Tue 20 Jan: After the Bell

Geopolitics Drive Risk-Off as Cold Snap Sends Natural Gas Higher. Your 5’ evening market wrap📄📈

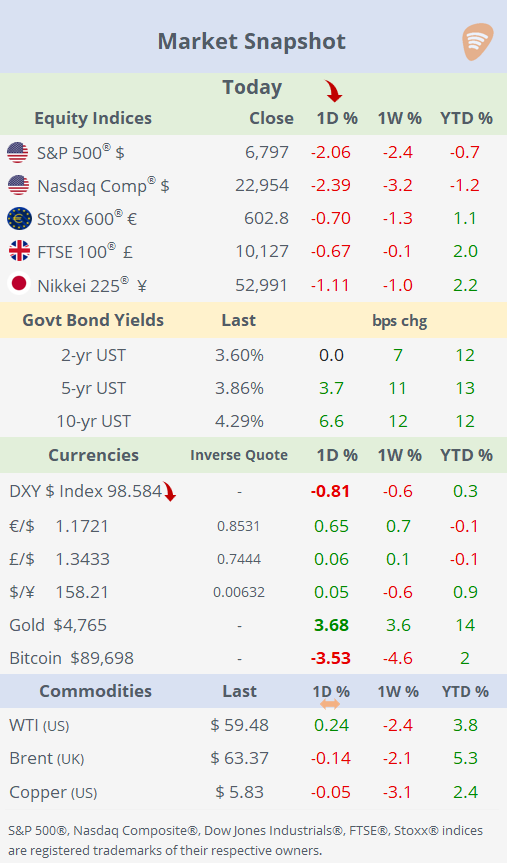

ℹ️ Today’s performance tables & charts on the ‘Market Data’ post.

Good evening,

Risk-off sentiment dominated markets on Tuesday, with global equities selling off sharply after the US reopened from Monday’s holiday. Benchmark indices fell by more than 2%, marking their weakest session of the month so far, led by declines in technology stocks. The trigger was a fresh geopolitical shock, as Trump announced tariffs on eight NATO allies amid renewed rhetoric around Greenland, just ahead of his arrival at the World Economic Forum in Davos.

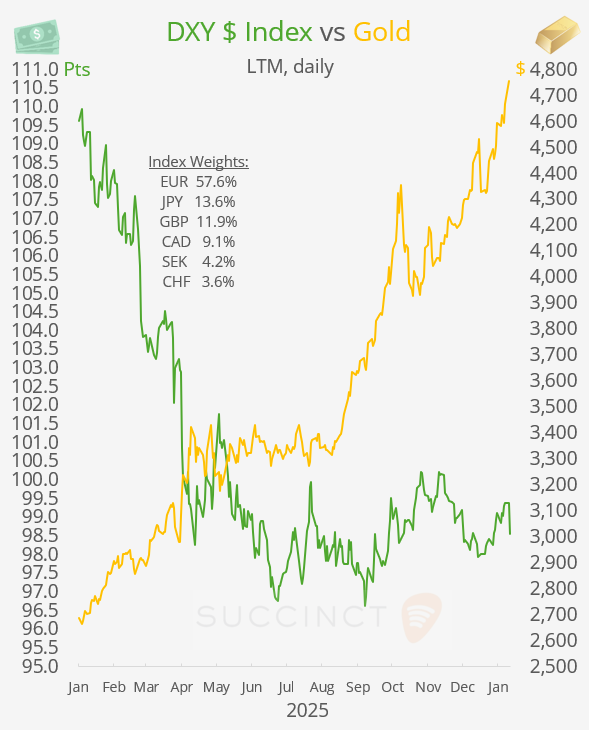

Market stress was evident across asset classes. The VIX jumped two points to 20.3%, its highest level since late November, while the $ weakened, with the DXY touching its lowest level of January and the Swiss franc rallying nearly 1% to its strongest level this year. Bond markets sold off globally: the 10-yr Treasury yield climbed to 4.30%, the highest close since August, while Japan’s long-end yields hit record highs on fiscal concerns tied to a potential tax-cut-driven election outcome.

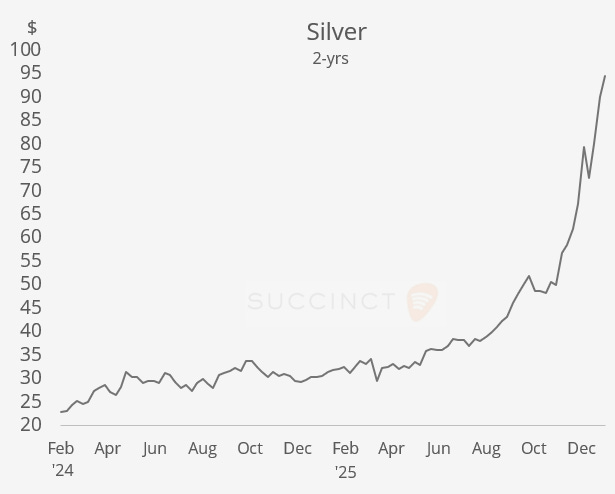

Safe havens outperformed, with gold ($4,765) and silver ($94) hitting fresh record highs, while risk assets continued to struggle. Bitcoin fell for a sixth consecutive session to a three-week low near $89,00, underscoring the broad-based retreat from risk.

A notable mover in the commodities space was natural gas. US natgas prices rallied sharply (+19%) today as weather models shifted toward a much colder forecast, with an Arctic blast expected to bring frigid conditions across the Midwest and Northeast, boosting anticipated heating and power demand. Traders repriced supply/demand risk quickly, pushing front-month futures significantly higher after recent lows. The jump also reflects weather-driven short-covering and tighter-than-expected inventories, making gas one of the strongest-moving commodities on the day.

Earnings: → After the close, Netflix shares fell ~5% in extended trading despite a modest beat on Q4 earnings and revenue, with EPS at $0.56 and revenue of $12.05bn, supported by strong subscriber growth to 325m and higher pricing. Revenue rose 18% YoY, driven by membership gains and rapidly expanding advertising, with ad revenue up more than 2.5x to over $1.5bn in 2025. The market reaction reflected cautious sentiment around forward-looking factors, including increased content spending, a pause in share buybacks linked to the pending Warner Bros. Discovery acquisition, and guidance that, while solid, did not materially exceed expectations. Shares are down 6% this year, up 2% in the LTM and plunged 37% from their all-time high six months ago.

Economics: It was a quiet day on the data front.

→ Germany’s producer prices fell 2.5% YoY in December, a deeper-than-expected decline that marked the steepest annual PPI drop since April 2024, highlighting renewed deflationary pressure at the factory gate. The data underline continued weakness in upstream costs, reinforcing the euro area’s disinflationary trend.

→ US ADP data showed private-sector employment rose by 8,000 jobs last week, the weakest reading since late November but still consistent with a gradually cooling, rather than deteriorating, labour market. The print suggests hiring momentum is moderating as conditions normalise.

Corporate Deals: → British pharma giant GSK (mcap £72bn) has agreed to acquire US biotech Rapt Therapeutics (mcap $1.6bn) for $2.2bn, as it looks to strengthen its drug pipeline amid looming patent expirations. The deal values Rapt at $58 per share, with an estimated $1.9bn up-front payment. The acquisition adds ozureprubart, a long-acting therapy for food allergies, enhancing GSK’s immunology portfolio. Rapt shares jumped 64% today and accumulated a 500% return in the LTM.

→ Zurich Insurance (mcap $101bn) has made a £7.7bn ($10bn) bid for UK specialist insurer Beazley (mcap £6.6bn), offering a 56% premium to its prior close amid accelerating consolidation in the European insurance sector. Beazley’s board previously rejected a lower £12.30 per-share proposal as undervaluing the company. A combination would create an insurer with around $15bn in gross written premiums, strengthening Zurich’s speciality and Lloyd’s of London footprint.

→ Netflix (mcap $373bn) has revised its bid for Warner Bros Discovery’s studio and streaming assets to an all-cash offer of $27.75 per share, valuing the business at $82.7bn including debt, as it competes with a rival bid from Paramount.

Day Ahead:

→ Data: UK inflation, US pending home sales, Indonesia policy rate.

→ Earnings: J&J, Charles Schwab, Prologis, Kinder Morgan, Travelers.

See you tomorrow.

Copyright © 2025 Succinct.

All rights reserved. This publication contains proprietary content and is intended solely for the recipient’s personal use. Disclaimer: Our service is for informational purposes only and does not constitute personal financial advice.