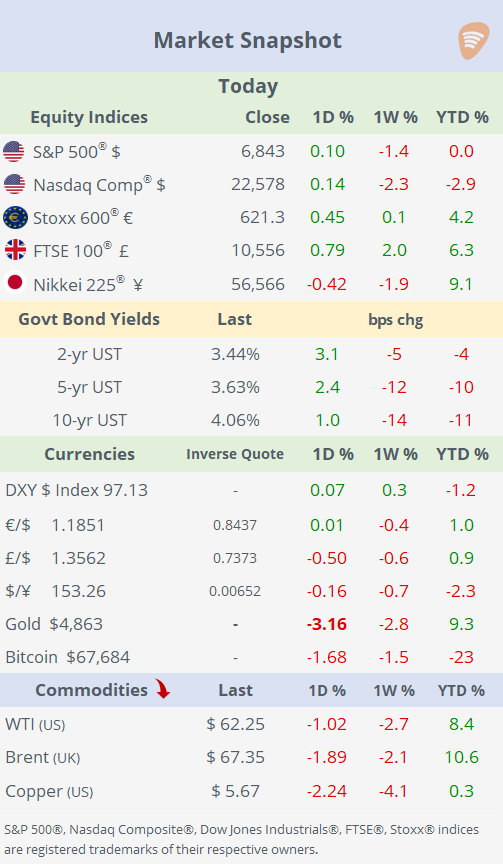

Tue 17 Feb: After the Bell

Volatile Open, Flat Finish: AI Worries Still in Focus

Good evening,

US markets reopened to volatile but ultimately flat trading on Tuesday, as investors continued to digest persistent AI-related concerns that have unsettled equities in recent weeks. Technology shares led early declines, with worries that AI could disrupt business models across multiple sectors, from wealth management and transportation to logistics and software, weighing on sentiment, before a late-session rebound helped stabilise prices as dip-buyers emerged.

Trading conditions remained cautious in thin, post-holiday liquidity, with investors also assessing labour-market signals from the latest ADP employment data alongside easing geopolitical tensions following constructive US–Iran talks, a combination that dampened safe-haven demand and left gold and silver under pressure.

Private software firms McAfee and Rocket Software are voluntarily releasing earnings to reassure lenders, as AI disruption has become a credit risk for legacy software business models. The early disclosures aim to protect funding access, stabilise spreads, and support refinancing, despite no public reporting requirement.

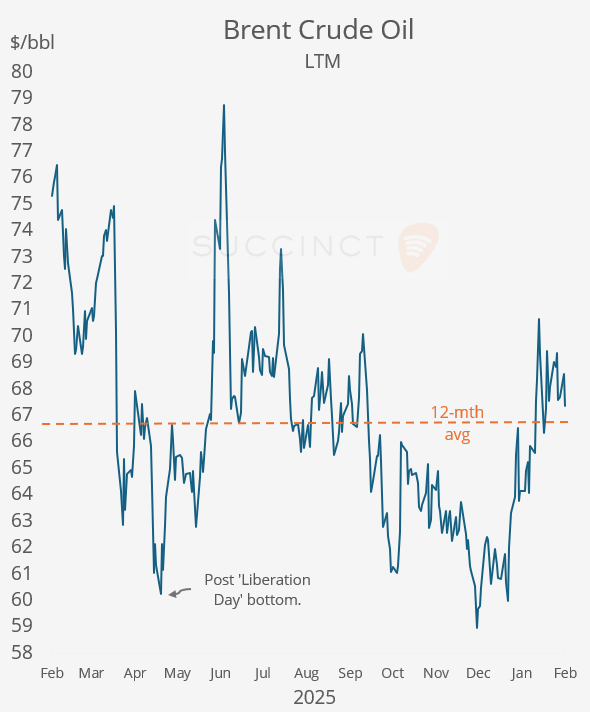

In geopolitics, the US and Iran reported progress in indirect nuclear talks in Geneva, agreeing on a set of “guiding principles” that both sides described as serious and constructive, easing some regional pressure, a dynamic that helped Brent oil fall ~2% as traders priced in lower immediate conflict risk.

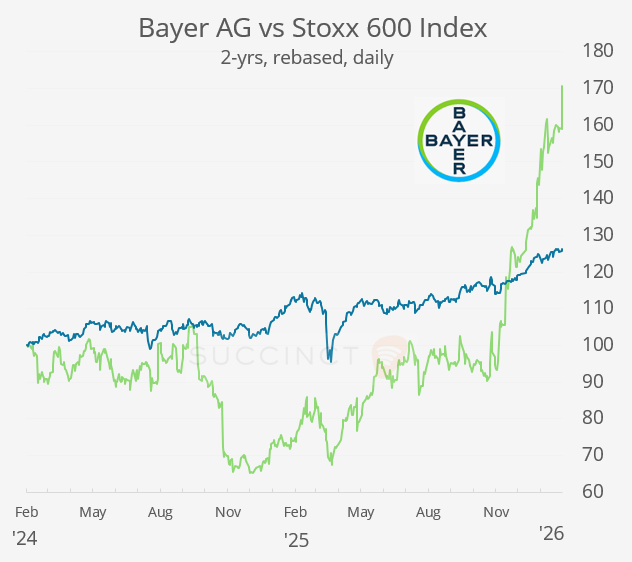

In business news, Germany’s Bayer AG (mcap €48bn) said it will pay a proposed $7.2bn settlement to resolve current and future US cancer lawsuits over its Roundup weedkiller (originally part of its 2018 acquisition of Monsanto), to contain prolonged litigation risk. Bayer shares jumped 7% to a ~3-year high on the announcement, reflecting reduced legal uncertainty.

Economics: → US ADP weekly employment update showed that private employers added an average of ~10k jobs per week in the four weeks to Jan 31, a modestly strengthening pace of hiring, pointing to continued but not strong labour market momentum.

→ UK jobs data showed unemployment rising to ~5.2%, near a five-year high, and wage growth cooling, a weaker-than-expected print that tilted sentiment dovish and reinforced expectations of rate cuts by the Bank of England (in four weeks).

→ Canada’s January inflation report showed headline CPI slowing to about 2.3% YoY and core CPI moderating slightly to 2.6%, coming in a touch softer than expectations, reinforcing the dovish bias for the Bank of Canada.

Corporate Deals: → In the healthcare and medical devices sector in the US, Danaher Corp (mcap $145bn) agreed to acquire Masimo Corp (mcap $9.4bn) for $10bn all-cash, buying a leading patient-monitoring / pulse-oximetry specialist to strengthen Danaher’s diagnostics and lab equipment franchise. Masimo shares jumped 34% today to a one-year high.

→ In Europe, German shipping giant Hapag-Lloyd AG (mcap €20bn) agreed to acquire Israel’s rival Zim (mcap $3.3bn), the world’s tenth-largest container shipping line, for $4.2bn all-cash, consolidating global container shipping / maritime logistics and strengthening trade routes across major global corridors. The bid represents a 58% premium to Zim’s share price at close on Friday. Zim rallied 25% today.

→ South African telco MTN Group (mcap $22bn) agreed to acquire UK-based IHS Towers for $6.2bn in an all-cash deal for telecom infrastructure (mobile towers). MTN already owned 25% of IHS, with European investment firm Wendel holding a 19% stake.

Day Ahead:

Data → US housing starts, building permits, durable goods, industrial production and FOMC Minutes; UK inflation.

Earnings → Booking Holdings, Analog Devices, DoorDash, Moody’s, Glencore, Occidental Petroleum.

See you tomorrow.

Copyright © 2026 Succinct.

All rights reserved. This publication contains proprietary content and is intended solely for the recipient’s personal use. Disclaimer: Our service is for informational purposes only and does not constitute personal financial advice.